NWS Nieuws & Achtergronden

Discussieer hier diepgaander over de actualiteiten.

Genoteerd. Ik zal het 'conspiracy theory'-gehalte van de artikelen die ik post laag houden.quote:

Ex-IMF economist sees large US bank collapsing

Daaropvolgend:

Rogoff's warning part of the problem

Shanghai Surge Sparks Region's Reboundquote:The truth is, the collapse of Bear Stearns Cos. [..] was about [..] confidence.

Oil Rises a Second Day on Dollar Drop, Gasoline Supply Forecastquote:Shanghai stocks soared Wednesday on speculation that the Chinese government was considering a fiscal stimulus package, triggering a recovery across the region.

quote:U.S. supplies of gasoline probably fell 3 million barrels last week from 202.8 million barrels the previous week, according to the median of 13 responses in a Bloomberg News survey of analysts. The Energy Department is scheduled to release the report at 10:35 a.m. in Washington.

Inventories of crude oil probably rose 1.05 million barrels in the week ended Aug. 15, the survey showed. Stockpiles of distillate fuel, including heating oil and diesel, probably gained 1 million barrels.

The problem is not the occupation, but how people deal with it.

Zet de popcorn maar in de magnetron.

http://finance.google.com/finance?q=NYSE%3AFre&hl=en

http://finance.google.com/finance?q=NYSE%3AFNM

Dit kan nooit lang meer gaan duren (als ze -20 %+ per dag down gaan).... de FED heeft er eigenlijk geen zin in. Maar ze moeten wel.

http://finance.google.com/finance?q=NYSE%3AFre&hl=en

http://finance.google.com/finance?q=NYSE%3AFNM

Dit kan nooit lang meer gaan duren (als ze -20 %+ per dag down gaan).... de FED heeft er eigenlijk geen zin in. Maar ze moeten wel.

Vooral het dikgedrukte stukje maakt het intresant. Wanneer je als aandeelhouder geld moet bijstorten ben ik benieuwd hoeveel aandeelhouders de aandelen willen blijven bezitten.quote:'Geldinjecties ECB niet eindeloos'

Uitgegeven: 21 augustus 2008 08:03

Laatst gewijzigd: 21 augustus 2008 08:04

AMSTERDAM - De Europese Centrale Bank kan niet eindeloos doorgaan met het openhouden van de geldkraan voor banken met geldmarktproblemen. Dat heeft Nout Wellink, president van de Nederlandsche Bank en directielid van de ECB, gezegd tegen Het Financieele Dagblad.

"Als we zien dat banken wel erg afhankelijk worden van centrale banken, dan moeten we ze stimuleren andere financieringsbronnen aan te snijden." Dit betekent dat aandeelhouders in het uiterste geval geld moeten bijstorten, aldus de krant.

Centrale banken hebben sinds het uitbreken van de kredietcrisis ruim een jaar geleden vele tientallen miljarden in de markt gepompt om een systeemcrisis te voorkomen.

Banken zijn voorzichtig met het uitlenen van geld aan elkaar, omdat ze niet weten in hoeverre andere banken geraakt zijn door slechte investeringen in producten gelieerd aan de Amerikaanse huizenmarkt.

Dat gaat dan via een claimemissie en de claims kun je normalitair op de beurs verkopen. Maar het geeft natuurlijk verwatering dus de aandelenkoersen zullen dalen. Ahold heeft in 2003 (of 2004?) ook een claimemissie gedaan om de balans te repareren.quote:Op donderdag 21 augustus 2008 08:15 schreef Basp1 het volgende:

[..]

Vooral het dikgedrukte stukje maakt het intresant. Wanneer je als aandeelhouder geld moet bijstorten ben ik benieuwd hoeveel aandeelhouders de aandelen willen blijven bezitten.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Overigens wel goed dat de ECB dit nu zegt

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

quote:Club Goodbye Dollar

‘Een spectaculair afscheidsfeest van de dollar’

30 augustus in ‘De Balie’ in Amsterdam (Leidseplein).

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

De dollar is nu toch weer flink aan het zakken. 1 euro is nu 1486. Dat was gisteren nog 2 cent minder.

quote:

Ben wel benieuwd naar het debat met Middelkoop en Bouman

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Het verhaal gaat iets verder... ECB / FED gooien de handdoek in de ring. Banken moeten het zelf oplossen. In Azie staat de geldkraan zo goed als dicht. Bron BNR.quote:Op donderdag 21 augustus 2008 08:15 schreef Basp1 het volgende:

Vooral het dikgedrukte stukje maakt het intresant. Wanneer je als aandeelhouder geld moet bijstorten ben ik benieuwd hoeveel aandeelhouders de aandelen willen blijven bezitten.

Nu begint het pas echt leuk te worden..... dat de kredietstromen leeg dreigen te raken.

quote:-Het belangrijkste bericht betrof het nieuws dat Lehman Brothers niet in staat is geweest een belang in zichzelf te verkopen aan enkele Aziatische staatsfondsen. Het gaat hier niet eens om Lehman, maar vooral om de terughoudendheid van die Aziatische investeerders om geld te steken in Westerse belangen.

-Nogal wat bekende en grote financials hebben nog veel nieuw geld nodig en de gedachte was dat er wel gerekend kon worden op die Aziatische staatsfondsen. Iedere twijfel daaraan zorgt voor extra nervositeit en dus lagere koersen.

-Voor de rest waren er allerlei uitspraken van DNB-president Wellink. Over de inflatie, over de huizenprijzen en over de ECB-steunoperaties.

Aziaten beseffen dat geld mogelijk beter is, Cash is Kingquote:Op donderdag 21 augustus 2008 21:18 schreef Drugshond het volgende:

[..]

Het verhaal gaat iets verder... ECB / FED gooien de handdoek in de ring. Banken moeten het zelf oplossen. In Azie staat de geldkraan zo goed als dicht. Bron BNR.

Nu begint het pas echt leuk te worden..... dat de kredietstromen leeg dreigen te raken.

[..]

http://www.blikopdebeurs.com/weblog1/pivot/entry.php?id=83quote:Jim Cramer: Lehman is "zwart gat"

21 08 08 - 22:51

Zakenbank Lehman Brothers is een "verscholen zwart gat", waar snel iets aan gedaan moet worden. Dat zegt Jim Cramer op CNBC. Aziatische kopers haken af, reserves drogen op en Citigroup verwacht nieuwe miljardenafschrijvingen.

dat bijstorten zal wel niet om 1 % gaan, maar om 100% of wie weet wel 1000% om sommige 'zwarte gaten' te redden. Denk niet dat er veel zijn die daar nog in mee zullen gaan.quote:Op donderdag 21 augustus 2008 08:15 schreef Basp1 het volgende:

[..]

Vooral het dikgedrukte stukje maakt het intresant. Wanneer je als aandeelhouder geld moet bijstorten ben ik benieuwd hoeveel aandeelhouders de aandelen willen blijven bezitten.

bron: Nu

Tja niet geheel onverwacht natuurlijkquote:NEW YORK - De olieprijs is donderdag met bijna 6 dollar gestegen tot 121,50 dollar per vat, onder invloed van de oplopende geopolitieke spanningen tussen de Verenigde Staten en Rusland. Het is de sterkste stijging van de olieprijs op één dag in meer dan twee maanden.

ANP

Oliehandelaren reageerden sterk op de boze reacties van Rusland op het akkoord over een raketschild dat Polen en de VS woensdag sloten.

Deze spanningen komen bovenop de onrust over de militaire interventie van de Russen in Georgië, waardoor de doorvoer van olie door Georgische pijpleidingen werd verstoord.

Ook de zwakkere dollar zorgt voor een oplopende olieprijs omdat olie dan goedkoper wordt voor kopers met andere valuta. De prijs van een vat lichte Amerikaanse olie (van 159 liter) bereikte in juli nog een recordniveau van meer dan 147 dollar.

To deny our impulses would deny the very thing that make us human.

Zou dat bijstorten dan gebaseerd zijn op de huidige aandelen prijs, als het eenmaal pennystocks zijn geworden hoeft men relatief gezien toch niet veel bij te strorten. Afgezien van het megaverlies wat ze al geleden hebben door de sterke waardevermindering van hun aandelen.quote:Op vrijdag 22 augustus 2008 05:31 schreef indahnesia.com het volgende:

[..]

dat bijstorten zal wel niet om 1 % gaan, maar om 100% of wie weet wel 1000% om sommige 'zwarte gaten' te redden. Denk niet dat er veel zijn die daar nog in mee zullen gaan.

quote:Amerikanen kopen Duits slachtoffer kredietcrisis

AMSTERDAM - De Duitse staatsbank KfW heeft na elf maanden een koper gevonden voor de bijna failliete IKB Deutsche Industriebank. KfW vond de redder in het land waar ook de problemen ontstonden die IKB aan het wankelen brachten: de Verenigde Staten. IKB was de eerste Duitse bank die vorig jaar zomer slachtoffer werd van de Amerikaanse crisis rond riskante hypotheken, die toen in alle hevigheid losbarstte.

IKB komt voor bijna 91 procent in handen van Lone Star Funds, een private investeerder uit Texas. Dat wil niet zeggen óf en wat het betaalt voor IKB. Na de bekendmaking dat de Amerikanen de Duitse bank overnemen, steeg het aandeel IKB met 12 procent tot 2,99 euro op de beurs in Frankfurt. Daarmee zouden beleggers de waarde van de bank op 289 miljoen euro schatten.

KfW zou 800 miljoen euro voor IKB hebben gevraagd, nadat zij vorig jaar zomer 10 miljard euro in de bank had gepompt om die voor omvallen te behoeden. Het afgelopen jaar moesten vier leden van de raad van bestuur van IKB het veld ruimen wegens hun rol in het debacle, onder wie topman Stefan Ortseifen. Onderzoek wees uit dat het risicobeheer van de bank grote gaten had vertoond. IKB moest 15,1 miljard euro afschrijven – geen enkel Duits bankbedrijf heeft meer geleden onder de wereldwijde kredietcrisis.

Eind mei waren er nog vier gegadigden voor IKB. Analisten denken dat Lone Star Funds het gevecht heeft gewonnen omdat het al eerder een Duitse bank, Corealcredit Bank, rigoureus heeft gesaneerd. De verwachting is dat de Amerikanen fors gaan snijden in de kosten en de positie van de bank op de markt voor leningen aan middelgrote ondernemingen zullen versterken.

quote:Kamer opent aanval op fiscale truc durfkapitaal

Het is niet de bedoeling dat de fiscus nog langer grote overnames financiert, meldt de Financiële Telegraaf vrjdag. De Tweede Kamer wil dat staatssecretaris De Jager (Financiën) de wet aanpast om deze constructie te dwarsbomen. Nu gaan vooral opkoopfondsen soms torenhoge leningen aan voor een aankoop, zodat er een ’papieren verlies’ ontstaat. Dat verlies geeft vervolgens recht op fiscale compensatie, waarmee een groot deel van de overname kan worden betaald. Afgelopen jaar maakte de Belastingdienst via deze werkwijze honderden miljoenen euro’s over aan Angelsaksische durfkapitalisten, die eigenaar zijn van onder meer Hema, kabelbedrijf Ziggo en afvalverwerker Van Gansewinkel.

CDA, SP en GroenLinks zijn ontstemd en willen weten hoeveel geld de fiscus daadwerkelijk kwijt is door deze constructie, die overigens gewoon wettelijk toegestaan is. De partijen dringen aan op beperking van de renteaftrek voor grote overnames. De Nederlandse Vereniging van Participatiemaatschappijen (NVP), waarin zestig Nederlandse durfkapitalisten zijn gebundeld, vindt dat er appels met peren worden vergeleken.

„De laatste dagen wordt ‘private equity’ behoorlijk in het verdomhoekje gezet. Men bekijkt bedrijven waarin wij beleggen als beursfondsen en dat is een andere categorie, die gebonden is aan specifieke regels wat betreft vermogensverhoudingen”, stelt André Olijslager, voorzitter van de NVP en voormalig topman van Friesland Foods. „Wij investeren waar anders niets zou gebeuren, omdat de banken het risico niet aandurven. Onze inzet is de omzet te verhogen en daarmee de waarde van het bedrijf. Winstgevendheid, een belangrijk item voor aandeelhouders op de beurs, speelt in de private equity-wereld minder. Je wilt een bedrijf groter en sterker maken om het na gemiddeld vijf jaar door te verkopen”, aldus Olijslager.

De zestig aangesloten participatiemaatschappijen investeren in 1400 bedrijven, waarvan ruim duizend in Nederland. Bij die inmiddels bijna 1050 bedrijven in Nederland werken 300.000 mensen, 8% van de hele werkzame bevolking. Private equity is dan ook niet meer weg te denken en creëert mogelijkheden die anders onbenut zouden blijven. Dat is volgens Olijslager de andere kant van de medaille. Hij stelt dat ook beursgenoteerde bedrijven schulden maken die worden afgetrokken. „Daar kan ik ook zo een optelsom van honderden miljoenen maken. Dat is nou eenmaal de wet en hele legers belastingadviseurs staan bedrijven bij om zo min mogelijk kwijt te zijn aan de fiscus. Dat is volkomen legaal, die mensen worden niet gearresteerd of zo. Alleen als een private equity-bedrijf gebruik maakt van de geldende belastingregels, wordt meteen moord en brand geschreeuwd.”

De Tweede Kamer wil alleen de excessen bestrijden. De renteaftrek voor de ’super op de hoek’ moet gewoon blijven bestaan, vindt CDA-Kamerlid Omtzigt, samen met zijn collega’s De Nerée en Blanksma. Maar papieren verliezen creeren zodat je geld terug krijgt over de rente die over de lening betaald wordt, dat moet niet meer kunnen, vindt het CDA. De Kamerleden opperen dat de renteaftrek getemporiseerd zou kunnen worden. Hun SP-collega Irrgang denkt dat De Jager eens naar Duitsland zou moeten kijken, waar de renteaftrek afhangt van de verhouding van eigen en vreemd vermogen. Ook zou je de fiscale aftrek afhankelijk kunnen maken van de verhouding tot de brutowinst.

’Private equity staat in het verdomhoekje’

GroenLinkser Vendrik wijst erop dat hij minister Wouter Bos van Financiën al een half jaar geleden heeft gevraagd om een notitie over de fiscale problematiek rond opkoopfondsen. „Ik neem aan dat Bos kort na de zomer met die notitie komt”, aldus Vendrik gisteren. Over de aantijging dat ‘private equity’ over lijken gaat, bedrijven failliet laat gaan en de serviceverlening op een zacht pitje laat zetten, is Olijslager ronduit ontstemd. „Investeringsfirma’s hebben geen enkel belang bij een faillissement en ook niet bij minder service. Dat is juist de kurk waarop een bedrijf moet drijven en groeien.”

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

oh dat was de truuk... in procenten rekenen!quote:Op vrijdag 22 augustus 2008 10:49 schreef Basp1 het volgende:

[..]

Zou dat bijstorten dan gebaseerd zijn op de huidige aandelen prijs, als het eenmaal pennystocks zijn geworden hoeft men relatief gezien toch niet veel bij te strorten. Afgezien van het megaverlies wat ze al geleden hebben door de sterke waardevermindering van hun aandelen.

What the hell ?!?quote:Wall street: Dow sluit 1,7% hoger

De financials op Wall Street gingen in volle vaart vooruit na berichten dat er mogelijks een overname van Lehman Brothers in de maak is. De Dow Jones kreeg een extra stimulans van Ben Bernanke, voorzitter van de Federal Reserve. Die gaf gisteren aan dat er niet meteen een renteverhoging aan komt.

Speculators Don't Hold 81% of Oil Market, CFTC Saysquote:Op zondag 24 augustus 2008 21:52 schreef geenID het volgende:

81% van oliecontracten is in handen van speculanten.

En de zaak vanuit een ander punt bekeken:quote:Aug. 21 (Bloomberg) -- Crude oil speculators don't control 81 percent of the oil contracts traded on the New York Mercantile Exchange, the U.S. Commodity Futures Trading Commission said, rebutting a Washington Post article.

The newspaper article published today is ``factually incorrect'' in saying that financial firms account for that much of the market, the regulator said.

[...]

Commercial Firms

The article notes in its 12th paragraph that some swaps dealers handle trades for commercial firms, which are not considered speculators.

Vitol Group, a commodities trader based in Rotterdam, said the article's description of its position in oil markets and the ``implied relation to oil price movements is fundamentally incorrect.''

The article says the company was betting oil prices would rise on June 6, when prices spiked $11 a barrel, with contracts equivalent to 57.7 million barrels on Nymex.

Vitol said in an e-mailed statement its net position on ``the main international exchanges'' that day was short 11 million barrels.

The commission said it will make public a report on speculation in commodity markets by Sept. 15.

Incorrect Media Speculation About Those Oil Speculators

The problem is not the occupation, but how people deal with it.

Het blijft gezeik over definities idd. Imo willen ze het gewoon delta neutral hebben en valt het wel mee qua speculatie.

Total returns van aandelenmarkten sinds de bodem in 2003.

De slechtst presterende markt zit nog steeds op +10% annualized.

De slechtst presterende markt zit nog steeds op +10% annualized.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

De ECM blijft de lekkerste returns hebben idd, zeker compounded is het heel veel meer dan bij de DCM en andere markten.

Dat is alleen op korte termijn zo. Op langere termijn krijg je een heel ander plaatje.quote:Op maandag 25 augustus 2008 10:22 schreef geenID het volgende:

De ECM blijft de lekkerste returns hebben idd, zeker compounded is het heel veel meer dan bij de DCM en andere markten.

Mijn punt was meer dat zelfs de slechtste markt in het plaatje (Japan) nog steeds 10% annualized heeft gemaakt vanaf de bodem in 2003. Btw ook leuk dat China bijna onderaan staat, ondanks (of dankzij) de hype.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

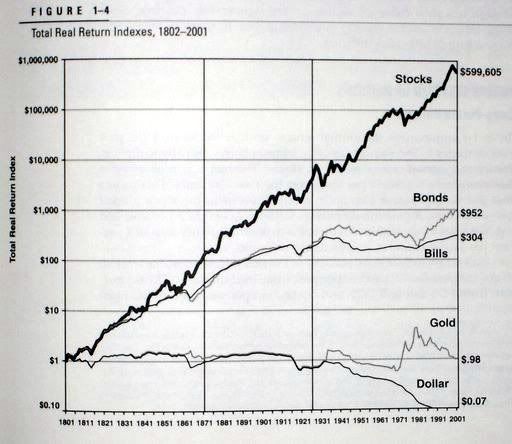

Historisch reeel rendement op aandelen is 6,9% geweest in de afgelopen 200 jaar, en dat is inderdaad aanzienlijk beter dan obligaties.quote:Op maandag 25 augustus 2008 10:57 schreef geenID het volgende:

Aandelen hebben een lagere historische return dan obligaties? Lijkt me heel sterk.

Dit plaatje is al een miljoen keer gepost, maar het is dan ook erg illustratief

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

quote:Bankiers en economen in verwarring door crisis

De kredietcrisis stelt 's werelds belangrijkste monetaire beleidsmakers en economen voor een raadsel. Dit bleek afgelopen weekeinde bij de jaarlijkse bijeenkomst van centrale bankiers en topeconomen in het Amerikaanse Jackson Hole.

,,We zullen allemaal moeten toegeven dat we in verwarring zijn. Niet zozeer vanwege dalende huizenprijzen of een financiële crisis, maar wel door de ernst en de lengte ervan'', hield econoom en voormalig centrale bankier Peter Fisher zijn collega's voor.

Topman Mario Draghi van de Italiaanse centrale bank waarschuwde dat het nog jaren kan duren voordat het vertrouwen op de financiële markten is hersteld. Ben Bernanke, de voorzitter van het Amerikaanse stelsel van centrale banken, viel hem hierin bij en stelde dat er geen ,,snelle oplossing'' voor de problemen voorhanden is.

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Wel bekende grafiek idd. Ik kwam btw nog een aardige Q&A van Warren Buffett tegen op Youtube: (deel 1 van 10), misschien wel nice voor de OP. Een mix van grappen en wijsheden.quote:Op maandag 25 augustus 2008 11:02 schreef SeLang het volgende:

[..]

Historisch reeel rendement op aandelen is 6,9% geweest in de afgelopen 200 jaar, en dat is inderdaad aanzienlijk beter dan obligaties.

Dit plaatje is al een miljoen keer gepost, maar het is dan ook erg illustratief

[ afbeelding ]

ECM, DCM. què?quote:Op maandag 25 augustus 2008 10:22 schreef geenID het volgende:

De ECM blijft de lekkerste returns hebben idd, zeker compounded is het heel veel meer dan bij de DCM en andere markten.

Het zijn de meest algemene termen voor de aandelenmarkt (Equity Capital Markets) en obligatiemarkt (Debt Capital Markets.) Ze nemen het een beetje over van de US Army om overal een acroniem of afkorting aan te geven.quote:

Aha, tanx.quote:Op maandag 25 augustus 2008 12:38 schreef geenID het volgende:

[..]

Het zijn de meest algemene termen voor de aandelenmarkt (Equity Capital Market) en obligatiemarkt (Debt Capital Market.) Ze nemen het een beetje over van de US Army om overal een acroniem of afkorting aan te geven.

Wikipedia kent deze termen niet, maar bijvoorbeeld wel European Common Market.

bronquote:Sharp contractions in the money supply and recession are two spokes on the same wheel. When the money supply shrinks, there's less economic activity, and the economy slows; it's as simple as that. An article in this week's UK Telegraph by Ambrose Evans-Pritchard shows that the country is sliding inexorably into the jaws of a deep recession.

From the UK Telegraph:

"The US money supply has experienced the sharpest contraction in modern history, heightening the risk of a Wall Street crunch and a severe economic slowdown in coming months. Data compiled by Lombard Street Research shows that the M3 ''broad money" aggregates fell by almost $50bn in July, the biggest one-month fall since modern records began in 1959.

"Monthly data for July show that the broad money growth has almost collapsed," said Gabriel Stein, the group's leading monetary economist." (Ambrose Evans-Pritchard,"Sharp US Money Supply contraction points to a Wall Street crunch ahead", UK Telegraph)

The Telegraph confirms what many of the doomsayers have been saying for more than a year now; we're facing a severe bout of deflation. The persistent credit-drain from rising foreclosures and deleveraging financial institutions is shrinking the money supply. Now it's visible in the data. Bernanke's low interest rates haven't stopped the hemorrhaging; deflation is spreading like Kudzu. According to Evans-Pritchard, "The growth in bank loans has turned negative" (while) "the overall debt burden in the US economy is currently at record levels, raising concerns that a recession - if it occurs - could set off a sharp downward spiral."

The under-capitalized banking system has slowed its lending and consumers have stopped borrowing; all the main economic indicators are pointing down. In fact, according to the Conference Board, "weakness among the leading indicators continues to be widespread" and dropped more than 0.7% in July alone. The report is a composite of selected indicators that show the overall direction of the economy. At present, they're all in negative territory.

The Fed lowered interest rates to 2 per cent hoping to help recapitalize the banks and stimulate consumer spending, but it hasn't worked. The banks still don't have the capacity to lend, so the main artery for credit distribution remains clogged and GDP is dropping off. A python has wrapped itself around the financial system and is gradually cutting-off the oxygen supply. Naturally, when the credit system is broken, the money supply contracts. That's true here, too. What's troubling is the speed at which it is all of this is taking place. It's "the biggest one-month fall since modern records began in 1959". The process is accelerating and will require the Fed to slash rates at its September meeting.

Economist Nouriel Roubini puts it like this:

"Over time inflation will be the last problem that the Fed will have to face as a severe US recession and global slowdown will lead to a sharp reduction in inflationary pressures in the U.S.: slack in goods markets with demand falling below supply will reduce pricing power of firms; slack in labor markets with unemployment rising will reduce wage pressures and labor costs pressures; a fall in commodity prices of the order of 30% will further reduce inflationary pressure.

The Fed will have to cut the Fed Funds rate much more as severe downside risks to growth and to financial stability will dominate any short-term upward inflationary pressures. Leaving aside the risk of a collapse of the US dollar given this easier monetary policy the Fed Funds rate may end up being closer to 0% than 1% by the end of this financial crisis and severe recession cycle."

Interest rates are going down not up as the futures market believes.

Federal Reserve chief Bernanke understands the problem, but has no way to fix it. The market is simply correcting from massive credit imbalances. The economy needs time to cool off and rebalance. Bernanke's various "auction facilities" were created to keep the banking system afloat while the government delivered "stimulus checks" to working people. The plan was designed to bypass the dysfunctional banking system and give money directly to taxpayers. Unfortunately, the strategy failed and added to the bulging fiscal deficits. Martin Feldstein summed it up like this in the Wall Street Journal:

"Recent government statistics show that only between 10% and 20% of the rebate dollars were spent. The rebates added nearly $80 billion to the permanent national debt but less than $20 billion to consumer spending....Here are the facts. Tax rebates of $78 billion arrived in the second quarter of the year. The government's recent GDP figures show that the level of consumer outlays only rose by an extra $12 billion, or 15% of the lost revenue. The rest went into savings, including the paydown of debt....Consumer outlays increased to $36 billion from $24 billion. So the additional $12 billion of consumer spending was less than 16% of the extra $76 billion of disposable personal income. By comparison, savings rose by $62 billion, or five times as much....This experience confirms earlier studies showing that one-time tax rebates are not a cost-effective way to increase economic activity."

The whole "stimulus" plan backfired. Americans did the responsible thing and used the money to pay off debts or stash it in savings instead of than wasting it Walmart or Target on more useless knick-knacks. It just goes to show that average working people can change their spending habits and making prudent choices when they see that times are tough. The culture of consumerism is the result of Madison Ave. saturation-campaigns and propaganda; there's nothing inherently wrong with the American people. Workers are constantly being blamed for "living beyond their means", but the real problem originates from flawed monetary policy and destructive commercialism. It's the prevailing "sicko" corporate culture that has created a nation of spendthrifts and speculators. Ordinary people are not at fault.

Fiscal stimulus can work if it is used properly, like if it was applied to the payroll tax. That would be the same as giving every working man and woman in America a sizable raise in pay that could used to give the economy a boost. (Couples making under $70,000 per year spend 100% of their earnings. They represent 50% of total GDP) The problem, however, is that that would violate a central tenet of neoliberalism which dictates that the payroll tax be used in the General Fund as a de facto flat tax levied against the poor and middle class to ensure that the ruling elite don't not have to pay their fair share for the maintenance of the empire. Bush and his ilk would rather run the economy off a cliff than compromise on their core values. The real reason we are faced with the current economic downturn is because wages have not kept pace with production which means that workers have had to increase their borrowing to maintain their same standard of living and keep the economy growing. If wages are flat the economy can't grow; it's as simple as that. That's why banking elites have lowered standards for lending; it's just a way to generate profits and create growth without giving workers the raise they deserve. It has the added benefit of pushing people into a life of debt-peonage. Americans are deeper in debt than anytime in history and are struggling just to make the interest payments on their loans. As a result, more and more homeowners are walking away from their mortgages and leaving the banks with huge, unanticipated debts. The architects of America's debt-slavery system are turning out to be its biggest victims.

Currently, billions of dollars are disappearing in the secondary market where bets were placed on mortgage-backed securities that are now virtually worthless. As market volatility increases, frazzled investors are moving into cash. Credit is being wrung from the system while the money supply continues to contract.

Mike Shedlock of Mish's Global Economic Trend Analysis gives this technical analysis:

"The recent plunge in M3 (ed.--M3 is the broadest measure of money used by economists to estimate the entire supply of money) makes it likely that credit lines have been fully tapped and/or banks have simply turned off the spigot. Liquidity shrinks by the day. Banks scrambling to refinance long-term debt are going to have a very tough go of it. Weekly unemployment claims are soaring. Consumers out of a job are going to have a tough time paying bills. Those looking for a bottom in these conditions are simply barking up the wrong tree."

The prospects of a deep and protracted downturn are now greater than ever. Financial institutions are either pulling back and preparing for the storm ahead or taking advantage of existing credit lines while they last. The herky-jerky market action suggests that a growing number of CEOs and CFOs can see that the walls are closing in on them. The crash-alert flag is about half-way up the pole.

Author Ellen Hodgson Brown's new book "The Web of Debt", points out some of the parallels some between our present predicament and events leading up to the Great Depression:

"The problem began in the Roaring Twenties when the Fed made money plentiful by keeping interest rates low. Money seemed to be plentiful, but what was actually flowing freely was 'credit' or 'debt'. Production was up more than wages, so more goods were available than money to pay for them; but people could borrow. ...Money was so easy to get that people were borrowing just to invest, taking out short-term, low interest loans that were readily available from the banks".

Sound familiar?

Brown continues: "The Fed began selling securities in the open market, reducing the money supply by reducing the reserves available for backing loans..The result was a huge liquidity squeeze---a lack of available money. Short-term loans suddenly became available only at much higher interest rates, making buying stock on margin much less attractive. As fewer people bought, stock prices fell, removing the incentive for new buyers to purchase stocks bought by earlier buyers on margin...The stock market crashed overnight."

The money supply contracted dramatically during the first few years of the Great Depression. Free-market guru, Milton Friedman, went so far as to blame the Central Bank for the disaster. He said, "The Federal Reserve definitely caused the Great Depression by contracting the amount of currency in circulation by one-third from 1929 to 1933."

As a result, interest rates rose and credit became scarcer. To some extent, these things are taking place already. Long-term interest rates and LIBOR have been rising and are headed higher. These are much more accurate gages of the "real" price of credit than the Fed's artificial Fed Funds Rate (2 per cent) which is just a give-away to the banks.

Brown does a good job of connecting the dots and showing how the Federal Reserve engineered the Depression with their failed monetary policies and serial bubble making. In another chapter, she quotes Louis T. McFadden, Chairman of the House Banking and Currency Committee, who is explicit in his condemnation of the Fed:

(The Depression) was not accidental. It was a carefully contrived occurrence. ...The international bankers sought to bring about a condition of despair here so that they might emerge as rulers of us all". (Ellen Hodgson Brown; "The Web of Debt", page 146)

Whether the present economic crisis was deliberate or not is irrelevant. The ultimate responsibility for our economic woes lies with the Fed; that's who created the speculative bubble that is now wreaking havoc on the broader economy. Millions of people will lose their homes, trillions of dollars of equity will be wiped out, and hundreds of banks will fail. Eventually, there will be more consolidation among the banks and greater concentration of wealth among fewer people. An self-regulated system run by unelected businessmen naturally gravitates towards monopoly and, yes, tyranny.

Charles Lindbergh summed up the role of the Federal Reserve like this:

"The financial system has been turned over to ...a purely profiteering group. The system is private, conducted for the sole purpose of obtaining the greatest possible profits from the use of other people's money." (Ellen Hodgson Brown; "The Web of Debt")

The impending global recession has nothing to do with crafty mortgage lenders, opportunistic loan applicants, dodgy rating agencies, or crooked home appraisers. That's like blaming Lindy England for Abu Ghraib. The source of the troubles is the Federal Reserve and monetary policies that are designed to rob people of their life savings.

Abolish the Fed.

ietwat aan de "great conspiracy"-kant, maar wel een redelijke samenvatting

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Leuk artikel....volgens sommige analisten moet de run nog echt beginnen.

Een zeer belangrijke mijlpaal is al gezet..... op de buitenlandse investeerders hoeven we niet te rekenen. Dus het verstevigen van de kapitaal positie gaat nu gepaard met de verkoop van onderdelen van een bank.

Q3/Q4 worden spannend. Wie dan hun balans niet op orde heeft mag nu zelf de portemonnee trekken.

Een zeer belangrijke mijlpaal is al gezet..... op de buitenlandse investeerders hoeven we niet te rekenen. Dus het verstevigen van de kapitaal positie gaat nu gepaard met de verkoop van onderdelen van een bank.

Q3/Q4 worden spannend. Wie dan hun balans niet op orde heeft mag nu zelf de portemonnee trekken.

De een na laatste zin is een beetje raar in de context van deflatie.

Tijdens een deflatoire periode zijn spaarders juist de grote winnaars, want hun geld wordt meer waard. Zij kunnen allerlei assets voor een appel en een ei kopen.

Tijdens een deflatoire periode zijn spaarders juist de grote winnaars, want hun geld wordt meer waard. Zij kunnen allerlei assets voor een appel en een ei kopen.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

FDIC may borrow money from Treasury

quote:(Reuters) - Federal Deposit Insurance Corp (FDIC) might have to borrow money from the Treasury Department to see it through an expected wave of bank failures, the Wall Street Journal reported.

The borrowing could be needed to cover short-term cash-flow pressures caused by reimbursing depositors immediately after the failure of a bank, the paper said.

The borrowed money would be repaid once the assets of that failed bank are sold.

"I would not rule out the possibility that at some point we may need to tap into (short-term) lines of credit with the Treasury for working capital, not to cover our losses," Chairman Sheila Bair said in an interview with the paper.

[..]

The fact that the agency is considering the option again, after the collapse of just nine banks this year, illustrates the concern among Washington regulators about the weakness of the U.S. banking system in the wake of the credit crisis, the Journal said.

The problem is not the occupation, but how people deal with it.

De FDIC heeft nog een 30b credit line met Treasury. Reuters neemt kennelijk niet alles over uit het WSJ artikel.

UK huizenprijzen

Nu terug op het niveau van 2006, dus eigenlijk is er nog weinig aan de hand. Al zou je eigenlijk nog de inflatie eraf moeten trekken om een realistisch beeld te krijgen (in de laatste 2 jaar is dat zo'n 8-9% totaal)

Nu terug op het niveau van 2006, dus eigenlijk is er nog weinig aan de hand. Al zou je eigenlijk nog de inflatie eraf moeten trekken om een realistisch beeld te krijgen (in de laatste 2 jaar is dat zo'n 8-9% totaal)

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Ruzie Fortis en Rabobank...

Opmerkelijk dat dit nog relatief weinig aandacht krijgt. Een grote bank die impliceert dat je spaargeld niet veilig zou zijn bij een collega grote bank. Nieuwe fase in de kredietcrisis?

Zojuist geplaatst op onze eigen site. http://www.blikopdebeurs.com/weblog1/pivot/entry.php?id=88quote:'Fortis-top woedend op Rabobank'

28 08 08 - 19:45

Uitlatingen van Rabobank bestuurslid Bert Bruggink zijn slecht gevallen bij Fortis en ING. Bruggink meldde veel nieuw spaargeld van Fortis en ABN omdat "klanten er ook van op aan moeten kunnen dat ze het er weer vanaf kunnen halen".

Een woordvoerder van Fortis noemt de uitspraken van Bruggink in NRC Handelsblad “hoogst onverantwoordelijk” en “een gevaar voor de stabiliteit van het financiële systeem”. “Ze impliceren dat geld bij Fortis, een van de grootste financiële instellingen van Nederland, niet veilig staat”, aldus de bank in een ongekend felle reactie tegenover dezelfde krant donderdag.

Spaargeld van Fortis

Rabobank meldde woensdag bij de halfjaarcijfers dat in de afgelopen twee maanden 6,3 miljard euro aan “toevertrouwde middelen” zijn binnengekomen, voor een groot deel spaargeld afkomstig van Fortis. Zowel Rabo als Fortis willen weinig kwijt over de ‘bankierstwist’. Fortis verwijst naar uitspraken van topman Verwilst vorige week, dat er “geen sprake is van een significante uitstroom”.

Financieel topman Bruggink ging ook in op de herwaardering van de beleggingsportefeuille. “Als je de cijfers van ING op deze manier zou presenteren, dan zou hun afschrijving niet 300 miljoen bedragen maar 10 miljard”. ING heeft nog niet formeel gereageerd, maar naar verluidt is het bestuur ‘not amused’ over de uitspraken van de Rabo-collega.

Opmerkelijk dat dit nog relatief weinig aandacht krijgt. Een grote bank die impliceert dat je spaargeld niet veilig zou zijn bij een collega grote bank. Nieuwe fase in de kredietcrisis?

Wat zit er nu onder die ijsberg. ?quote:What the 'problem bank' list doesn't say

More banks are in trouble nowadays, but some experts wonder just how accurate a picture the FDIC's list paints of the industry.

NEW YORK (CNNMoney.com) -- The government's latest assessment of the nation's financial system showed that many more small banks are in trouble. But what the report didn't say may speak volumes.

On Tuesday, the Federal Deposit Insurance Corp. revealed that the number of institutions on its so-called "problem bank" list jumped to 117 during the second quarter, up from 90 just three months earlier.

That list has gained greater attention lately as many banks continue to suffer losses stemming from the deteriorating housing market and slowdown in the broader economy. Nine banks have failed so far this year, including IndyMac, a California-based mortgage lender with assets of $32 billion at the time of its collapse.

But experts contend that the list is a lagging indicator and, as a result, may not provide an accurate picture of the current health of U.S. banking industry.

Typically, the list is published some 8 weeks after all of the nation's banks have reported their latest quarterly results.

What's more, notes Mark J. Flannery, a professor of finance at the University of Florida's Warrington College of Business Administration, regulators base their decision on what banks tell them.

And since current accounting standards give banks some discretion about when they recognize bad news, they may want to put it off as long as possible.

Exactly how bank regulators determine which institution is worthy for the "problem list" remains a process shrouded in secrecy.

But what is known is that the health of a bank tends to be based on several factors including the amount of capital an institution has on hand to protect against losses, the quality of its assets, its management, and its earnings, liquidity and sensitivity to market risk.

Bank regulators - which in addition to the FDIC include the Office of the Comptroller of the Currency (OCC) and Office of Thrift Supervision (OTS) - then give the banks a report card, assigning a composite rating based on the bank's performance in each category. Those that receive a rating of 4 or 5 are put on the list.

A selective list?

Since the failure of IndyMac in mid-July, however, speculation has emerged that regulators may have exercised some discretion about which institutions they put on the confidential list.

The FDIC's first-quarter problem list, released at the end of May, clearly did not have IndyMac on it. That's because the FDIC reported that the 90 banks on the list had a combined $26.3 billion in assets - less than the size of IndyMac. That suggested that the only problem banks at the time were smaller community banks.

Experts say that if IndyMac had been on the list, the total asset size of troubled banks would have been much higher. That might have prompted a witch hunt of sorts, with the market looking for which bank was in trouble and possibly causing a run on that institution.

"It is kind of the issue of the snake swallowing the watermelon," said Bert Ely, an Alexandria, Va.-based banking industry consultant of Ely & Co. "I can assure you if IndyMac had been on the list in late May, there would have been an immediate hunt."

Others pointed out that bank failures, as a rule, don't happen to be overnight phenomena.

Tim Yeager, a professor of finance at the University of Arkansas' Walton College of Business who previously worked for the Federal Reserve Bank of St. Louis, said regulators probably knew about the state of IndyMac for some time even though it wasn't on the first-quarter problem list.

"It is telling that IndyMac was not on the problem list the quarter before," said Yeager. "Usually bank failures like that are pretty slow events - it is unlikely [federal regulators] were surprised by that."

The OTS, IndyMac's primary regulator, has maintained that it was aware of the company's problems, but was in the midst of an examination of the lender that did not wrap up until after the first quarter was over. At that point, IndyMac was placed on the list.

If it ain't broke....

Those who keep a close eye on the nation's banking industry argue that the nearly 30-year-old bank monitoring system, commonly referred to as CAMELS (which stands for Capital adequacy, Asset quality, Management, Earnings, Liquidity and Sensitivity to market risk) remains quite effective at gauging a bank's health.

In recent years, there have been calls for regulators to take into greater account the wisdom of the market, most notably a bank's stock price or the yield a company's debt is trading at.

As innovative a solution that may be, the lion's share of the nation's banks are not publicly traded. What's more, those indicators aren't always reliable, note experts such as Flannery.

Stock prices, for example, can be affected by broader gyrations in the market and may not accurately predict if a bank will go bust or is even on the verge of failure.

"I think there are times when the CAMELS system is more informative and times when the market price is more informative," said Flannery. "There is no general rule."

If regulators are at a disadvantage, it is determining just how many banks could fail as a result of the current credit crisis.

While regulators are working hard to stay ahead of the problems faced by banks, their forecasting models have not endured a credit or mortgage crisis of this magnitude before and, as a result, have no way of telling how deep the impact will be.

"You can look at this and say they are missing the problems, but this business cycle is different from others," said Yeager. "You need to go through this to be able to update the model - it is really a Catch-22." To top of page

De Rabobank is sowieso een beetje een vreemde eend in de bijt. Niet beursgenoteerd (en dus door de buitenwacht minder goed te beoordelen), maar ik citeer wikipedia even:quote:Op donderdag 28 augustus 2008 20:13 schreef HansAEX het volgende:

Ruzie Fortis en Rabobank...

[..]

Zojuist geplaatst op onze eigen site. http://www.blikopdebeurs.com/weblog1/pivot/entry.php?id=88

Opmerkelijk dat dit nog relatief weinig aandacht krijgt. Een grote bank die impliceert dat je spaargeld niet veilig zou zijn bij een collega grote bank. Nieuwe fase in de kredietcrisis?

Aan de oppervlakte ziet het er allemaal top notch uit en misschien is het dat ook wel gewoon. Je zult mij ook niet horen zeggen dat die lui van de Rabobank liegen dat het gedrukt staat en die Triple A kredietrating zal vast wel ergens op gebaseerd zijn. Maar het is toch allemaal een beetje 'anders dan anders'.quote:"De kredietwaardigheid van de Rabogroep is de hoogst haalbare, de Triple A-status, toegekend door Moody's en Standard & Poor's.

Naar eigen zeggen behoort de Rabobank Groep tot de vijftien grootste financiële instellingen van de wereld gemeten naar kernvermogen."

Dat ze kritiek hebben op Fortis is misschien ergens wel terecht. Maar ik denk dat ze beter niet te hoog van de toren kunnen blazen, want wie weet wat er nog komt. Zulke openbare kritiek komt op mij niet erg betrouwbaar over (eerder een beetje proleterig) en het wekt bij mij juist een beetje de suggestie dat er bij de Rabobank misschien zelf iets aan de hand zou kunnen zijn (bijvoorbeeld rap dalende spaartegoeden door al die internetspaarbankjes). Als zoiets dan toch geuit moet worden, doe het dan lekker binnenskamers, tijdens het maandelijkse overleg bij DNB ofzo.

Ik denk ook niet dat de Rabobank er erg veel bij te winnen heeft als Fortis kopje onder gaat. Ja, op de hele korte termijn misschien, maar uiteindelijk worden ze zelf ook de dupe van een ernstige daling in het vertrouwen van de consument in financiële instellingen.

Op dinsdag 28 oktober 2008 20:02 schreef Mwanatabu het volgende:

Denk dat jij met je bord voor je kop blij mag zijn dat jij niet achter een raam staat met je kontje als kutje :W

Denk dat jij met je bord voor je kop blij mag zijn dat jij niet achter een raam staat met je kontje als kutje :W

Het artikel op NRC.nl.quote:Op donderdag 28 augustus 2008 20:13 schreef HansAEX het volgende:

Ruzie Fortis en Rabobank...

[..]

Zojuist geplaatst op onze eigen site. http://www.blikopdebeurs.com/weblog1/pivot/entry.php?id=88

Opmerkelijk dat dit nog relatief weinig aandacht krijgt. Een grote bank die impliceert dat je spaargeld niet veilig zou zijn bij een collega grote bank. Nieuwe fase in de kredietcrisis?

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Het is gewoon een beetje onhandige uitspraak van die Rabobank man. Ik zou er niet teveel belang aan hechten. Hij wilde gewoon even het punt maken dat Rabo één van de meest solide banken ter wereld is.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Oke, ik zou dit soort artikelen niet meer posten, maar toch.

Economic Numbers - Can They Be Trusted?

Economic Numbers - Can They Be Trusted?

Jullie gedachten?quote:[..]

Buried in that release is the real outrage:

"Domestic profits of financial corporations increased $24.7 billion in the second quarter, compared with an increase of $37.3 billion in the first. Domestic profits of non-financial corporations decreased $46.9 billion in the second quarter, compared with a decrease of $32.1 billion in the first."

Excuse me?

Do you actually expect me to believe that profits of financial corporations increased by $24.7 billion (or that they did so in the first quarter either)?

Am I smoking something or did not the financial sector report decreasing profits in the second quarter, and in fact, many reported absolutely stunning losses?

[..]

So we have a totally bogus "financial service profits" number which of course pumps reported GDP substantially.

If you're interested in how Americans are doing, try this:

"Real gross domestic purchases -- purchases by U.S. residents of goods and services wherever produced -- increased 0.2 percent in the second quarter, compared with an increase of 0.1 percent in the first."

Right. Including $160 billion in stimulus checks, which incidentally, is about 1% of GDP. So how much would it have fallen without spending $160 billion that we don't have?

I'll answer that, since the same page gives me a metric to use. 1.4 GDP points (percent) is $39.7 billion (so the BEA says); that is a 5.6% annualized "run rate" on GDP.

So GDP actually fell (using the cooked numbers) by 1.4% on an annualized basis in the second quarter, since taking $160 billion out of one hand and placing it into another didn't actually change a thing (the government doesn't have any money; they get it from you, so the "stimulus" should in fact be subtracted back out from any claimed "GDP" - but isn't), and this assumes you believe the BEA's "deflater" (inflation) number which is vastly different than the CPI reported elsewhere and that financial firms increased their profits in the second quarter!

One final note. If you find and read Rosenberg's research report (its worth looking for; try a search on the forum) you'll find that the non-financial corporate deflater came in at negative 3.8%.

For the uninitiated, positive numbers indicate inflation (in prices), while negative ones indicate "that which Bernanke claims cannot happen here with The Fed on watch" - that nasty "D" phrase, otherwise known as a "deflationary collapse."

The problem is not the occupation, but how people deal with it.

er lopen hier verschillende statistici rondquote:Op vrijdag 29 augustus 2008 12:20 schreef waht het volgende:

Oke, ik zou dit soort artikelen niet meer posten, maar toch.

Economic Numbers - Can They Be Trusted?

[..]

Jullie gedachten?

het is ons beroep om te goochelen met cijfers lieverd

edit:

bijvoorbeeld:

bij sommige berekeningen worden in de VS huiseigenaren gezien als "ondernemers" en dus wordt er een (fictieve) huuropbrengst meegerekend bij het inkomen van de betreffende huiseigenaar. of die nu daar zelf woont of niet!

verder: hou rekening met 'imputatie': dat is wanneer je van een boel gegevens (stel, voor het berekenen van de gemiddelde benzineprijs, ik noem maar wat) er enkele niet hebt (te laat ingeleverd, niet compleet ingevuld, etc...) worden die geschat. daar is dus vrij veel mogelijkheid tot fouten/manipulatie.

en uiteraard zijn de inflatiecijfers al jaren 'verdacht'. die discussie is hier al vaker gevoerd!

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

De inflatiecijfers zijn toch niet het verdacht, het is alleen opvallend dat men altijd weer andere berekeningsmethodes bedenkt/ mandjes veranderd. Maar het cijfertje klopt als een bus, ik heb nog een i^2=-1 gezien.quote:Op vrijdag 29 augustus 2008 14:21 schreef simmu het volgende:

en uiteraard zijn de inflatiecijfers al jaren 'verdacht'. die discussie is hier al vaker gevoerd!