WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

http://tegenlicht.vpro.nl(...)2/evgenymorozov.htmlquote:Evgeny Morozov: het einde van de internet-utopie

Het Internet als bevrijdende kracht richting democratie. Evgeny Morozov, schrijver van The Net Delusion vindt dit een valse voorstelling van zaken. Hij neemt plaats in een visuele arena met twaalf schermen, waarin hij wordt gebombardeerd met beelden en quotes.

Sinds de Arabische revoluties wordt aan de bevrijdende rol van het Internet een grote rol toegekend. Sociale media worden gezien als het nieuwe wapen bij het omverwerpen van dictaturen. Evgeny Morozov, de 27-jarige Wit-Russische schrijver van "The Net Delusion", bestrijdt dit ongebreidelde cyber-utopisme en laat zien dat autoritaire regimes het Internet juist gebruiken om verzet de kop in te drukken.

Opmerkelijk is dat Morozov voorheen zelf het internet inzette ter verspreiding van democratische idealen, met name in de Oost-Europese landen. Maar hij raakte diep teleurgesteld en ontpopte zich als één van de meest vooraanstaande critici van de interneteuforie. Net als overal gebruiken de meeste mensen onder een dictatuur het internet niet om de samenleving te veranderen of om ideeën rond democratie te verspreiden, maar juist om hun moeilijke bestaan te ontvluchten en online spelletjes te spelen of porno te bekijken, aldus Morozov.

Tegenlicht geeft deze dwarse visie ruimte. We vroegen de jonge Wit-Rus om plaats te nemen in een arena waarin hij wordt omringd door videoschermen. In deze setting - die hij zelf omschrijft als een panopticum - wordt hij gebombardeerd met quotes en beelden uit eerdere uitzendingen. Er zijn onder meer fragmenten van de onlangs in China opgepakte en vrijgelaten kunstenaar Ai Weiwei, de toespraak over Internetvrijheid van Hillary Clinton, de jonge Egyptische activiste Farida Makar en WikiLeaks-voorman Julian Assange. Morozovs reactie op de aan hem gepresenteerde dilemmas leidt tot een levendige dialoog tussen beeld en inhoud, waarin hij ons meeneemt in zijn strijd tegen het blinde cyber-utopisme.

http://beta.uitzendinggemist.nl/afleveringen/1112074

Wel een interessante Tegenlicht-uitzending, die ook over economie, sociale zekerheid en commercie gaat.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Ik vond hem wel heel erg negatief, soms had ik het gevoel dat hij negatief was omdat hij daarvoor ingehuurd was.quote:Op donderdag 6 oktober 2011 15:59 schreef pberends het volgende:

[..]

http://tegenlicht.vpro.nl(...)2/evgenymorozov.html

http://beta.uitzendinggemist.nl/afleveringen/1112074

Wel een interessante Tegenlicht-uitzending, die ook over economie, sociale zekerheid en commercie gaat.

1/10 Van de rappers dankt zijn bestaan in Amerika aan de Nederlanders die zijn voorouders met een cruiseschip uit hun hongerige landen ophaalde om te werken op prachtige plantages.

"Oorlog is de overtreffende trap van concurrentie."

"Oorlog is de overtreffende trap van concurrentie."

Ja idd, alleen al 't feit dat dit artikel op bijvoorbeeld Fok! wordt gepost en bediscussieerd zou 'm al wat positiever moeten stemmen.quote:Op donderdag 6 oktober 2011 16:07 schreef icecreamfarmer_NL het volgende:

[..]

Ik vond hem wel heel erg negatief, soms had ik het gevoel dat hij negatief was omdat hij daarvoor ingehuurd was.

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

quote:Britain in grip of worst ever financial crisis, Bank of England governor fears

Sir Mervyn King expressed fears that Britain is in the grip of the world's worst ever financial crisis after the Bank of England announced it was injecting £75bn into the ailing economy.

The Bank's governor said the UK was suffering from a 1930s-style shortage of money and needed a second dose of quantitative easing to boost demand and prevent inflation falling too low.

Britain's first dose of quantitative easing, also known as QE1, was in 2009/10, with £200bn being injected into the economy. Labour said the launch of QE2 was an admission that the government's economic policy had failed.

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

quote:Moody’s verlaagt kredietwaardigheid Britse banken

Kredietbeoordelaar Moody’s heeft de kredietwaardigheid van twaalf Britse financiële instellingen verlaagd. Dat maakte het kredietagentschap vanochtend bekend.

Onder de twaalf instellingen die zijn afgewaardeerd zitten grote banken en verzekeraars als Royal Bank of Scotland, Lloyds en de Britse vestiging van de Spaanse bank Santander. Moody’s zegt de instellingen te moeten afwaarderen omdat het volgens de kredietbeoordelaar minder waarschijnlijk is dat de Britse overheid de instellingen steunt als ze in de financiële problemen komen. “Bekendmakingen en daden van de Britse autoriteiten hebben de waarschijnlijkheid van steun op de middellange en lange termijn significant verkleind”, aldus Moody’s.

De afwaardering van de Britse banken door Moody’s komt niet doordat het heel slecht met de Britse banken gaat, legt onze correspondent in Londen Titia Ketelaar uit:

“De reden van de afwaardering is dat Moody’s denkt dat de Britse regering in de toekomst minder geneigd is de banken te steunen als ze weer in de problemen komen. Het is niet zo dat hun kredietwaardigheid nu in het geding is, het is meer een waarschuwing. De situatie van de Britse banken is niet te vergelijken met de situatie van banken in andere Europese landen.”

De Britse minister van Financiën George Osborne zei in een reactie tegenover de BBC dat hij het volste vertrouwen heeft dat het goed zit met het kapitaal van de Britse banken. Hij benadrukte dat de Britse regering stappen neemt om te voorkomen dat het in de toekomst nodig is om opnieuw staatssteun aan banken te geven.

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

heeeeeeej, de buurtjes waren op tvquote:

'Economische groei is als kanker'

Zo kun je het ook zien.

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

1/10 Van de rappers dankt zijn bestaan in Amerika aan de Nederlanders die zijn voorouders met een cruiseschip uit hun hongerige landen ophaalde om te werken op prachtige plantages.

"Oorlog is de overtreffende trap van concurrentie."

"Oorlog is de overtreffende trap van concurrentie."

Link naar de buren: CEO Dexia logeert al drie jaar in Brussels tophotel Amigo

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Even ter aandacht.

In de afgelopen 7 posts tel ik 4 posts met linkjes naar andere websites. Dat is niet de bedoeling. Als de website waar je naar toe linkt een artikel bevat moet je het artikel ook gewoon in je post plaatsen. Is het een video, vermeldt dan op zijn minst wat er te zien is en waarom dat interessant is.

En pberends, AEX is geen uithangbord voor je FP artikelen. Als users de Frontpage willen raadplegen kunnen ze dat op eigen gelegenheid doen.

Deze reeks is eigenlijk al ingehaald door de problemen in de EU. Ik zie dit meer als SC. Soort van Max Keiser reeks. En dan moet je wat dingen (durven) loslaten.quote:Op woensdag 12 oktober 2011 00:52 schreef Bolkesteijn het volgende:

[info]Even ter aandacht.[/info]

In de afgelopen 7 posts tel ik 4 posts met linkjes naar andere websites. Dat is niet de bedoeling. Als de website waar je naar toe linkt een artikel bevat moet je het artikel ook gewoon in je post plaatsen. Is het een video, vermeldt dan op zijn minst wat er te zien is en waarom dat interessant is.

En pberends, AEX is geen uithangbord voor je FP artikelen. Als users de Frontpage willen raadplegen kunnen ze dat op eigen gelegenheid doen.

China Blowback topic..... plz.quote:

http://www.tagesschau.de/ausland/weltspiegelchina108.html

Waar het om gaat is dat je daarmee voorkomt dat je een topic met dode linkjes hebt straks. Artikelen veranderen wel eens van URL of worden na verloop van tijd in een betaald deel van een website geplaatst.quote:

Deze reeks is eigenlijk al ingehaald door de problemen in de EU. Ik zie dit meer als SC. Soort van Max Keiser reeks. En dan moet je wat dingen (durven) loslaten.

Ik klikker... maar dat valt reuze mee, we krijgen wel een context verschuiving... Dit was eens een ground zero reeks. Nu hebben we rugnummers bij gelijklopende topics.quote:Op woensdag 12 oktober 2011 02:06 schreef Bolkesteijn het volgende:

[..]

Waar het om gaat is dat je daarmee voorkomt dat je een topic met dode linkjes hebt straks. Artikelen veranderen wel eens van URL of worden na verloop van tijd in een betaald deel van een website geplaatst.

Lees ook de commentsquote:Bloomberg: Wall Street Sees ‘No Exit’ From Financial Decline as Bankers Fret Future

Wall Street executives, facing demonstrators camped for a fourth week in New York’s financial district, say they’re anxious and angry for other reasons.

An era of decline and disappointment for bankers may not end for years, according to interviews with more than two dozen executives and investors. Blaming government interference and persecution, they say there isn’t enough global stability, leverage or risk appetite to triumph in the current slump.

“I don’t think it’s a time to make money -- this is a time to rig for survival,” said Charles Stevenson, 64, president of hedge fund Navigator Group Inc. and head of the co-op board at 740 Park Ave. The building, home to Blackstone Group LP Chairman Stephen Schwarzman and CIT Group Inc. Chief Executive Officer John Thain, was among those picketed by protesters yesterday. “The future is not going to be like a past we knew,” he said. “There’s no exit from this morass.”

[ Bericht 4% gewijzigd door Perrin op 13-10-2011 08:41:31 ]

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

Move Your Money

The Move Your Money project is a nonprofit campaign that encourages individuals and institutions to divest from the nation's largest Wall Street banks and move to local financial institutions.

Little has changed to prevent another financial crisis or to end 'Too Big To Fail,' and with Congress unwilling to act, we are encouraging individuals to take power into their own hands by voting with their dollars and no longer contributing to a financial system that has led our country astray.

We are a campaign that gives people real, concrete actions they can take to create a more sane, stable and localized banking system.

The Move Your Money project is a nonprofit campaign that encourages individuals and institutions to divest from the nation's largest Wall Street banks and move to local financial institutions.

Little has changed to prevent another financial crisis or to end 'Too Big To Fail,' and with Congress unwilling to act, we are encouraging individuals to take power into their own hands by voting with their dollars and no longer contributing to a financial system that has led our country astray.

We are a campaign that gives people real, concrete actions they can take to create a more sane, stable and localized banking system.

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Eindelijk iets wat enig effect kan sorteren (want een beetje kamperen nabij WS, haalt echt niks).quote:Op zaterdag 15 oktober 2011 19:46 schreef Aether het volgende:

Move Your Money

The Move Your Money project is a nonprofit campaign that encourages individuals and institutions to divest from the nation's largest Wall Street banks and move to local financial institutions.

Little has changed to prevent another financial crisis or to end 'Too Big To Fail,' and with Congress unwilling to act, we are encouraging individuals to take power into their own hands by voting with their dollars and no longer contributing to a financial system that has led our country astray.

We are a campaign that gives people real, concrete actions they can take to create a more sane, stable and localized banking system.

Please Move The Deer Crossing Sign

Nederlandse economie niet conform EU-eisen

AMSTERDAM - Nederland wijkt af van de Europese normen die zijn gesteld om economische misstanden op te sporen. Dat blijkt volgens het Financieele Dagblad uit een overzicht dat het kabinet heeft opgesteld.

Op verzoek van VVD-Kamerlid Mark Harbers hebben minister Maxime Verhagen van Economische Zaken en Jan Kees de Jager van Financiën onder elkaar gezet hoe Nederland de afgelopen tien jaar scoorde op de negen indicatoren die de Europese Commissie heeft opgesteld om macro-economische onevenwichtigheden op te sporen.

Uit het overzicht blijkt dat Nederland kampt met zowel een te hoge private- als overheidsschuld. Ook de zeer hoge hypotheekschuld is niet conform de Europese eisen.

Verhagen reageerde vanochtend met een brief in de Volkskrant op de uitkomsten. Hij schrijft dat Europa naar aanleiding van de eurocrisis meer op economisch beleid moet coördineren: "Nu concentreert de discussie zich vooral op strengere naleving van de begrotingsregels", aldus Verhagen. "Maar dit is niet meer dan een symptoom van de crisis. De oorzaak ligt dieper. Het gaat niet alleen om gezonde begrotingen, maar vooral ook om gezonde economieën."

AMSTERDAM - Nederland wijkt af van de Europese normen die zijn gesteld om economische misstanden op te sporen. Dat blijkt volgens het Financieele Dagblad uit een overzicht dat het kabinet heeft opgesteld.

Op verzoek van VVD-Kamerlid Mark Harbers hebben minister Maxime Verhagen van Economische Zaken en Jan Kees de Jager van Financiën onder elkaar gezet hoe Nederland de afgelopen tien jaar scoorde op de negen indicatoren die de Europese Commissie heeft opgesteld om macro-economische onevenwichtigheden op te sporen.

Uit het overzicht blijkt dat Nederland kampt met zowel een te hoge private- als overheidsschuld. Ook de zeer hoge hypotheekschuld is niet conform de Europese eisen.

Verhagen reageerde vanochtend met een brief in de Volkskrant op de uitkomsten. Hij schrijft dat Europa naar aanleiding van de eurocrisis meer op economisch beleid moet coördineren: "Nu concentreert de discussie zich vooral op strengere naleving van de begrotingsregels", aldus Verhagen. "Maar dit is niet meer dan een symptoom van de crisis. De oorzaak ligt dieper. Het gaat niet alleen om gezonde begrotingen, maar vooral ook om gezonde economieën."

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Private schulden 223% van het bbp. Gelukkig maakt de VVD zich meer zorgen om de 63% overheidsschuld

.

.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Hoeveel bezit staat er tegenover de private schuld? Dat is natuurlijk wel een vraag die van belang is. Bij de overheid speelt dat niet, want de overheid heeft geen bezit wat zomaar even verkocht kan worden bij liquidatie en kent alleen een overzicht van inkomsten en uitgaven.

Steeds minder, de pensioenen verdampen en de huizenprijs gaat omlaagquote:

Hoeveel bezit staat er tegenover de private schuld? Dat is natuurlijk wel een vraag die van belang is. Bij de overheid speelt dat niet, want de overheid heeft geen bezit wat zomaar even verkocht kan worden bij liquidatie en kent alleen een overzicht van inkomsten en uitgaven.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

quote:Op maandag 17 oktober 2011 17:50 schreef JimmyJames het volgende:

Ja maar hypotheekaftrekrente voor the wins. De VVD

Populistisch geblaat. Met de VVD valt best over verlaging van de HRA te praten, maat dan moeten de voorwaarden natuurlijk wel interessant zijn voor de VVD. Zolang PvdA, D66 en andere linkse partijen vast blijven houden aan enkel het afschaffen van de HRA en niet het equivalent verlagen van de belastingen is het voor de VVD natuurlijk totaal niet interessant om daar mee in te stemmen.quote:Op maandag 17 oktober 2011 18:16 schreef pberends het volgende:

Private schulden 223% van het bbp. Gelukkig maakt de VVD zich meer zorgen om de 63% overheidsschuld

De pensioenen verdampen helemaal niet, en de huizenprijzen waren belachelijk veel gestegen.quote:

Steeds minder, de pensioenen verdampen en de huizenprijs gaat omlaag.

Dat zeg je wel erg stellig.quote:

[..]

De pensioenen verdampen helemaal niet.

Ik zit bij een van de betere pensioenfondsen en die hebben CAO loonstijgingen al 3 jaar niet meegenomen en voor de gepensioneerden niet geindexeerd.

Al met al is er cumulatief in 3 jaar een procent of 10 aan (toekomstige) koopkracht verdampt.

Ik heb geen inzicht in de ontwikkelingen bij andere fondsen maar het lijkt me vrij veilig om aan te nemen dat daar minimaal hetzelfde of meer is verdampt.

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Verrassend dat je de VVD verdedigt.quote:

Populistisch geblaat. Met de VVD valt best over verlaging van de HRA te praten, maat dan moeten de voorwaarden natuurlijk wel interessant zijn voor de VVD. Zolang PvdA, D66 en andere linkse partijen vast blijven houden aan enkel het afschaffen van de HRA en niet het equivalent verlagen van de belastingen is het voor de VVD natuurlijk totaal niet interessant om daar mee in te stemmen.

Vanuit een politiek tactisch oogpunt valt het natuurlijk wel te verdedigen. Echter is het gewoon slecht voor Nederland dat de huizenbubbel zo ver is opgeblazen mede door de HRA.

Please Move The Deer Crossing Sign

Vertel dat maar aan de VVD en de pensioenfondsen.quote:

[..]

De pensioenen verdampen helemaal niet, en de huizenprijzen waren belachelijk veel gestegen.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Onzin, ook die partijen weten dat daar andere belastingverlagingen tegenover moeten staan.quote:

[..]

[..]

Populistisch geblaat. Met de VVD valt best over verlaging van de HRA te praten, maat dan moeten de voorwaarden natuurlijk wel interessant zijn voor de VVD. Zolang PvdA, D66 en andere linkse partijen vast blijven houden aan enkel het afschaffen van de HRA en niet het equivalent verlagen van de belastingen is het voor de VVD natuurlijk totaal niet interessant om daar mee in te stemmen.

De andere partijen zijn niet gek.

1/10 Van de rappers dankt zijn bestaan in Amerika aan de Nederlanders die zijn voorouders met een cruiseschip uit hun hongerige landen ophaalde om te werken op prachtige plantages.

"Oorlog is de overtreffende trap van concurrentie."

"Oorlog is de overtreffende trap van concurrentie."

Dit verschijnsel noemt men stagflatie, inflatie zonder extra bestedingsruimte, ofwel, we worden allemaal armer, jaar na jaarquote:

[..]

Dat zeg je wel erg stellig.

Ik zit bij een van de betere pensioenfondsen en die hebben CAO loonstijgingen al 3 jaar niet meegenomen en voor de gepensioneerden niet geindexeerd.

Al met al is er cumulatief in 3 jaar een procent of 10 aan (toekomstige) koopkracht verdampt.

Ik heb geen inzicht in de ontwikkelingen bij andere fondsen maar het lijkt me vrij veilig om aan te nemen dat daar minimaal hetzelfde of meer is verdampt.

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

Alles staat met alles in verbinding: de eurocrisis in grafieken

Hoeveel schulden heeft een land en aan wie is het geld verschuldigd?

Wanneer er geen preventieve maatregelen worden getroffen, kan dit het gevolg zijn

Het risico van besmetting

Hoeveel schulden heeft een land en aan wie is het geld verschuldigd?

Wanneer er geen preventieve maatregelen worden getroffen, kan dit het gevolg zijn

Het risico van besmetting

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Wat een flutdiagrammen (nofiquote:

Alles staat met alles in verbinding: de eurocrisis in grafieken

Hoeveel schulden heeft een land en aan wie is het geld verschuldigd?

[ afbeelding ]

Wanneer er geen preventieve maatregelen worden getroffen, kan dit het gevolg zijn

[ afbeelding ]

Het risico van besmetting

[ afbeelding ]

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Ik zal je alvast een conclusie geven van de getuigenis van de beide heren:quote:Op woensdag 2 november 2011 15:16 schreef Aether het volgende:

Balkenende en Bos worden verhoord over kredietcrisis

"We kunnen het ons niet meer zo goed herinneren, maar met de kennis van nu zouden we het anders hebben aangepakt"

quote:Subprime moment looms for ‘risk-free’ sovereign debt

When future financial historians look back at the early 21st century, they may wonder why anybody ever thought it was a good idea to repackage subprime securities into triple A bonds. So, too, in relation to assumptions about the “risk-free” status of western sovereign debt.

After all, during most of the past few decades, it has been taken as a key axiom of investing that most western sovereign debt was in effect risk-free, and thus expected to trade at relatively undifferentiated tight spreads. Now, of course, that assumption is being exposed as a fallacy. Just look at those Greek haircuts, or the scale of future losses now being implied in the credit derivatives markets for Portugal, Ireland and Italy.

As the turmoil in the eurozone spreads, forcing a paradigm shift for investors, the intriguing question now is whether we are on the verge of a paradigm shift in the regulatory and central bank world, too. After all, it is not just investors who have tended to assume that mainstream sovereign bonds are risk-free; this assumption has also acted as a pillar of the entire regulatory structure, and many central bank operations.

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

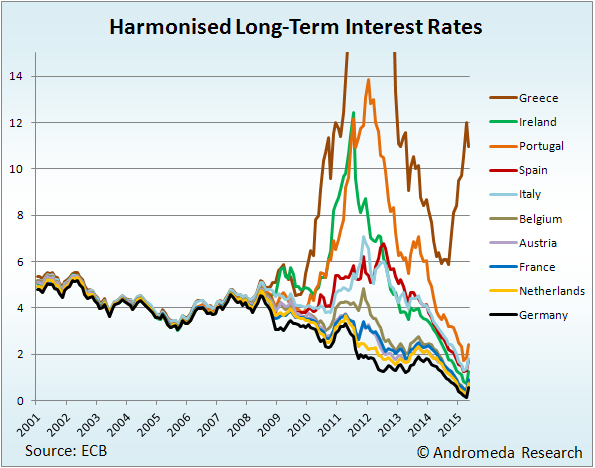

Ja de "risk free" rates lopen tegenwoordig lekker uit elkaar

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Wat hebben die banken enorm zitten slapen tot 2007, als het gaat om leningen aan Grieken en ander onbetrouwbaar volk.

Good intentions and tender feelings may do credit to those who possess them, but they often lead to ineffective — or positively destructive — policies ... Kevin D. Williamson

Amerikanen bedoel je dan zeker. Al die bagger die we door dat onbetrouwbare volk in de maag hebben laten splitsen...quote:

Wat hebben die banken enorm zitten slapen tot 2007, als het gaat om leningen aan Grieken en ander onbetrouwbaar volk.

Oudje:quote:

[..]

Amerikanen bedoel je dan zeker. Al die bagger die we door dat onbetrouwbare volk in de maag hebben laten splitsen...

When the student is ready, the teacher will appear.

When the student is truly ready, the teacher will disappear.

When the student is truly ready, the teacher will disappear.

Ja, je financiert een woning met een hypotheek van 100%, maar toch is het "bezitsvorming" (nee, lees: je huurt een huis van de bank). Als vervolgens de prijzen sterk dalen (omdat er veel lucht in de huizenprijzen zit door o.a. de hypotheekrenteaftrek), blijf je over met een restschuld / hypotheek die onder water staat (Mooi appeltje voor de dorst, Mark!).quote:Rutte: Hypotheekschuld geen probleem

Volgens minister-president Mark Rutte is de Nederlandse hypotheekschuld van 645 miljard euro, die 104 procent van het Nederlandse bruto binnenlands product (bbp) bedraagt en daarmee de hoogste ter wereld is, geen probleem. Dit zei de VVD-premier vrijdag in Nieuwsuur.

Klaas Knot, de president van De Nederlandsche Bank (DNB), waarschuwde eerder deze week dat de hoge hypotheekschulden een bedreiging zijn voor de financiële stabiliteit van Nederland. Knot wil dan ook de hypotheekrenteaftrek hervormen.

Rutte vindt echter dat de DNB-president onzin vertelt: "Ik ben het niet met hem eens. Kern hier is: ja, er is veel hypotheekschuld in Nederland, maar daar staan ook huizen tegenover; bezit. Gewoon de stenen; het is niet een vakantie waar je voor leent, waarmee de waarde kwijt is, maar er staat bezit tegenover. We hebben in Nederland ook zo'n 700 miljard in de pensioenpotten zitten. We hebben dus ook heel erg veel besparingen."

Aan de hypotheekrenteaftrek wil de premier dan ook helemaal niet komen: "De hypotheekrenteaftrek is er met een doel: namelijk bezitsvorming stimuleren. Het is goed als mensen een eigen huis hebben. Ook is de hypotheekrenteaftrek een correctie op te hoge belastingen."

En waarom loopt de VVD dan altijd zo te zeiken op de hoge belastingen in Nederland? Schijnbaar worden die goed gecompenseerd door de HRA. Maar nee hoor, elke keer zeuren over dat 52%-tarief.quote:Aan de hypotheekrenteaftrek wil de premier dan ook helemaal niet komen: "De hypotheekrenteaftrek is er met een doel: namelijk bezitsvorming stimuleren. Het is goed als mensen een eigen huis hebben. Ook is de hypotheekrenteaftrek een correctie op te hoge belastigen."

[ Bericht 7% gewijzigd door pberends op 05-11-2011 15:04:39 ]

President Camacho

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

TV series: Boardwalk Empire | Burn Notice | Dexter | Game of Thrones | Impractical Jokers | Luther | Sherlock | Sons of Anarchy

En dat soort mensen besturen het land ; Ik zeg.. met hooivorken en fakkels die gasten oppakken en voor justitie gooien voor het oplichten van 16 miljoen nederlanders. En ja hoor - Heel veel financiele instanties waarschuwen nederland voor dit probleem maar mark rutte denkt het allemaal beter te weten. De IMF en dergelijke vertellen allemaal onzin - Als je een hypotheek afsluit is het huis meteen van jou volgens mark.. Zeg dat maar tegen de bankenquote:

[..]

Ja, je financiert een woning met een hypotheek van 100%, maar toch is het "bezitsvorming" (nee, lees: je huurt een huis van de bank). Als vervolgens de prijzen sterk dalen (omdat er veel lucht in de huizenprijzen zit door o.a. de hypotheekrenteaftrek), blijf je over met een restschuld / hypotheek die onder water staat (Mooi appeltje voor de dorst, Mark!).

[..]

En waarom loopt de VVD dan altijd zo te zeiken op de hoge belastingen in Nederland? Schijnbaar worden die goed gecompenseerd door de HRA. Maar nee hoor, elke keer zeuren over dat 52%-tarief.

quote:Economy Hitting Stall Speed Because of Debt: El-Erian

Policymakers have taken the wrong approach in dealing with the global economy's numerous problems, shuffling debt around while avoiding making difficult decisions, Pimco's Mohamed El-Erian said.

"We used all of the wrong bullets," the co-CEO for the largest bond fund in the world told CNBC. "We tried to throw money at the problem. The issue is not money, the issue is that what we have are structural impediments and structural challenges need structural solutions.

Five problems confront the U.S. economy, he said: Housing, unemployment, public finances, infrastructure and clogged credit markets.

"Until we get movement on those five things, we're at stall speed," he said.

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

quote:Roubini: Down with the Eurozone

The eurozone crisis seems to be reaching its climax, with Greece on the verge of default and an inglorious exit from the monetary union, and now Italy on the verge of losing market access. But the eurozone's problems are much deeper. They are structural, and they severely affect at least four other economies: Ireland, Portugal, Cyprus, and Spain. For the last decade, the PIIGS (Portugal, Ireland, Italy, Greece, and Spain) were the eurozone's consumers of first and last resort, spending more than their income and running ever-larger current-account deficits. Meanwhile, the eurozone core (Germany, the Netherlands, Austria, and France) comprised the producers of first and last resort, spending below their incomes and running ever-larger current-account surpluses.

These external imbalances were also driven by the euro’s strength since 2002, and by the divergence in real exchange rates and competitiveness within the eurozone. Unit labor costs fell in Germany and other parts of the core (as wage growth lagged that of productivity), leading to a real depreciation and rising current-account surpluses, while the reverse occurred in the PIIGS (and Cyprus), leading to real appreciation and widening current-account deficits. In Ireland and Spain, private savings collapsed, and a housing bubble fueled excessive consumption, while in Greece, Portugal, Cyprus, and Italy, it was excessive fiscal deficits that exacerbated external imbalances.

The resulting build-up of private and public debt in over-spending countries became unmanageable when housing bubbles burst (Ireland and Spain) and current-account deficits, fiscal gaps, or both became unsustainable throughout the eurozone's periphery. Moreover, the peripheral countries’ large current-account deficits, fueled as they were by excessive consumption, were accompanied by economic stagnation and loss of competitiveness.

So, now what?

Symmetrical reflation is the best option for restoring growth and competitiveness on the eurozone's periphery while undertaking necessary austerity measures and structural reforms. This implies significant easing of monetary policy by the European Central Bank; provision of unlimited lender-of-last-resort support to illiquid but potentially solvent economies; a sharp depreciation of the euro, which would turn current-account deficits into surpluses; and fiscal stimulus in the core if the periphery is forced into austerity.

Unfortunately, Germany and the ECB oppose this option, owing to the prospect of a temporary dose of modestly higher inflation in the core relative to the periphery.

The bitter medicine that Germany and the ECB want to impose on the periphery – the second option – is recessionary deflation: fiscal austerity, structural reforms to boost productivity growth and reduce unit labor costs, and real depreciation via price adjustment, as opposed to nominal exchange-rate adjustment.

The problems with this option are many. Fiscal austerity, while necessary, means a deeper recession in the short term. Even structural reform reduces output in the short run, because it requires firing workers, shutting down money-losing firms, and gradually reallocating labor and capital to emerging new industries. So, to prevent a spiral of ever-deepening recession, the periphery needs real depreciation to improve its external deficit. But even if prices and wages were to fall by 30% over the next few years (which would most likely be socially and politically unsustainable), the real value of debt would increase sharply, worsening the insolvency of governments and private debtors.

In short, the eurozone's periphery is now subject to the paradox of thrift: increasing savings too much, too fast leads to renewed recession and makes debts even more unsustainable. And that paradox is now affecting even the core.

If the peripheral countries remain mired in a deflationary trap of high debt, falling output, weak competitiveness, and structural external deficits, eventually they will be tempted by a third option: default and exit from the eurozone. This would enable them to revive economic growth and competitiveness through a depreciation of new national currencies.

Of course, such a disorderly eurozone break-up would be as severe a shock as the collapse of Lehman Brothers in 2008, if not worse. Avoiding it would compel the eurozone's core economies to embrace the fourth and final option: bribing the periphery to remain in a low-growth uncompetitive state. This would require accepting massive losses on public and private debt, as well as enormous transfer payments that boost the periphery’s income while its output stagnates.

Italy has done something similar for decades, with its northern regions subsidizing the poorer Mezzogiorno. But such permanent fiscal transfers are politically impossible in the eurozone, where Germans are Germans and Greeks are Greeks.

That also means that Germany and the ECB have less power than they seem to believe. Unless they abandon asymmetric adjustment (recessionary deflation), which concentrates all of the pain in the periphery, in favor of a more symmetrical approach (austerity and structural reforms on the periphery, combined with eurozone-wide reflation), the monetary union's slow-developing train wreck will accelerate as peripheral countries default and exit.

The recent chaos in Greece and Italy may be the first step in this process. Clearly, the eurozone’s muddle-through approach no longer works. Unless the eurozone moves toward greater economic, fiscal, and political integration (on a path consistent with short-term restoration of growth, competitiveness, and debt sustainability, which are needed to resolve unsustainable debt and reduce chronic fiscal and external deficits), recessionary deflation will certainly lead to a disorderly break-up.

With Italy too big to fail, too big to save, and now at the point of no return, the endgame for the eurozone has begun. Sequential, coercive restructurings of debt will come first, and then exits from the monetary union that will eventually lead to the eurozone’s disintegration.

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie