WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Oud bericht:

Jim Rogers .

.

http://www.nu.nl/algemeen(...)ecrisis-in-2030.htmlquote:'Wereldwijde voedsel- en energiecrisis in 2030'

Uitgegeven: 20 maart 2009 09:35

Laatst gewijzigd: 20 maart 2009 10:04

AMSTERDAM - De snelle groei van de wereldbevolking zal over 20 jaar leiden tot een wereldwijde crisis wegens tekorten aan voedsel, energie en water. Dat voorspelt de wetenschappelijke adviesraad van de Britse regering.

Volgens berekeningen van de Britse wetenschapsraad zullen er in 2030 meer dan 8,3 miljard mensen op aarde leven (1,5 miljard meer dan nu).

De vraag naar voedsel en energie zou daardoor stijgen met 50 procent. Het waterverbruik neemt door de bevolkingsgroei waarschijnlijk toe met 30 procent.

Milieuconferentie

De aanwezige grond- en brandstoffen op aarde zijn volgens hoofdwetenschapper John Beddington ontoereikend voor die situatie. Hij presenteerde de voorspelling op de milieuconferentie Sustainable Development UK 09 in Londen.

"Het wordt een noodlottige storm", zo verklaart Beddington op BBC News. "De wereld zal weliswaar niet totaal instorten, maar als we niets aan deze problemen doen, dan wordt het een erg zorgelijke situatie. Er zullen grote internationale voedsel- en watertekorten ontstaan. "

Niet afwachten

De huidige lage prijzen voor olie en voedsel zorgen volgens Beddington voor onderschatting van het probleem. "Dat de prijzen nu zijn gedaald, betekent niet dat we rustig kunnen afwachten."

Volgens de wetenschapper kan een wereldcrisis in 2030 mogelijk worden voorkomen door nieuwe technologieën. Zo gaat in de landbouwsector op dit moment gemiddeld 20 tot 30 procent van de oogst verloren door ziektes en dierenplagen.

Betere oogsttechnieken

"We hebben meer resistente planten nodig en betere oogsttechnieken", aldus Beddington. "Genetische modificatie kan een deel van de oplossing vormen. Met genetische technologie zouden we mogelijk plantsoorten kunnen kweken die resistent zijn tegen droogte."

Jim Rogers

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

http://www.guardian.co.uk(...)rown-china-recessionquote:Robert Zoellick, the World Bank's president, emphasised the need to give multilateral bodies new powers, rather than just extra financing. In a speech in London yesterday Zoellick said: "If leaders are serious about creating new global responsibilities or governance, let them start by modernising multilateralism to empower the WTO, the IMF, and the World Bank Group to monitor national policies.

"Bringing sunlight to national decision-making would contribute to transparency, accountability and consistency across national policies.

"As a first step, the G20 should endorse a WTO monitoring system to advance trade and resist economic isolationism, while working to complete the Doha negotiations to open markets, cut subsidies, and resist backsliding."

Zoellick, Bilderberglid, betrokken geweest bij Goldman Sachs, Fannie Mae, Enron, en een van de bedenkers van de inval in Irak.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

wel sick ze zijn vrijwel geheel afhankelijk van china en ze zitten nu al op de knieen met een bakje eronder om al het slijm op te vangen.quote:Op zondag 5 april 2009 10:54 schreef pberends het volgende:

[..]

http://www.guardian.co.uk(...)rown-china-recession

Zoellick, Bilderberglid, betrokken geweest bij Goldman Sachs, Fannie Mae, Enron, en een van de bedenkers van de inval in Irak.

National Suicide: How Washington is Destroying the American Dream

we moeten anders gaan etenquote:Op zaterdag 4 april 2009 17:33 schreef pberends het volgende:

Oud bericht:

[..]

http://www.nu.nl/algemeen(...)ecrisis-in-2030.html

Jim Rogers

Als water schaarser wordt, dan zal water een grotere aandeel hebben in de kostprijs van voedsel

dus gaan we voedsel gebruiken dat minder energie en minder water nodig heeft.

dus moeten de chinezen aardappels gaan eten

Ik vind dit niet voor hem pleitenquote:

president Wereldbank Zoelick

Ik denk dat hij zijn benoeming te danken heeft aan George dobbeljoe, hij zal wel gauw de baan verliezen

quote:De Wereldbank-president is in Amerika een omstreden figuur. Zoellick werkte voor zijn functie bij de Wereldbank voor hypotheekgigant Fannie Mae, de zakenbank Goldman Sachs en zat daarna in de regering van George W. Bush voor handel en buitenlandse zaken. Al in 1998 schreef hij namens de neoconvervatieve denktank Project for the New American Century (PNAC) een brief aan president Bill Clinton om Irak binnen te vallen.

Dat plan schreef hij dus 3 jaar VOOR 9/11

9 / 11 kwam dus wel heel erg toevallig, of was 9/ 11 opgezet daarvoor??

[ Bericht 2% gewijzigd door henkway op 05-04-2009 13:04:57 ]

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Dat hoef je mij niet te vertellen hoor. Ik denk niet dat Amerika zelf het WTC ingevlogen is, maar zij wisten donders goed dat er aanslagen op die dag zouden gebeuren. Zij hebben het gewoon laten gebeuren door het te negeren, en ook de scrambler-jets op die dag aan de zijlijn te houden voor een grootschalige oefening.quote:Op zondag 5 april 2009 11:54 schreef henkway het volgende:

[..]

Ik vind dit niet voor hem pleiten

president Wereldbank Zoelick

[ afbeelding ]

Ik denk dat hij zijn benoeming te danken heeft aan George dobbeljoe, hij zal wel gauw de baan verliezen

[..]

Dat plan schreef hij dus 3 jaar VOOR 9/11

9 / 11 kwam dus wel heel erg toevallig, of was 9/ 11 opgezet daarvoor??

Door 9/11 kon de neoconservatieve kliek eindelijk hun plannen, die ze al jaren hadden klaarliggen, in het Midden Oosten uitvoeren.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

S&P 500 Can’t See Enough Money to Feed Stocks’ Rally (Update1)

http://www.bloomberg.com/apps/news?pid=20601087&sid=al6lArvbSwuI&refer=home

http://www.bloomberg.com/apps/news?pid=20601087&sid=al6lArvbSwuI&refer=home

National Suicide: How Washington is Destroying the American Dream

Shell gaat de laatste weken ook niet echt goed overigens.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Vleesconsumptie moet ook fors worden teruggedrongen of veranderd (vooral minder rund- en varkensvlees). Dat is zo gruwelijk inefficiënt. Kijk maar eens wat een koe nodig heeft aan water en voedsel om er 1 kilo vlees uit te halen.quote:Op zondag 5 april 2009 11:21 schreef henkway het volgende:

[..]

we moeten anders gaan eten

Als water schaarser wordt, dan zal water een grotere aandeel hebben in de kostprijs van voedsel

dus gaan we voedsel gebruiken dat minder energie en minder water nodig heeft.

dus moeten de chinezen aardappels gaan eten

---

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

Ik ben ook anti-vlees ivm het milieu en energie, van mij mogen ze er accijns op heffen.

Ik eet overigens wel elke dag een hamburger á 40 eurocent.

Ik eet overigens wel elke dag een hamburger á 40 eurocent.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Ben zelf ook wel wat hypocriet daarin want rundvlees vind ik ook gewoon lekker. Pasta met rundergehakt is een van mijn favoriete gerechten. Maar als ze nou eens een goed alternatief voor vlees uitvinden, dat nagenoeg zo smaakt en qua structuur identiek is (maar wel mileuvriendelijk uiteraard) doe ik mee, het moet dan wel betaalbaar zijn. Dat nepvlees dat er nu is, is vaak niet zo lekker en ook nog eens peperduur.quote:Op maandag 6 april 2009 13:44 schreef pberends het volgende:

Ik ben ook anti-vlees ivm het milieu en energie, van mij mogen ze er accijns op heffen.

Ik eet overigens wel elke dag een hamburger á 40 eurocent.

---

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

http://www.lewrockwell.com/schiff/schiff12.html

Blijft geweldig dit interview:

Blijft geweldig dit interview:

quote:Q: Okay, Marc, I think this would wrap it up, but I'd like to ask you one question. If you had to leave one message with our readers to take away from all this, what would that be? What would be the big takeaway for them?

MF: We live now in an environment of very, very high volatility, because on the one hand you have the private sector that has tightened lending conditions, and wealth has been destroyed, and households will save more and be more prudent financially than they've been; in other words, credit or liquidity is tightening.

Then on the other hand you have these clowns in government that think that they can solve any problem. As Mr. Geithner said recently, "we know how to fix the problems." Well if he knew so well how to fix the problems, why did he let the problems happen in the first place? He was the New York Fed Chairman when the conditions were created! And Mr. Bernanke was the Fed Chairman since, I think, 2005, and he was the architect of this ultra-expansionary monetary policy. They have no credibility at all, and in my opinion they're going to make matters worse. And the worse the economic conditions will become, the more Mr. Bernanke will throw money at the system; and that will lead to huge volatility in the market. You can have rebounds in individual stocks, and in whole markets, of 30 percent in one month, then they can drop 20 percent in a month; don't forget, between November and the end of the December, the 30-year Treasury ran at 20 percent; and from its peak at the end of December it dropped 20 percent.

There is huge volatility and the same will happen in equities. And that's why I think it's very difficult to make long-term predictions. When you have a perfect free-market, it's difficult to predict the future. But when you have a market that is disturbed by government manipulations and money-printing, it's impossible to make any predictions.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

nog meer windowdressing: http://www.cnbc.com/id/30068415

nee, we hebben ze echt moeten meeslepen om deze triljoenensubsidie in ontvangst te nemen

nee, we hebben ze echt moeten meeslepen om deze triljoenensubsidie in ontvangst te nemen

*giggles*quote:Op maandag 6 april 2009 16:10 schreef Dinosaur_Sr het volgende:

nog meer windowdressing: http://www.cnbc.com/id/30068415

nee, we hebben ze echt moeten meeslepen om deze triljoenensubsidie in ontvangst te nemen

tsjek deze link op die pagina dan!

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

hier haakte ik af: "I can practically guarantee you ...."quote:Op maandag 6 april 2009 16:49 schreef simmu het volgende:

[..]

*giggles*

tsjek deze link op die pagina dan!

niet helemaal, maar bij "I know this is true because I've taken advantage of the opportunity personally" kreeg ik Seats&Sofa's flashback's

en de rest heb ik dus niet gelezen.....

http://online.wsj.com/article/BT-CO-20090406-707995.htmlquote:UPDATE: Bank Losses To Exceed Great Depression -Calyon's Mayo

APRIL 6, 2009, 10:55 A.M. ET

NEW YORK (Dow Jones)--Recent actions by the U.S. government to support the banking sector won't stop loan loss levels from exceeding those reached during the Great Depression, banking analyst Mike Mayo of Calyon Securities said Monday.

Mayo, a long-time bear on the banking sector who recently left Deustche Bank, started Calyon's coverage of the U.S. banking sector with an "underweight" rating, indicating investors should minimize exposure in their portfolio.

Though the comments in Monday's report largely reiterate those made in a report Mayo released March 11 while still at Deutsche Bank, they underscore the lingering concerns among investors about the prospects for stabilization in the financial sector. Shares of banks have gained in recent weeks owing to the government intervention, hopes for improved earnings reports and thawing in credit markets, but uncertainty about the health of banks remains high.

Shares of banking sector stocks were leading the decliners in the S&P 500 index Monday morning. Shares of all 11 banks Mayo mentioned in his report were down by more than 3% each in early trading.

Mayo put "underweight" ratings on Bank of America Corp. (BAC), Citigroup Inc. (C) , JPMorgan Chase & Co. (JPM), Comerica Inc. (CMA), PNC Financial Services Group Inc. (PNC) and Wells Fargo & Co. (WFC). He assigned more- bearish "sell" ratings on BB&T Corp. (BBT), SunTrust Banks Inc. (STI), U.S. Bancorp (USB), Fifth Third Bancorp (FITB) and KeyCorp (KEY).

In recent trading, SunTrust shares were posting the biggest declines among those mentioned in the report, down 8.9% at $12.60. Bank of America shares were down 2.2% at $7.43, after falling as low as $7.14 earlier. Citigroup was down 3.5% at $2.75.

Mayo said loan losses for U.S. banks will likely increase to 3.5% from 2% by the end of 2010, due to ongoing problems in mortgage loans and increasing deterioration in credit cards and consumer, construction, commercial real estate and industrial loans. Under a stress scenario, loan losses could reach as high as 5.5%, Mayo said, compared with the 3.4% loss rate reached in 1934.

Loans Not Marked Down Enough

Mayo titled his report "Seven Deadly Sins of Banking," and listed them as "greedy loan growth, a gluttony of real estate, lust for high yields, sloth-like risk management, pride of low capital, envy of exotic fees, and anger of regulators."

He said that the government won't be able to quickly resolve problem loans, which he said had only been marked by the banks that hold them to 98 cents on the dollar.

Furthermore, government efforts to support banks are a "Catch-22," he said, since being leinent with banks that have made mistakes will leave toxic assets on their balance sheets, while being tough on banks after the government stress tests are released in late April would force many of them to raise more dilutive equity capital, which would then hurt banking and lending activity.

"Thus, the industry may transition from the financial crisis (late stages of capital market write-downs) only to have more severe consequences of the economic crisis (loan losses)," Mayo wrote.

The report was Mayo's first since leaving the research department of Deutsche Bank AG (DB) for Calyon Securities USA Inc., an affiliate of the Asia Pacific-area research firm CLSA.

Also Monday, an analyst at BMO Capital Markets told clients in a research report that last month's rally in bank shares was unsustainable. Bank shares in the S&P 500 have rallied about 50% since the second week in March, when positive comments about profitability during January and February by Citigroup CEO Vikram Pandit and other bank CEOs set off a rally that was extended by further government actions to support banks.

Like Mayo, BMO Capital analyst Peter Winter said he was concerned by increasing deterioration in commercial real estate and commercial and industrial loans. Banks' capital reserves are inadequate given the rapid acceleration in problem assets and delinquent payments, he said.

Oh. Yes.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

http://www.rtl.nl/(/finan(...)s_naar_1_procent.xml

1 maands Euribor nu al bijna op 1%

Wat nou kredietcrisis...

1 maands Euribor nu al bijna op 1%

Wat nou kredietcrisis...

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Heb je deze gelezen? Abn amro tradebox maakt fouten

Ik ben benieuwd of hij een poot heeft om op te staan.

ABN-Amro heeft hem zomaar laten handelen zonder geld op zijn rekening te hebben. Daar bovenop nog een storing in TradeBox van ABN. Hij is 60.000 euro lichter...

Ik ben benieuwd of hij een poot heeft om op te staan.

ABN-Amro heeft hem zomaar laten handelen zonder geld op zijn rekening te hebben. Daar bovenop nog een storing in TradeBox van ABN. Hij is 60.000 euro lichter...

I am not omniscient, but I know a lot.

- Goethe, “Faust”

- Goethe, “Faust”

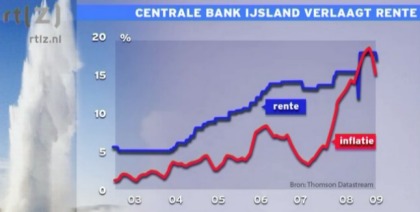

ECB's Nowotny Says 1.00% Rates is Lowest Limit

National Suicide: How Washington is Destroying the American Dream

woo check die candlesticks in de realtime TA grafiek van de S&P, een lange groene bar..................

National Suicide: How Washington is Destroying the American Dream

'Economisch herstel begint in China' .

.

Soros, ga toch met pensioen ouwe seniele manquote:Soros prees overheden wereldwijd. Volgens hem zetten beleidsmakers de juiste stappen om structurele problemen in het financiële systeem en de economie te verhelpen: "Het systeem was fundamenteel zwak en we kunnen niet terug naar waar we vandaan komen."

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

ABN of welke broker dan ook mag iemand niet rood laten staan. Je mag iemand hoogstens rood laten staan op het moment dat iemand aandelen heeft (overwaarde). Vreemd verhaal dat iemand technisch gezien dan kon al kon beleggen.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Post het maar eens daar. TS heeft je steun nodig, merk ik zo...quote:Op maandag 6 april 2009 20:21 schreef pberends het volgende:

ABN of welke broker dan ook mag iemand niet rood laten staan. Je mag iemand hoogstens rood laten staan op het moment dat iemand aandelen heeft (overwaarde). Vreemd verhaal dat iemand technisch gezien dan kon al kon beleggen.

I am not omniscient, but I know a lot.

- Goethe, “Faust”

- Goethe, “Faust”

Meredithquote:Wall Street diept verliezen uit door bankzorgen

06-04-2009 19:45:42

Brussel (tijd) - De Amerikaanse beurzen staan maandag halfweg de sessie nog dieper in de rode cijfers dan bij aanvang. Bankwaarden worden verkocht nu het recente optimisme over de sector volgens een aantal analisten voorbarig was. Berichten over het afspringen van de overname van Sun Microsystems door IBM weegt op de technologiewaarden.

Omstreeks 19.30 uur noteert de Dow 1,8 procent lager op 7.877,17 punten, de S&P500 geeft 2,1 procent prijs op 825,05 punten. Technologiebeurs Nasdaq gaat dieper in het rood met een verlies van 2,2 procent.

Beleggers zijn nerveus in afwachting van de officiele aftrap van het, vermoedelijk sombere, resultatenseizoen dinsdag. Dan komt de aluminiumgigant Alcoa nabeurs als eerste met cijfers over het eerste kwartaal. Na het beursoptimisme van de laatste weken worden de eerstekwartaalcijfers gezien als de lakmoesproef voor een duurzaam beursherstel. Alcoa geeft 6,1 procent prijs op 7,66 dollar.

Bankwaarden krijgen er eveneens van langs nadat analist Mike Mayo van Calyon Securities, een onderdeel van Credit Lyonnais Securities Asia, een negatief rapport over de sector schreef. Mayo (ex-Deutsche Bank) verwacht dat de banksector nog kredietverliezen zal moeten boeken die de niveau's van de 'Grote Depressie' zullen overstijgen. Nieuwe overheidsingrepen om de sector te ondersteunen zullen volgens Mayo niet het verwachte effect hebben, in het bijzonder omdat de kredietportefeuille's van de banken nog steeds aan 98 procent van hun nominale waarde in de boeken staan.

Ook Meredith Whitney zei in een interview met Forbes dat de banksector nog verdere afwaarderingen zal moeten doorvoeren op de hypotheekgerelateerde activa, nu de vastgoedprijzen hun daling verderzetten. Bovendien kampt de VS met nooit geziene werkloosheidscijfers, wat volgens Whitney niet in de vooruitzichten van de kredietverstrekkers is geïmplementeerd. Whitney verwierf faam door als een van de eerste te wijzen op de grote risico's die Citigroup liep op de aan de Amerikaanse vastgoedmarkt verbonden rommelkredieten. Citigroup gaat 4,6 procent lager, Bank of America noteert 2,5 procent lager, JPMorganChase geeft 4,9 procent prijs.

In de technologiesector keldert Sun Microsystems met 24,3 procent tot 6,44 dollar. Volgens berichten in The Wall Street Journal zou de netwerkspecialist een miljardenovernamebod van IBM (-1,7% op 100,44 dollar) hebben afgewezen. IBM zou 7 miljard dollar of circa 9,4 dollar per aandeel willen bieden voor Sun. Volgens de krant is de raad van bestuur van Sun verdeeld over de deal. Een fractie onder leiding van voorzitter en mede-oprichter Scott McNealy is tegen de inlijving door IBM, terwijl een tweede groep, aangevoerd door CEO Jonathan Schwartz, er voor is.

Ook Cisco Systems weegt op de technologiesector. Het aandeel verliest (-4,4% op 17,36 dollar) fors nadat Goldman Sachs het advies verlaagde van 'buy' naar 'neutral' nu het koersdoel van 18 dollar werd bereikt. Analisten blijven positief over de lange termijn van het bedrijf, maar denken dat de groeiverwachtingen grotendeels ingecalculeerd worden door de markt.

Een opvallende stijger is het casinoconcern MGM Mirage (+34% op 6,23 dollar). De casinoreus, in handen van miljardair Kirk Kerkorian, heeft volgens The Wall Street Journal zakenbank Morgan Stanley ingehuurd om zich te buigen over de mogelijke verkoop van twee winstgevende vestigingen. De opbrengst van de eventuele verkoop moet de zware financiële druk op MGM Mirage verlichten.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Het gaat er daar in de VS volgens mij veel erger aan toe dan politici ons willen doen geloven.quote:Op maandag 6 april 2009 22:33 schreef pberends het volgende:

http://www.rtl.nl/compone(...)doelen.avi_plain.xml

Gaarkeukens VS in de problemen.

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

Ze lopen daar anderhalf jaar voor op de crisis dan wij hier..quote:Op maandag 6 april 2009 22:36 schreef Lemmeb het volgende:

[..]

Het gaat er daar in de VS volgens mij veel erger aan toe dan politici ons willen doen geloven.

I am not omniscient, but I know a lot.

- Goethe, “Faust”

- Goethe, “Faust”

4 triljoen? Das niet best!quote:Europese bankwaarden opnieuw kop van jut

07-04-2009 19:16:53

Brussel (tijd) - De Europese aandelenmarkten zijn gisteren voor de derde dag op rij in de rode cijfers geëindigd. Slechter dan verwachte cijfers over de economie in de eurozone en de vrees dat het nieuwe resultatenseizoen wel eens slechter kan uitdraaien dan gevreesd, wogen flink door op de indexen. Vooral de financiële aandelen kregen het dinsdag zwaar te verduren.

De Europese beurzen waren beduidend lager gestart nadat was bekendgeraakt dat de economie van de eurozone tijdens de laatste drie maanden van vorig jaar nog sterker was gekrompen dan analisten aanvankelijk hadden gedacht.

Veel beleggers, die maandag al een pak negatieve beursrapporten voorgeschoteld hadden gekregen, beschouwden dat als een nieuw signaal dat het optimisme van de afgelopen weken misschien wat te voorbarig was geweest.

Of dat effectief het geval is, zal waarschijnlijk wat duidelijker worden bij de publicatie van de eerstekwartaalcijfers. De markten waren gisteren alvast nagelbijtend aan het wachten op de resultaten van de aluminiumreus Alcoa, het traditionele startschot voor het Amerikaanse resultatenseizoen.

De meeste investeerders leken er alvast van uit te gaan dat die cijfers zullen tegenvallen, en gingen over tot verkopen. Die negatieve trend werd nog verhevigd door uitspraken van beursgoeroe George Soros, die de recente remonte omschreef als een korte rally in een berenmarkt.

De DJ EuroStoxx50 sloot 0,7 procent lager op 2.165,56 punten. Parijs daalde 0,9 procent, Frankurt ging met 0,6 procent achteruit. Dat de Londense FTSE een van de grootste dalers was in Europa met een verlies van 1,6 procent, was voor een flink stuk te wijten aan de terugval van de financiële waarden.

Rommelkredieten

Volgens de Britse krant The Times zou het IMF zijn ramingen voor het totaalbedrag aan rommelkredieten dat de financiële instellingen nog bezitten hebben verhoogd tot 4 triljoen dollar. Bovendien verlaagde het beurshuis Sanford C. Bernstein zijn advies voor de Britse banken. Barclays verloor 8,5 procent op 157,7 pence, Lloyds ging met 8,5 procent achteruit tot 72,9 pence. Royal Bank of Scotland, dat gisteren drastische besparingsmaatregelen aankondigde, dook zelfs 10,40 procent lager tot 26,7 pence.

Het feit dat de Europese economie het slechter dan verwacht blijkt te doen, gaf de aandelen uit de constructiesector gisteren een flinke knauw.

Vooral Wavin, de grootste producent van plastic buizen in Europa, moest het ontgelden. Het aandeel donderde in Amsterdam met 25 procent omlaag tot 2,17 euro. Ook de Franse fabrikant van bouwmaterialen Saint-Gobain verloor heel wat terrein. Het aandeel sloot 6 procent lager op 2,93 euro.

Pieter Suy

pieter.suy@tijd.be

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Dat idee heb ik ook, jaquote:Op maandag 6 april 2009 22:36 schreef Lemmeb het volgende:

[..]

Het gaat er daar in de VS volgens mij veel erger aan toe dan politici ons willen doen geloven.

Vorig jaar was er op het journaal al iemand ie zei dat er in de US hongersnood zou zijn gelijk aan Afrika

dat leek toen idioot

Ik zie de wandelende geraamtes idd hier voorbijkomen.quote:Op dinsdag 7 april 2009 21:29 schreef henkway het volgende:

Vorig jaar was er op het journaal al iemand ie zei dat er in de US hongersnood zou zijn gelijk aan Afrika

dat leek toen idioot

Good intentions and tender feelings may do credit to those who possess them, but they often lead to ineffective — or positively destructive — policies ... Kevin D. Williamson

Ten principles for a Black Swan-proof world

quote:1. What is fragile should break early while it is still small. Nothing should ever become too big to fail. Evolution in economic life helps those with the maximum amount of hidden risks – and hence the most fragile – become the biggest.

2. No socialisation of losses and privatisation of gains. Whatever may need to be bailed out should be nationalised; whatever does not need a bail-out should be free, small and risk-bearing. We have managed to combine the worst of capitalism and socialism. In France in the 1980s, the socialists took over the banks. In the US in the 2000s, the banks took over the government. This is surreal.

3. People who were driving a school bus blindfolded (and crashed it) should never be given a new bus. The economics establishment (universities, regulators, central bankers, government officials, various organisations staffed with economists) lost its legitimacy with the failure of the system. It is irresponsible and foolish to put our trust in the ability of such experts to get us out of this mess. Instead, find the smart people whose hands are clean.

4. Do not let someone making an “incentive” bonus manage a nuclear plant – or your financial risks. Odds are he would cut every corner on safety to show “profits” while claiming to be “conservative”. Bonuses do not accommodate the hidden risks of blow-ups. It is the asymmetry of the bonus system that got us here. No incentives without disincentives: capitalism is about rewards and punishments, not just rewards.

5. Counter-balance complexity with simplicity. Complexity from globalisation and highly networked economic life needs to be countered by simplicity in financial products. The complex economy is already a form of leverage: the leverage of efficiency. Such systems survive thanks to slack and redundancy; adding debt produces wild and dangerous gyrations and leaves no room for error. Capitalism cannot avoid fads and bubbles: equity bubbles (as in 2000) have proved to be mild; debt bubbles are vicious.

6. Do not give children sticks of dynamite, even if they come with a warning . Complex derivatives need to be banned because nobody understands them and few are rational enough to know it. Citizens must be protected from themselves, from bankers selling them “hedging” products, and from gullible regulators who listen to economic theorists.

7. Only Ponzi schemes should depend on confidence. Governments should never need to “restore confidence”. Cascading rumours are a product of complex systems. Governments cannot stop the rumours. Simply, we need to be in a position to shrug off rumours, be robust in the face of them.

8. Do not give an addict more drugs if he has withdrawal pains. Using leverage to cure the problems of too much leverage is not homeopathy, it is denial. The debt crisis is not a temporary problem, it is a structural one. We need rehab.

9. Citizens should not depend on financial assets or fallible “expert” advice for their retirement. Economic life should be definancialised. We should learn not to use markets as storehouses of value: they do not harbour the certainties that normal citizens require. Citizens should experience anxiety about their own businesses (which they control), not their investments (which they do not control).

10. Make an omelette with the broken eggs. Finally, this crisis cannot be fixed with makeshift repairs, no more than a boat with a rotten hull can be fixed with ad-hoc patches. We need to rebuild the hull with new (stronger) materials; we will have to remake the system before it does so itself. Let us move voluntarily into Capitalism 2.0 by helping what needs to be broken break on its own, converting debt into equity, marginalising the economics and business school establishments, shutting down the “Nobel” in economics, banning leveraged buyouts, putting bankers where they belong, clawing back the bonuses of those who got us here, and teaching people to navigate a world with fewer certainties.

Then we will see an economic life closer to our biological environment: smaller companies, richer ecology, no leverage. A world in which entrepreneurs, not bankers, take the risks and companies are born and die every day without making the news.

In other words, a place more resistant to black swans.

The writer is a veteran trader, a distinguished professor at New York University’s Polytechnic Institute and the author of The Black Swan: The Impact of the Highly Improbable

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

Dat is best een lekker wijfquote:

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

quote:

Mwoah. 39 jaar alweer en een beetje belegen.

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

Maar met 39jr inderdaad een jaar of 15 te oud

In elk geval te oud om mijn kind te baren

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

hehehehquote:Op woensdag 8 april 2009 12:26 schreef SeLang het volgende:

[ afbeelding ]

Maar met 39jr inderdaad een jaar of 15 te oud

In elk geval te oud om mijn kind te baren

Nouja, ik ben pas 32 en zou het er zeker nog wel op kunnen hoor, met twee flessen wijn achter m'n kiezen. Oudere vrouwen zijn altijd botergeil.

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

Leuke stellingen waar ik me wel in kan vinden helaas zal het niet zo gaan.quote:Op woensdag 8 april 2009 10:53 schreef Perrin het volgende:

Ten principles for a Black Swan-proof world

ze kan jouw mogelijk nog wel een paar kunstjes lerenquote:Op woensdag 8 april 2009 12:26 schreef SeLang het volgende:

[ afbeelding ]

Maar met 39jr inderdaad een jaar of 15 te oud

In elk geval te oud om mijn kind te baren

Interessante punten, vooral die eerste aangezien vrijwel elk bedrijf ernaar streeft zo groot mogelijk te worden.quote:Op woensdag 8 april 2009 10:53 schreef Perrin het volgende:

Ten principles for a Black Swan-proof world

[..]

The problem is not the occupation, but how people deal with it.

heeheehee! geen commentaar op 30+ vrouwen he! en zekers niet op wijven met hersens in plaats van sperma in hun hoofd!

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Zijn die er ook dan?quote:

heeheehee! geen commentaar op 30+ vrouwen he! en zekers niet op wijven met hersens in plaats van sperma in hun hoofd!

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

simmu zal wel de enige zijn dan eh ?quote:

People once tried to make Chuck Norris toilet paper. He said no because Chuck Norris takes crap from NOBODY!!!!

Megan Fox makes my balls look like vannilla ice cream.

Megan Fox makes my balls look like vannilla ice cream.

Ik prefereer allebei tegelijk in plaats van één van de twee.quote:

[..]

simmu zal wel de enige zijn dan eh ?

[ Bericht 0% gewijzigd door Lemmeb op 08-04-2009 14:13:27 ]

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

Een notoire anti-inflatiehavik bij de Fed is ook om:

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

grmbl. bij mijn weten zitten hier zonder meer verder enkel testosteronbommetjes, dus echt vergelijkingsmateriaal is er niet he! dames, waar zijn jullie?quote:Op woensdag 8 april 2009 13:38 schreef sitting_elfling het volgende:

[..]

simmu zal wel de enige zijn dan eh ?

pas maar op: komende zomer gaan we weer verder fokken. wordt ze weer lekker fel van al die hormonen! is het gelijk afgelopen ook met dat halfbakken gemiep op de beurzen. wonderlijk maar waar, aan de hand van selene en mij kan je precies voorspellen wat het wordt

enfin: ontopic maar weer. ligt het aan mij of is het wat stilletjes rond gm de laatste paar dagen?

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Wat bedoel je met "anti-inflatiehavik"? Was dit iemand die altijd op het gevaar van inflatie zat te hameren, of juist iemand die altijd tegen dat gevaar in ging?quote:

Een notoire anti-inflatiehavik bij de Fed is ook om:

[ afbeelding ]

Afijn, ik ben blij dat hij er hetzelfde over denkt als ik. De enige inflatie die in de VS zou kunnen ontstaan is hyperinflatie, als de dollar valt. Maar dat heeft met 'normale' inflatie weinig meer te maken.

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

quote:Op woensdag 8 april 2009 14:12 schreef Lemmeb het volgende:

[..]

Wat bedoel je met "anti-inflatiehavik"? Was dit iemand die altijd op het gevaar van inflatie zat te hameren, of juist iemand die altijd tegen dat gevaar in ging?

Afijn, ik ben blij dat hij er hetzelfde over denkt als ik. De enige inflatie die in de VS zou kunnen ontstaan is hyperinflatie, als de dollar valt. Maar dat heeft met 'normale' inflatie weinig meer te maken.

Iemand die vooral op het gevaar van hogere inflatie lette.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Zie hier de inflatie-rente roadmap van de Fed de komende jaren.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

En met 'War' wordt WOII bedoeld neem ik aan?

The problem is not the occupation, but how people deal with it.

quote:Op woensdag 8 april 2009 17:16 schreef waht het volgende:

En met 'War' wordt WOII bedoeld neem ik aan?

Wat zijn de stippellijntjes bij de boventste grafiek?

Ongelofelijk om te zien trouwens dat tjdens de grote depressie de industriele productie met 60% terug viel. De grote vraag zal alleen wel zijn was de vroegere industie vergelijkbaar met de huidige industrie. Tijdens de grote depressie werkten bijvoorbeeld veel mensen op het land, en tegenwoordig kunnen we zelfs de landbouw al als een industrie beschouwen. En qau diensten kan ik me niet voorstellen dat die al zoveel in overvloed aanwezig waren tijden de grote depressie.

Ongelofelijk om te zien trouwens dat tjdens de grote depressie de industriele productie met 60% terug viel. De grote vraag zal alleen wel zijn was de vroegere industie vergelijkbaar met de huidige industrie. Tijdens de grote depressie werkten bijvoorbeeld veel mensen op het land, en tegenwoordig kunnen we zelfs de landbouw al als een industrie beschouwen. En qau diensten kan ik me niet voorstellen dat die al zoveel in overvloed aanwezig waren tijden de grote depressie.

Juist in de industrie was er toen een enorme gesubsidieerde overproduktiequote:Op woensdag 8 april 2009 18:35 schreef Basp1 het volgende:

Wat zijn de stippellijntjes bij de boventste grafiek?

Ongelofelijk om te zien trouwens dat tjdens de grote depressie de industriele productie met 60% terug viel. De grote vraag zal alleen wel zijn was de vroegere industie vergelijkbaar met de huidige industrie. Tijdens de grote depressie werkten bijvoorbeeld veel mensen op het land, en tegenwoordig kunnen we zelfs de landbouw al als een industrie beschouwen. En qau diensten kan ik me niet voorstellen dat die al zoveel in overvloed aanwezig waren tijden de grote depressie.

http://nl.wikipedia.org/wiki/Grote_Depressie

Als zelfs de Fed het zegt...quote:Huizenmarkt

Een grote transactie bij de Amerikaanse huizenbouwers: Pulte Homes (-10,5%) neemt sectorgenoot Centex (+18,9%) over voor $ 1,3 miljard in aandelen, op het moment van bieden een premie van 32,6%. Maar of de huizenmarkt de bodem heeft gezien is nog maar de vraag. Uit de notulen van de Fed FOMC vergadering van 18 maart bleek dat de leden niet verwachten dat de verbetering van de huizenmarktcijfers in februari het begin is van een nieuwe trend.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Money is short, times are hard, here's my fucking business card!

"I never let my schooling interfere with my education." — Mark Twain

"I never let my schooling interfere with my education." — Mark Twain

Heel interessant verhaal:

http://www.dnaindia.com/report.asp?newsid=1246649quote:Investors beware, 'tis a sucker's rally

Friday, April 10, 2009 3:25 IST

"The more I think about it, the more interesting it becomes that sentiment has turned bullish so quickly. When bear markets really bottom, sentiment is so negative that it really feels like the blood is not only in the streets, but that we are haemorrhaging from every orifice with nary a tourniquet in sight. That hasn't happened yet." --Richard Russell, one of the world's most revered investment letter writers, who has been publishing Dow Theory Letters since 1958

"You have become a scaremonger," she said.

"Yeah. But isn't one man's scaremonger another man's realist?" I asked.

"I was looking at some numbers and realised that most stock markets around the world have rallied big time since the beginning of March. Take the Bombay Stock Exchange Sensex, which has risen by more than 20%. The Dow Jones Industrial Average, the oldest stock index in the world, has given a return of 11% since the beginning of March. And here you are, going on and on as if the world is about to come to an end."

"Ever heard of a term called 'dead cat bounce'?" I asked.

"I thought we are discussing the stock market. Why are we suddenly talking about cats?"

"Let me explain. A dead cat bounce is a term used to describe rallies in a bear market. It comes from the notion that even a dead cat bounces if its falls from a great height. Most bear markets are characterised by these dead cat bounces. Take the Great Crash of the stock market that happened in October 1929 and which ultimately led to the Great Depression. Between 1929 and 1932, Dow fell by around 90%. But during that period, there were six rallies in which the stock market gave a return of more than 20%. Every time there was a renewed sense of optimism among the investors, but each time the rally went kaput and the market touched new lows."

"Rather interesting. But what makes investors get back into the market time and again?" she asked.

"I think it is a matter of hope. When everything was rallying, investors believed nothing could go wrong. That is why the world over stock markets went up and so did property prices. Over the last 15 months, the process has reversed. Stock markets have fallen with a thud, and so have property prices. But investors still have an iota of hope left in them. So every time stock prices go up a little, investors come up with stories that they tell themselves, to convince themselves that everything will be fine, and that the good old days will be back. The business media picks this up, and builds on it. If you have realised, anchors of business news channels have been smiling a lot more in the last few days."

"So what is the story investors are telling themselves this time around?"

"That combined government action will save the world, and its financial markets. The latest episode in this story is the meeting of the leaders of the Group of Twenty (G-20) which happened last week. They announced a $1.1 trillion stimulus for the International Monetary Fund (IMF) and other international institutions. This has made investors across the world happy. They don't realise that the financial meltdown has destroyed investment capital of around $50 trillion. So what difference is a little over a trillion dollars going to make? Also, as one journalist put it, 20 leaders of G-20 spent 220 minutes in London, discussing the crisis, which means each leader had precisely 11 minutes to put across his point of view."

"Eleven minutes?" she interrupted.

"Actually, it was much lesser, considering there were ten other leaders from organisations like the IMF, Association of South East Asian Nations and the Financial Stability Forum, etc also attending the meeting. So, there were thirty leaders and a total of 220 minutes to discuss the entire issue, which means a little over seven minutes per leader. Not a huge amount of time. Hence, expecting them to come out with anything substantial in such a short period of time would be outright foolish."

"What of the economy? Isn't that supposed to recover in the days to come?"

"Ultimately everything recovers; the question is --- when? That nobody really knows, and at best, the so-called experts are guessing. Let me give you the example of Japan. Exports for March are down 49% from the same time a year back. Exports to the US, Japan's largest trading partner, collapsed by 58.4%. Industrial production was down 9.4% in February and the economy contracted 12.1% in the first three months of the year. All this is forcing companies to cut jobs and salaries. Salaries have come down by 3.5% from a year back. Investors in Japan have ignored all the negative news and the Nikkei-225 index has rallied 17.8% since the beginning of March. They are betting on an export-led recovery in the second half of the year. The Japanese economy may be an extreme example, but the situation is no different in other parts of the world as well, with the economy contracting and massive job losses."

"You are scaring me even more now."

"Maybe, but that is the way I see it. Also, a point to remember is that as more and more people lose their jobs all over the world, there will be more loan defaults, and a further slowdown in spending, which will impact corporate profits. This, in turn, will lead to more job losses and a further slowdown in spending. An important point to remember is that till now, the United States has the main source of demand for the world economy. And the American consumer is clearly not in a mood to buy either goods or services right now."

"What are you hinting at?" she asked.

"Stock market performance ultimately rests on hopes of future corporate performance. And if investors don't buy goods and services, companies can't make profits. Meanwhile, investors are stuck with delusional optimism. By the time they come out of it, they would have lost a few dollars more. Or should I say rupees? P T Barnum, an American showman, once famously said, "There's a sucker born every minute." Rallies in bear markets are sucker's rallies. Now can you tell me what people who invest only on the basis of such rallies are called?"

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Deflatie in Zwitserland:

Riemen vast!quote:Swiss slide into deflation signals the next chapter of this global crisis

Watch Switzerland closely. It is tipping into deflation, the first Western country to succumb to Japan's disease.

By Ambrose Evans-Pritchard

Last Updated: 7:17PM BST 05 Apr 2009

Swiss consumer prices fell 0.4pc in March (year-on-year). Swiss CPI will be minus 1pc at least by July, nearing the level where spending psychology changes. By the time you have a self-feeding spiral, it is too late.

"This is something that we must prevent at all costs. The current situation is extraordinarily serious," said Philipp Hildebrand, a governor of the Swiss National Bank.

The SNB is not easily spooked. It is the world's benchmark bank, the keeper of the monetary flame. Yet even the SNB's hard men have thrown away the rule book, taking emergency action to force down the exchange rate of the Swiss franc.

Here lies the danger. If other countries try to export deflation by this means, we will face a second phase of the global crisis. Taiwan is already devaluing. Korea, Singapore, and Sweden all seem tempted to follow. Japan is chomping at the bit.

"We don't fully realise in the West what a catastrophic collapse Japan has suffered," says Albert Edwards, global strategist at Société Générale. "The West has dumped a large part of its economic downturn onto Japan by devaluing against the yen."

This is about to go into reverse as Tokyo hits the ping-pong ball back across the net. "As the unfolding collapse in the yen gathers pace, the West will see its green shoots incinerated to dust," he said.

Japan's industrial output fell 38pc in February (year-on-year), mostly concentrated into the last four months. No major economy imploded at this speed in the 1930s. The country has been hit by a double shock. As an export power it has taken the brunt of Anglo-Saxon belt-tightening: as the world's top creditor it is cursed by a "safe-haven" currency that soars in moments of danger – largely because the Japanese bring home their wealth till the storm passes. Normally, Japan can cope. This time, the yen's rise has pushed the economy over a cliff.

The yen must come back down to earth, and soon, or Japanese society will start to disintegrate. If necessary, the Bank of Japan will force it down by intervention, as occurred in 2003-2004.

Will China stand idly by as Japanese unleashes a shock to the global system through competitive devaluation? That depends whether you think China's spring recovery is the real thing, or an inventory build-up before the next downward slide. The Communist Party says 20m jobs have been lost since the bubble burst. This cannot be tolerated for long.

It is remarkable that China's fall into deflation has attracted so little notice. China's CPI was minus 1.6pc in February. The country has built too many factories producing goods that the world cannot absorb. The temptation is to shunt this excess capacity abroad. A faction of the politburo is already itching to devalue the yuan.

Of course, Britain has already played the currency card. That is different. The pound's fall, though welcome, is a side-effect of the Bank of England efforts to stem the credit crunch. There has been no currency intervention.

Crucially, Britain has a current account deficit. Many countries toying with devaluation are exporters with surpluses – 15.4pc of GDP for Singapore, 8.4pc for Switzerland, and 6.1pc for China. If these countries refuse to let their imbalances correct, world demand must implode.

Mr Hildebrand denies that the SNB is pursuing a "beggar-thy-neighbour' strategy. Like the yen, the franc suffers from the safe-haven curse: everybody buys it in a storm. This tightens monetary conditions. The SNB cannot easily offset this. It has already cut interest rates to near zero. There are not enough Swiss government bonds in the market to rely on the sort of "QE" asset purchases being carried out by the Bank.

Ultimately, I suspect this crisis may mark the moment when the Swiss franc loses its safe-haven role. Credit default swaps (CDS) measuring risk on five-year government debt have reached 127 for Switzerland, higher than Britain at 118. Norway has the world's lowest CDS at 48, reflecting its status as a petro-democracy.

Switzerland's banks are over-leveraged. Loans to emerging markets equal 50pc of GDP (half to Eastern Europe). Banking secrecy is dying. Fortunately for the Swiss, they have built up $700bn in net foreign assets for a rainy day. Improvident Britons are less lucky. But that is another story. What we risk now is a game of deflation "pass-the-parcel" worldwide. The economic establishment was caught off guard from 2003 to 2007 because it overlooked the way that Asia's unbalanced relationship with the West was feeding a credit bubble.

It may be caught again as the same warped structure leads to a chain of (panicked) devaluations.

Enjoy the "bear-trap" rally on global bourses this spring. But remember, we have only just begun to see the mass lay-offs and hardship caused by this slump. The politicians will act to save their skins. Markets may not like the result.

Nicht ärgern, nur wundern!

http://inflation.us/charts.html

Dow Jones Index

Adjusted for real inflation, the Dow Jones Index has actually lost much of its value since 1963.

Dow Jones Index

Adjusted for real inflation, the Dow Jones Index has actually lost much of its value since 1963.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

http://www.thedailyshow.com/video/index.jhtml?videoId=223883&title=Full-Metal-Budget

Heerlijk ook die media, zeggen dat er fors bezuinigd wordt, terwijl er daadwerkelijk 4% meer bijkomt.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy