WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

De Rabo probeert weer wat zieltjes te winnen:

quote:Rabobank waarschuwt voor teveel enthousiasmeDe Nederlandse economie heeft de ergste krimp achter de rug, maar de recessie is nog lang niet voorbij. De Nederlandse economie zal dit jaar niet met 4% maar met 6% krimpen. [...]

http://www.rtl.nl/(/finan(...)g_niet_voorbij_6.xml

"People that use Fiat currency as a store of value.

There is a name for it:

We call them Poor"

There is a name for it:

We call them Poor"

Zieltjes voor wat?

Ik in een aantal worden omschreven: Ondernemend | Moedig | Stout | Lief | Positief | Intuïtief | Communicatief | Humor | Creatief | Spontaan | Open | Sociaal | Vrolijk | Organisator | Pro-actief | Meedenkend | Levensgenieter | Spiritueel

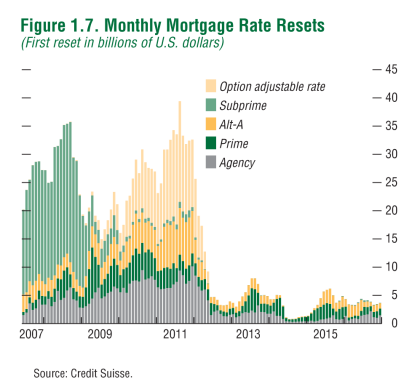

Bloemetjesbergquote:Option ARMs Threaten U.S. Housing Rebound as 2011 Resets Peak

June 11 (Bloomberg) -- Shirley Breitmaier’s mortgage payment started out at $98 when she refinanced her three-bedroom home in Galt, California, in 2007. The 73-year-old widow may see it jump to $3,500 a month in two years.

Breitmaier took out a payment-option adjustable rate mortgage, a loan popular during the housing boom for its low minimum payments before resetting at higher costs later.

About 1 million option ARMs are estimated to reset higher in the next four years, according to real estate data firm First American CoreLogic of Santa Ana, California. About three quarters of those loans will adjust next year and in 2011, with the peak coming in August 2011 when about 54,000 loans recast, the data show.

Option ARM borrowers hit with unaffordable monthly payments are another threat to the housing recovery and the economy, said Susan Wachter, a professor of real estate finance at the University of Pennsylvania’s Wharton School in Philadelphia. Owners who surrender properties to the bank rather than make higher payments for homes that have plummeted in value will further depress real estate prices and add to the inventory of properties on the market, she said.

“The option ARM recasts will drive up the foreclosure supply, undermining the recovery in the housing market,” Wachter said in an interview. “The option ARMs will be part of the reason that the path to recovery will be long and slow.”

Option ARM recasts will mean more pain for California, the state with the most foreclosures in the U.S.

$750 Billion Problem

More than $750 billion of option ARMs were originated in the U.S. between 2004 and 2008, according to data from First American and Inside Mortgage Finance of Bethesda, Maryland. California accounted for 58 percent of option ARMs, according to a report by T2 Partners LLC, citing data from Amherst Securities and Loan Performance.

Shirley Breitmaier took out a $315,000 option ARM to refinance a previous loan on her house.

Her payments started at 3/8 of 1 percent, or less than $100 a month, according to Cameron Pannabecker, the owner of Cal-Pro Mortgage and the Mortgage Modification Center in Stockton, California, who is working with Breitmaier. The loan allowed her to forgo higher payments by adding the unpaid balance to the principal. She’ll be required to start paying principal and interest to amortize the debt when the loan reaches 145 percent of the original amount borrowed.

Hoping for Help

Breitmaier, who has been in the home for 45 years and lives with her daughter, now fears she will lose the off-white stucco house that’s a hub for her family.

“I wish the government would bail us out like the banks and the car businesses,” she said. “I’d like to go from here to the grave next to my husband.”

Paul Financial LLC originated the loan and it was sold to GMAC, Pannabecker said.

“This loan is a perfect example front to back, bottom to top, of everything that has gone wrong over the last five to seven years,” Pannabecker said. “The consumer had a product pushed on them that they had no hope of understanding.”

GMAC is working with Breitmaier and will review all of her options, said Jeannine Bruin, a spokeswoman for the company. Bruin declined to be more specific, citing the firm’s customer confidentiality policy.

Inexpensive Payments

Peter Paul of Paul Financial, based in San Rafael, California, said he wasn’t familiar with Breitmaier’s loan agreement but disagreed with Pannabecker’s characterization.

“The problem is, real estate values went down,” Paul said. Paul said he’s winding down the company and hasn’t made any loans since the fall of 2007.

Option ARMs typically recast after five years and the lower payments can end before that time if the loan balance increases to 110 percent or 125 percent of the original mortgage, according to a Federal Reserve brochure on its Web site.

These home loans were primarily marketed to people with good credit scores, said Dirk van Dijk, director of research at Zacks Investment Research in Chicago. They were also sold to the elderly and immigrants who were lured by inexpensive payments, said Maeve Elise Brown, executive director of Housing and Economic Rights Advocates in Oakland, California.

Refinancing is impossible in many states given the nationwide drop in prices. In California, the median existing single-family home price dropped 37 percent in April to $256,700 from a year earlier, according to the state Association of Realtors.

Late Payments Soar

“Once you start amortizing that loan, the payment is going to shoot up,” said David Watts, a London-based strategist with research firm CreditSights.

The delinquency rate for payment-option ARMs originated in 2006 and bundled into securities is soaring, according to a May 5 report from Deutsche Bank AG. Over the past year, payments 60 days late or more on option ARMs originated in 2006 have almost doubled to 42.44 percent from 23.26 percent, Deutsche Bank said. For 2007 loans, the rate has climbed from 10.1 percent to 35.25 percent.

“We’re already seeing much higher levels of delinquencies of these option ARM loans even before you reach the point of the recast,” said Paul Leonard, the California director of the non- profit Center for Responsible Lending.

The threat of soaring payments has counselors at Housing and Economic Rights Advocates busy.

“There’s a level of hopelessness to the phone calls now,” said Brown.

We pakken 'm er weer bij:

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Voor zichzelf natuurlijk! Hoe meer angst ze zaaien, hoemeer mensen ze hopen die bij de 'veilige' rabobank gaan bankieren.quote:

"People that use Fiat currency as a store of value.

There is a name for it:

We call them Poor"

There is a name for it:

We call them Poor"

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

gelukkig, we zijn gered,quote:Op donderdag 11 juni 2009 16:28 schreef pberends het volgende:

Amerikanen geven weer meer uit

[ afbeelding ]

Epische faal dat Amerikaanse handelstekort.

Wat een misdadige constructies, dat verzin je gewoon niet...quote:[...] payments started at 3/8 of 1 percent, or less than $100 a month [...] The loan allowed her to forgo higher payments by adding the unpaid balance to the principal. She’ll be required to start paying principal and interest to amortize the debt when the loan reaches 145 percent of the original amount borrowed.

Lekker <$100/m betalen voor de eerste 5 jaar or so, en dan zitten met een hypotheek van 145% van je OUDE gebubbelde huiswaarde, tegen het lange rente tarief van 2011

Can you say fucked...

Ik in een aantal worden omschreven: Ondernemend | Moedig | Stout | Lief | Positief | Intuïtief | Communicatief | Humor | Creatief | Spontaan | Open | Sociaal | Vrolijk | Organisator | Pro-actief | Meedenkend | Levensgenieter | Spiritueel

Misdadig is 1 stap, er instappen is toch echt stap 2.quote:Op donderdag 11 juni 2009 19:29 schreef eleusis het volgende:

[..]

Wat een misdadige constructies, dat verzin je gewoon niet...

Lekker <$100/m betalen voor de eerste 5 jaar or so, en dan zitten met een hypotheek van 145% van je OUDE gebubbelde huiswaarde, tegen het lange rente tarief van 2011

Can you say fucked...

People once tried to make Chuck Norris toilet paper. He said no because Chuck Norris takes crap from NOBODY!!!!

Megan Fox makes my balls look like vannilla ice cream.

Megan Fox makes my balls look like vannilla ice cream.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

quote:Op vrijdag 12 juni 2009 14:04 schreef pberends het volgende:

Wouter Bos komt met Stopdecrisis.nl

Epische faal die Bos. The crisis has just been started.

http://www.telegraaf.nl/s(...)oomreis__.html?p=5,1quote:Op vrijdag 12 juni 2009 14:16 schreef Bolkesteijn het volgende:

[..]

Wat mij betreft een nieuw dieptepunt in de kredietcrisis.

Ze weten er wel een positieve draai aan te geven

---

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

And when the leaves fall the land looks more human

it's got me questioning the essence of my farm boy blues

hence, I never wore the fashions of the know-what-I'm-doin'

Haha, ja maak even lekker je laatste spaarcentjes op als je ontslagen bent en doe alsof er niets aan de hand is. Slim.quote:Op vrijdag 12 juni 2009 14:32 schreef Zero2Nine het volgende:

[..]

http://www.telegraaf.nl/s(...)oomreis__.html?p=5,1

Ze weten er wel een positieve draai aan te geven

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

quote:Op vrijdag 12 juni 2009 15:15 schreef pberends het volgende:

[..]

Haha, ja maak even lekker je laatste spaarcentjes op als je ontslagen bent en doe alsof er niets aan de hand is. Slim.

quote:Veenman hoopt dat het einde van de crisis in zicht is bij thuiskomst. Veel zorgen maakt ze zich in ieder geval niet. „Ik hoop dat de arbeidsmarkt weer wat aantrekt en dat ik meer kans heb op een leuke baan in november. Ik ben te ambitieus om genoegen te nemen met een baan die me niet trekt.”

Epic fail.

For great justice!

Pff, de ellende op de arbeidsmarkt moet nog beginnen. Minimaal een verdubbeling van het aantal werklozen vanaf het huidige niveau, waarschijnlijk het driedubbele.quote:

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

3,1%quote:12-06-2009 15:55:00 VS inflatieverwachting 5-jaar juni +3,1% Vs +2,9% in mei

12-06-2009 15:55:00 VS inflatieverwachting 12-maanden juni +3,1% Vs +2,8% in mei

12-06-2009 15:55:00 VS consumentenvertrouwen mid-juni 69,0 Vs 68,7 in mei

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Ook dit zinnetje:quote:

[..]

Pff, de ellende op de arbeidsmarkt moet nog beginnen. Minimaal een verdubbeling van het aantal werklozen vanaf het huidige niveau, waarschijnlijk het driedubbele.

Benieuwd hoe lang ze dat vol gaat houden.quote:Ik ben te ambitieus om genoegen te nemen met een baan die me niet trekt.

For great justice!

"Bernanke is a economic criminal and Geithner a dishonest person"

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Epische faal dat RTL Z:

http://www.rtl.nl/(/finan(...)2_1030_vix_daalt.xml

Optiebeleggers: de kredietcrisis is voorbij

Ging Letland vandaag niet bijna failliet?

http://www.rtl.nl/(/finan(...)2_1030_vix_daalt.xml

Optiebeleggers: de kredietcrisis is voorbij

Ging Letland vandaag niet bijna failliet?

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Ik heb je ook wel eens anders horen zeggen peterquote:

People once tried to make Chuck Norris toilet paper. He said no because Chuck Norris takes crap from NOBODY!!!!

Megan Fox makes my balls look like vannilla ice cream.

Megan Fox makes my balls look like vannilla ice cream.

Een mooie tijd voor Amerikanen om te sparen, en kut als je schulden/ een hypotheek hebt

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

dat noemen we een Woutertjequote:Op vrijdag 12 juni 2009 18:59 schreef sitting_elfling het volgende:

[..]

Ik heb je ook wel eens anders horen zeggen peter

ik wil best een post verzinnen met epic fail erin, maar ik vind het een k*t mode woord. Shit doe ik het toch.

mooi met 9% werklozen en een krimp van 6% zo een hoog vertrouwen

quote:vr 12 jun 2009, 16:13

Consumentenvertrouwen VS hoogst in 9 maanden

ANN ARBOR (AFN) - Het Amerikaanse consumentenvertrouwen is in juni gestegen tot een stand van 69 van 68,7 in mei. Het consumentenvertrouwen in de Verenigde Staten staat daarmee op het hoogste niveau in negen maanden. Dat blijkt uit voorlopige cijfers van de universiteit van Michigan die vrijdag werden gepubliceerd.

Amerikanen blijven heerlijk. Ze hebben nog steeds een groot handelstekort. Dat kan maar 2 dingen betekenen:quote:Op zaterdag 13 juni 2009 03:20 schreef henkway het volgende:

mooi met 9% werklozen en een krimp van 6% zo een hoog vertrouwen

[..]

- Of de dollar zal zwakker en zwakker worden (wanneer zij doorgaan met overconsumeren)

- Of ze laten een diepere recessie toe om het handelstekort op te lossen

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Ze zullen vanaf nu zelf de bonds moeten opkopen en de US banken en US pensioenfondsen hehbben er ook geen geld voor en de belastinginkomsten deze maan zijn desastreus/quote:Op zaterdag 13 juni 2009 10:01 schreef pberends het volgende:

[..]

Amerikanen blijven heerlijk. Ze hebben nog steeds een groot handelstekort. Dat kan maar 2 dingen betekenen:

- Of de dollar zal zwakker en zwakker worden (wanneer zij doorgaan met overconsumeren)

- Of ze laten een diepere recessie toe om het handelstekort op te lossen

Dat de US bonds gaat uitgeven in RMB lijkt me ook niet, daaruit blijkt wel de zeer zwakke positie van de dollar

It 's only a matter of time

goede moment voor een hypotheeklening in dollars

daar zeg je wat. Alhoewel IJslanders en Letten dat ook dachten toen ze een lening in euro aangingen.....quote:Op zaterdag 13 juni 2009 10:25 schreef henkway het volgende:

goede moment voor een hypotheeklening in dollars

Fluctueert een hoop zeg.quote:Op vrijdag 12 juni 2009 20:33 schreef SeLang het volgende:

Een mooie tijd voor Amerikanen om te sparen, en kut als je schulden/ een hypotheek hebt

[ afbeelding ]

Rusland: dollar blijft wereldreservemunt

quote:Kudrin tegenover persagentschap Bloomberg na de G8-top van maandag: "Natuurlijk hebben wij nog vertrouwen in de Amerikaanse dollar... de Amerikaanse economie is een van de leidende economiën in de wereld, en de fundamentals van de VS zijn in uiterst gezonde staat."

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy