quote:Klik op de link voor het filmpje...A Second Mortgage Disaster On The Horizon?

60 Minutes: New Wave Of Mortgage Rate Adjustments Could Force More Homeowners To Default

Dec. 14, 2008

The Mortgage Meltdown

Scott Pelley reports on the mortgage crisis that's far from over, with a second wave of expected defaults on the way that could deepen the bottom of the U.S. recession. | Share/Embed

(CBS) When it comes to bailouts of American business, Barney Frank and the Congress may be just getting started. Nearly two trillion tax dollars have been shoveled into the hole that Wall Street dug and people wonder where the bottom is.

As correspondent Scott Pelley reports, it turns out the abyss is deeper than most people think because there is a second mortgage shock heading for the economy. In the executive suites of Wall Street and Washington, you're beginning to hear alarm about a new wave of mortgages with strange names that are about to become all too familiar. If you thought sub-primes were insanely reckless wait until you hear what's coming.

One of the best guides to the danger ahead is Whitney Tilson. He's an investment fund manager who has made such a name for himself recently that investors, who manage about $10 billion, gathered to hear him last week. Tilson saw, a year ago, that sub-prime mortgages were just the start.

"We had the greatest asset bubble in history and now that bubble is bursting. The single biggest piece of the bubble is the U.S. mortgage market and we're probably about halfway through the unwinding and bursting of the bubble," Tilson explains. "It may seem like all the carnage out there, we must be almost finished. But there's still a lot of pain to come in terms of write-downs and losses that have yet to be recognized."

In 2007, Tilson teamed up with Amherst Securities, an investment firm that specializes in mortgages. Amherst had done some financial detective work, analyzing the millions of mortgages that were bundled into those mortgage-backed securities that Wall Street was peddling. It found that the sub-primes, loans to the least credit-worthy borrowers, were defaulting. But Amherst also ran the numbers on what were supposed to be higher quality mortgages.

"It was data we'd never seen before and that's what made us realize, 'Holy cow, things are gonna be much worse than anyone anticipates,'" Tilson says.

The trouble now is that the insanity didn't end with sub-primes. There were two other kinds of exotic mortgages that became popular, called "Alt-A" and "option ARM." The option ARMs, in particular, lured borrowers in with low initial interest rates - so-called teaser rates - sometimes as low as one percent. But after two, three or five years those rates "reset." They went up. And so did the monthly payment. A mortgage of $800 dollars a month could easily jump to $1,500.

Now the Alt-A and option ARM loans made back in the heyday are starting to reset, causing the mortgage payments to go up and homeowners to default.

"The defaults right now are incredibly high. At unprecedented levels. And there’s no evidence that the default rate is tapering off. Those defaults almost inevitably are leading to foreclosures, and homes being auctioned, and home prices continuing to fall," Tilson explains.

"What you seem to be saying is that there is a very predictable time bomb effect here?" Pelley asks.

"Exactly. I mean, you can look back at what was written in '05 and '07. You can look at the reset dates. You can look at the current default rates, and it's really very clear and predictable what's gonna happen here," Tilson says.

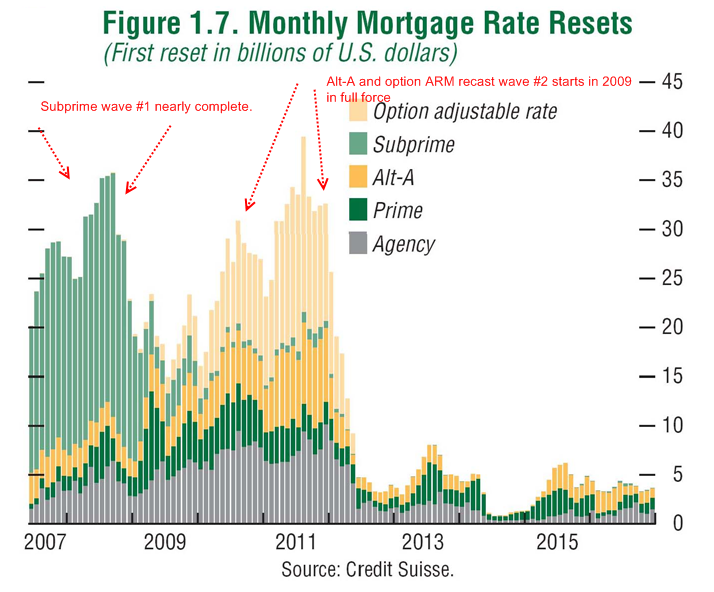

Just look at a projection from the investment bank of Credit Suisse: there are the billions of dollars in sub-prime mortgages that reset last year and this year. But what hasn't hit yet are Alt-A and option ARM resets, when homeowners will pay higher interest rates in the next three years. We're at the beginning of a second wave.

"How big is the potential damage from the Alt As compared to what we just saw in the sub-primes?" Pelley asks.

"Well, the sub-prime is, was approaching $1 trillion, the Alt-A is about $1 trillion. And then you have option ARMs on top of that. That's probably another $500 billion to $600 billion on top of that," Tilson says.

Asked how many of these option ARMs he imagines are going to fail, Tilson says, "Well north of 50 percent. My gut would be 70 percent of these option ARMs will default."

"How do you know that?" Pelley asks.

"Well we know it based on current default rates. And this is before the reset. So people are defaulting even on the little three percent teaser interest-only rates they're being asked to pay today," Tilson says.

50 % is nu verwerkt.... subprime + alt-a

Option arm is now kicking in.

quote:Op woensdag 24 december 2008 02:36 schreef Papierversnipperaar het volgende:

Zijn die ook gebundeld en massaal verkocht aan Europese banken?

quote:Ben je gek joh, tuurlijk nietAEGON

Hypotheek gerelateerde beleggingen

In het derde kwartaal was er ook een sterke daling in de waarde van hypotheek gerelateerde beleggingen, met name van near prime residential (RMBS) en commerical mortgage-backed securities (CMBS).

De risico’s in AEGON’s hypotheek gerelateerde portefeuille zijn duidelijk toegenomen. AEGON heeft regelmatig verwezen naar een deel van de subprime portefeuille waar de meeste afschrijvingen worden verwacht, namelijk van effecten met als onderpand subprime hypotheken met een variabele rente, zogenoemde hybrid ARM’s, beleggingen met een initi�le rating van AA. Op 30 september had AEGON EUR 0,5 miljard van dergelijk beleggingen, minder dan 19% van de totale subprime beleggingsportefeuille van EUR 2,7 miljard.

AEGON heeft ook belegd in andere hypotheek gerelateerde beleggingen, onder meer in effecten met als onderpand near-prime hypotheken, zogenoemde Alt-A en negative amortization/Option ARM floaters. Het grootste deel van deze portefeuille is super senior en zo opgezet dat hoge verliezen op het onderpand kunnen worden weerstaan. Zelfs in het geval van zware verliezen op het onderpand, zullen verliezen op de hoofdsom beperkt blijven.

Meer dan 86% van AEGON’s commercial mortgage-backed beleggingen hebben een senior of super senior AAA rating en kunnen zware verliezen op het onderpand weerstaan zonder verlies op de hoofdsom. Obligaties zonder AAA rating zijn conservatief afgesloten.

quote:Fail....Op woensdag 24 december 2008 08:48 schreef Basp1 het volgende:

Wanneer de rente zo laag blijft staan als deze nu al staat en de banken in de VS zouden dit ook naar de klant door rekenen zou er niet al te veel met die ARM hypotheken aan de hand moeten zijn. Dan moet wel de rente de gehele looptijd van die hypotheken zo laag blijven staan wat toch nooit zal gebeuren.

Zie rekenvoorbeeldjes met 1 % en 6,25 %

quote:Smells like ponzi to me.I hope this helps to clear up some of the confusion surrounding option ARMs. I felt it was necessary to clear up some of the details of these mortgages to put an end to any notion that lower rates are somehow going to buffer $500 billion in option ARM recasts over the next few years. It won’t. It is all about the price.

quote:en fortisOp woensdag 24 december 2008 10:47 schreef Emu het volgende:

Deels eens maar ook deels niet. Over de ARM's spreek ik mij niet uit, maar Alt-A loans vertegenwoordigen toch een ander type ontlener. Maar daar zal de default rate inderdaad ook wel stijging. Pittig detail, ING zit diep in de ALT-A :p Ik heb om die reden mijn ING aandelen nog verkocht aan 24 euro (gelukkig).

De FED is nu buyer and lender of last resort nu de rest van de wereld geen trek meer heeft in VS hypotheken.

De FED balance sheet zal nog verder exploderen.

In feite worden die hypotheken Monetized, er worden gewoon vers geperste dollars voor betaald.

Omdat de huizenprijzen dat niet deden, en in de VS de bank het risico draagt!! is het fout gegaan. Wanneer je in de VS een (top)-hypotheek hebt van $300,000,= en de marktwaarde van je huis is onder de $200K gezakt, mag je gewoon de bank inlopen en je sleutel inleveren.

Je huis ben je dan kwijt, maar je schuld ook. En daar ' verdien" je op zo'n moment dus $100K mee! Het allerergste is dat bovenstaande een zichzelf versterkend effect is. Want het doet de prijs weer meer zakken, waardoor het voor meer mensen aantrekkelijker word de sleutel in te leveren, et cetera. Er stelt zich dus geen evenwicht in maar juist een kettingreactie!!

Gelukkig kunnen in Nederland huizenprijzen alleen stijgen. Dat heeft Bos vorig jaar zelf gezegd.

Huizenprijzen in de staat CA.

Do the math

quote:Holy fuck...Op woensdag 31 december 2008 13:55 schreef Drugshond het volgende:

[ afbeelding ]

Huizenprijzen in de staat CA.

Do the math

quote:Dit scenario is in NL niet ondenkbaar. Er is hier meer overwaardering dan ooit in Californie is geweest.Op woensdag 31 december 2008 13:55 schreef Drugshond het volgende:

[ afbeelding ]

Huizenprijzen in de staat CA.

Do the math

quote:Nee ook dan niet, want banken zijn heel creatief in het vinden van mogelijkheden om geld uit te lenen, dan had men starters een lening gegeven op basis van de Balkenende norm en het toekomstige inkomen van de labrador was volledig meegeteld geworden.Op woensdag 24 december 2008 14:36 schreef LXIV het volgende:

De kern van het probleem is dat men er vanuit is gegaan dat de huizenprijzen in Amerika altijd zouden blijven stijgen. In dat scenario was alles goed gegaan.

En in de US hadden ze een president die goed meewerkte met de banken in cre�ren van virtuele rijkdom door de payability op te jagen met leningen aan ontslagen luiwammessen en mensen met veel schulden.

Die hypotheken werden toch doorverkocht naar Europa dus wat maakt het uit

quote:Net als ieder pyramidesysteem blijft het systeem intact zolang de massa er nog in geloofd en bereid is om in te stappen.Op woensdag 31 december 2008 15:18 schreef henkway het volgende:

[..]

Nee ook dan niet, want banken zijn heel creatief in het vinden van mogelijkheden om geld uit te lenen, dan had men starters een lening gegeven op basis van de Balkenende norm en het toekomstige inkomen van de labrador was volledig meegeteld geworden.

En in de US hadden ze een president die goed meewerkte met de banken in cre�ren van virtuele rijkdom door de payability op te jagen met leningen aan ontslagen luiwammessen en mensen met veel schulden.

Die hypotheken werden toch doorverkocht naar Europa dus wat maakt het uit

OVerigens wordt het grootste deel van de schuld betaald door het bijdrukken van dollars, dus denk ik door de Chinezen. Want bijdrukken van dollars als jij zelf een triljardenschuld in dollars hebt hoeft helemaal niet ongunstig te zijn!!

Wat dat betreft heeft Amerika echt onevenredig geprofiteerd de afgelopen 60 jaar van de positie van de dollar als wereldvaluta. Logisch dat veel landen ze niet meer hebben willen.

quote:Maar die chinezen zijn knettergek als ze hiermee doorgaan en de japanners ook, ik zou zeggen wissel maar om en afrekenen in renminbiOp woensdag 31 december 2008 15:22 schreef LXIV het volgende:

[..]

OVerigens wordt het grootste deel van de schuld betaald door het bijdrukken van dollars, dus denk ik door de Chinezen. Want bijdrukken van dollars als jij zelf een triljardenschuld in dollars hebt hoeft helemaal niet ongunstig te zijn!!

ze hebben trouwens de WTC torens verplaatst naar china

quote:Dat kan niet, want als ze maar 25% van hun voorraad dumpen is de rest niks meer waardOp woensdag 31 december 2008 15:27 schreef henkway het volgende:

[..]

Maar die chinezen zijn knettergek als ze hiermee doorgaan en de japanners ook, ik zou zeggen wissel maar om en afrekenen in renminbi

quote:It's just beginning..... let wel de ALT-A assets van ING (AAA) zijn op dit moment bezit van de Nederlandse belastingbetaler.S&P Warns — Again — on Alt-A First Liens

Standard & Poor’s Ratings Services said earlier this week that its ratings on 9,430 classes from 1,077 U.S. first-lien Alt-A RMBS transactions issued in 2005, 2006, and 2007 had been placed on CreditWatch with negative implications — otherwise translated as “downgrade imminent.” The affected classes had an original par amount of approximately $552.83 billion, and have a current principal balance of $445.43 billion, the rating agency said.

It’s almost becoming a yawner to see more RMBS downgrades, but what they mean should not be lost on any market participant, even if they’re increasingly common and the hundreds of billions of dollars involved now seem a numbing figure to most of us covering this mess.

A review of the thousands upon thousands of classes by HousingWire shows that roughly half of the at-risk bonds are currently rated AAA by the rating agency; downgrades to securities rated AAA are likely to lead to further write-down pressure for banks and insurers already hard-hit by ratings downgrades.

S&P said the ratings warning came on the heels of a Feb. 24 update to the agency’s loss severity assumptions for most Alt-A transactions. S&P cited a “belief that the influence of continued foreclosures, distressed sales, an increase in carrying costs for properties in inventory, costs associated with foreclosures, and more declines in home sales may depress prices further and lead loss severities higher than we had previously assumed” on recent Alt-A deals.

As of the February 2009 distribution date, severe delinquencies — 90+ days, foreclosures and REOs — have accounted for an average of 22.92 percent of current aggregate pool balance for affected transactions, S&P said. And, over the past three months, severe delinquencies in affected deals have risen by a sharp 24.5 percent, illustrating the pressure much of the Alt-A space is now facing.

S&P last made major cuts to private-party RMBS deals in early February. Read previous coverage.

The bottom line here is this: for all of the pain felt in this area already, plenty of banks large and small are still generally carrying securities on their books at a level justifiable against current ratings levels (how many investor presentations have we seen in recent months touting the percentage of securities held rated AAA?). Would-be buyers know the securities aren’t worth the AAA rating they’ve got, and frankly so too do any would-be sellers, but nobody can sell a security still at AAA at C-level prices, and then justify the hit that so doing would have on the rest of their books.

With many of these AAA high-fliers falling officially off their perch, that dynamic appears set to change further.

70-30 % kans dat we hier een goede deal hebben gemaakt (volgens Bos).

We will see.

quote:ach het is een win-win situatie. of het is het eind van de kankermaatschappij as we know it, of het is het eind van de altijd grif burgergeld uitgevende pvda.Op woensdag 11 maart 2009 19:48 schreef Drugshond het volgende:

[..]

It's just beginning..... let wel de ALT-A assets van ING (AAA) zijn op dit moment bezit van de Nederlandse belastingbetaler.

70-30 % kans dat we hier een goede deal hebben gemaakt (volgens Bos).

We will see.

quote:zit de pvda ook in de US ??Op woensdag 11 maart 2009 19:55 schreef zoalshetis het volgende:

[..]

ach het is een win-win situatie. of het is het eind van de kankermaatschappij as we know it, of het is het eind van de altijd grif burgergeld uitgevende pvda.

quote:Indirect met ING wel

quote:wat een domme vraag.

quote:Yup, we subsidieren arme amerikanen. Ik heb al medelijden

quote:Op woensdag 11 maart 2009 20:45 schreef zoalshetis het volgende:

pvda. niet allen voor allochtonen, maar ook om ons geld zo snel mogelijk weg te krijgen. partij van de allochtoon is nu ook nog eens partij van de amerikanen.

Doet het goed bij de achterban denk ik

Banks: Here Come The OptionARM Blowups!

Well well well.

From my 2009 Prediction Ticker:

Mortgages are not done. The story last year was "Subprime." This year's will be "ALT-A", "Option ARMs" and so-called "Prime". The Fed and Treasury know this, which is why they are playing games with "agency" debt in a desperate attempt to clear this market before the ticking nuclear devices go off. The amount of debt involved in these "bad deals" is vastly higher than that in the "subprime" space and if they fail to contain it (a near certainty) Round #2 of severe bank instability gets served up on us in the second half of 2009.

No really?

Guess what the WSJ said this weekend?

NEW YORK (Dow Jones)--For the third straight month, option adjustable-rate mortgages are generating proportionally more delinquencies and foreclosures than subprime mortgages, the scourge of the housing crisis.

A further acceleration of troubles among the loans could mean higher-than-expected losses for Wells Fargo & Co. (WFC) and JPMorgan Chase & Co. (JPM), as well as the Federal Deposit Insurance Corp.'s own insurance fund.

Yep. Bank-o-rama is not over. And by the way, this is what I said to Dick Bove on this subject well over a year ago:

Also note that we STILL haven't gotten entirely back to sound lending principles, which are 20% down payments, 36% DTI and a 30 year fixed mortgage. Until we do and prices adjust at that level we are not at a housing bottom.

There is much more, of course, if you care to review that article. Its actually pretty good.

Then there's this ditty that I wrote before (shortly before) WaMu blew up:

The Truth is that OTS should have demanded that these clowns eliminate the dividend back in April of 2007 and disgorge this paper, no matter the mark. I wrote about it back then and said they were toast, and now, with the stock trading at just over $2, it looks like their day is coming.

.....

Anyone who didn't recognize in April of 2007 that these OptionARM loans in California were underwater then and would only go FURTHER underwater, and as such this "capitalized interest" would never be paid, is absolutely unqualified to run a frapping lemonade stand, say much less a Federal Regulatory Agency.

Of course our fine government apparatus, instead of shutting these clowns down, played "shotgun marriage" with both them and Wachovia - exactly what it did with Fannie, Freddie and AIG. As such all that happened is that the ticking bomb got moved somewhere else instead of being put out in the desert where it wouldn't hurt "innocent bystanders" - oh no, instead, let's put it in the middle of a big city so that we can then shower taxpayer money on it in an attempt to keep it from blowing sky high!

That obviously didn't work as you can now see, and we're not talking small potatoes either.

Wells "acquired" $115 billion of these things when they "bought" Wachovia. They claim they're worth $93 billion. Oh really? A bunch of loans that were mostly at or near 100% Loan-to-value (that is, near zero equity) when originally written, in markets where prices have declined by half? Oh, and in May, the firm said that 51% of the balances out were being paid only on the minimum - that is, they are still negatively-amortizing even as house prices fall! Talk about double-screwed!

JP Morgan, for its part, has nearly $90 billion in exposure through both its "acquisition" of WaMu and a pretty set of off-balance sheet "vehicles" (which of course are being shielded from having to be accounted for, and who knows how well those are performing!)

Oh, and as I and others have noted, we're just starting to see "recasts" on these mortgages, which will continue for the next couple of years, and these "recasts", which cannot be avoided as the properties are deeply underwater and thus cannot be refinanced, often cause payments to double or even triple.

I've been warning people about this now for a long time; finally, the "mainstream media" is picking up on it. Indeed, if you go back to the origin of The Market Ticker you will find that I started writing this blog precisely because Washington Mutual (WaMu) reported "earnings" that were insufficient to pay their dividend, "paying" the rest with capitalized interest (that, is negative amortization amounts that were getting added to principal!) Of course that only works if the principal ever gets paid!

Indeed, go back to the very first articles on The Market Ticker and what do you find? They're all about Option ARMs! Examples?

How about right here, from April 18th 2007:

Let's use WaMu as an example, because they make a particularly good - or ugly, depending on your perspective - example of this.

In March of 2006, Washington Mutual recorded net income of $985 million dollars. 4Q06 they booked $1,058 mln. This last quarter, they booked $784mln.

But in those three quarters they booked $194mln, $333mln and $361 million, respectively, in PayOption ARM "Capitalized Interest." This was booked and recognized as EARNINGS.

Now here's the problem: In 1Q 06, 194 million out of $985 is 19.7%. In December, it was 31%. But this last quarter, it was FORTY SIX PERCENT, more than a DOUBLE over the year ago levels.

And what's worse, not one dime of that "income" can be spent! It is entirely phantom.

This is the same sort of crap that sunk Lucent and Enron - booking "income" that is not in fact spendable, as it has an impairment associated with it (the LTV is INCREASED by this negative amortization) AND it is not CASH!

And from the very first article in The Market Ticker archives....

1. Combined "loan to value" on ALT-A purchases in 2006 was 88% on average, with 55% of buyers taking out a second at the same time as the purchase.

2. Low or no-documentation (stated income) loans were 81% of total originations.

3. Interest only and option ARMs were 62% of purchase originations in 2006.

4. 1-year hybrid ARMs were 28% of ALT-A originations in 2006 (these loans reset in just one year!)

5. Investors and second home buyers were 22% of ALT-A purchase originations in the last year.

6. Approximately 40% of purchases in 2006 involved second mortgages taken at the same time as the purchase. This is important because these "piggybacks" are how you get around loan-to-value restrictions! While the industry has tried to say that this is primarily a subprime thing, THAT IS A LIE - 55% of ALT-As had piggypacks in 2006!

7 TWENTY FOUR PERCENT OF ALL NEW ALT-A ORIGINATIONS WERE INTEREST ONLY OR NEGATIVE AMORTIZATION IN 2006!

Generational buy on banks eh, when their entire "valuation" is predicated on balance sheets where one can't possibly assign an honest value to huge parts of their loan portfolio?

I think not, and I've been pounding the table on this since The Market Ticker began - literally, from the first posting.

SHUT THEM ALL DOWN.

================================================================

Showtime....and this time it will be ugly

Monday, July 13, 2009

The chart below was promptly whipped up after reading this report($) in today's Wall Street Journal about just how fast Option-ARMs are souring as compared to subprime loans.

IMAGE It's not so much that the default rates for Option-ARMs have exceeded that of subprimes loans for three months running, but that the absolute numbers are so high.

More than one-third of all Option-ARMs (called Pick-A-Pay loans below) are in default and most of these are likely to make it to the foreclosure stage eventually.

Option ARMs were typically issued to creditworthy homeowners and allow borrowers to make a range of monthly payments. The payment options include a partial-interest payment that adds the unpaid interest to the loan's balance. On many such loans, balances have risen while values of the underlying properties have plummeted amid the housing crisis.

As of April, 36.9% of Pick-A-Pay loans were at least 60 days past due, while 19% were in foreclosure, according to data from First American CoreLogic, a unit of Santa Ana, Calif.-based First American Corp. In contrast, 33.9% of subprime loans were delinquent, with 14.5% of those loans in foreclosure, the figures show.

Payment-option mortgages are heavily concentrated in the worst-hit regions in the housing market, including California and Florida, making borrowers inordinately vulnerable to declining property values. The deepening loan turmoil could mean higher-than-expected losses for Wells Fargo & Co., J.P. Morgan Chase & Co. and the Federal Deposit Insurance Corp.'s own insurance fund.

"The realization of the issues related to option ARMs is just beginning," said Chris Marinac, director of research at Atlanta-based FIG Partners.

If memory serves, the wackiest thing about Option-ARMs a few years ago was that banks could book the interest and principal payments as income even though they weren't actually receiving the money - the vast majority of borrowers were only making the lowest payment that didn't even cover the full amount of the interest due that month.

quote:Ieder rationeel denkend mens zou dit concept per definitie al hebben afgeschoten. Waarom konden de Amerikaanse banken dat ook niet bedenken?? Ik kan de mensen die zo'n hypotheek hebben niet kwalijk nemen dat ze niet betalen trouwens. Financieel gezien zou dat stom zijn. Laat de banken die zich hiermee hebben ingelaten maar failliet gaan, anders komen we nooit van deze rotzooi af.Op dinsdag 14 juli 2009 21:19 schreef zoalshetis het volgende:

IK HEB NATUURLIJK WEER GELIJK GEKREGEN.

quote:banken moeten gaan beseffen dat ze met het geld van burgers geen burgers moeten gaan uitzuigen. we hebben het wel eens over te grote, uitzuigende ambtenarenapparaten, maar de banken kunnen er ook wat van.Op woensdag 15 juli 2009 22:05 schreef drexciya het volgende:

[..]

Ieder rationeel denkend mens zou dit concept per definitie al hebben afgeschoten. Waarom konden de Amerikaanse banken dat ook niet bedenken?? Ik kan de mensen die zo'n hypotheek hebben niet kwalijk nemen dat ze niet betalen trouwens. Financieel gezien zou dat stom zijn. Laat de banken die zich hiermee hebben ingelaten maar failliet gaan, anders komen we nooit van deze rotzooi af.

vies spelletje met ons geld. hypotheekrente op 2 % of inflatiegerelateerd.

quote:Natuurlijk. Gingen als warme broodjes over de toonbank. 8% op een triple A-pakketje. Je bent gek als je dat niet doet.Op woensdag 24 december 2008 02:36 schreef Papierversnipperaar het volgende:

Zijn die ook gebundeld en massaal verkocht aan Europese banken?

quote:70% default haalt volgens mij ELQ niet eens.

By Lisa Lambert

WASHINGTON (Reuters) - The federal government and states are girding themselves for the next foreclosure crisis in the country's housing downturn: payment option adjustable rate mortgages that are beginning to reset.

"Payment option ARMs are about to explode," Iowa Attorney General Tom Miller said after a Thursday meeting with members of President Barack Obama's administration to discuss ways to combat mortgage scams.

"That's the next round of potential foreclosures in our country," he said.

Option-ARMs are now considered among the riskiest offered during the recent housing boom and have left many borrowers owing more than their homes are worth. These "underwater" mortgages have been a driving force behind rising defaults and mounting foreclosures.

In Arizona, 128,000 of those mortgages will reset over the the next year and many have started to adjust this month, the state's attorney general, Terry Goddard, told Reuters after the meeting.

"It's the other shoe," he said. "I can't say it's waiting to drop. It's dropping now."

The mortgages differ from other ARMs by offering an option to pay only the interest each month or a low minimum payment that leads to a rising balance in the loan's principal.

When the balance of the loan reaches a certain level or the mortgage hits a specific date, the borrower must begin making full payments to cover the new amount. The loan's interest rate also may have been fixed at a low level for the first few years with a so-called teaser rate, but then reset to a higher level.

Because the new monthly payments can be five or 10 times what borrowers are accustomed to paying, they "threaten a much greater hit to the consumer than the subprimes," Goddard said, referring to the mortgages often extended to less credit-worthy

borrowers that fed the first wave of the financial crisis.

Miller said option-ARMs were discussed at Tuesday's meeting on mortgage scams, which brought state attorneys general from across the country together with U.S. Treasury Secretary Timothy Geithner, Attorney General Eric Holder, Housing and Urban Development Secretary Shaun Donovan, and Federal Trade Commission Chairman Jon Leibowitz.

The mortgages tend to be "jumbo," or for significantly large amounts, Goddard said, making it even harder for borrowers to sidestep foreclosure. He said he expected to see an increase in scams as distressed homeowners become more desperate to refinance big debts.

Goddard said his office is investigating hundreds of cases where companies have made fraudulent promises, and charged large fees, to mortgage defaulters.

The U.S. housing market has suffered the worst downturn since the Great Depression, and its impact has rippled through the recession-hit economy.

Some signs of stabilization emerged recently, with sales rising and home price declines moderating in many regions of the country. Home prices in some regions have risen.

However, many economists say there is still a huge supply of unsold homes lingering on the market and that, coupled with a frenzy of more foreclosures ahead, should depress home prices for the rest of 2009.

Real estate data firm RealtyTrac, in its August 2009 U.S. Foreclosure Market Report, said foreclosure filings -- default notices, scheduled auctions and bank repossessions -- were reported on 358,471 U.S. properties during the month, a decrease of less than 1 percent from the previous month, but an increase of nearly 18 percent from the same month a year ago.

The report said one in every 357 U.S. housing units received a foreclosure filing last month.

...........................................................

Ben benieuwd heel benieuwd.... zeker voor de toekomstige positie van Wells Fargo

zat er aan te komen, heeft iemand nog dat grafiekje wanneer alt a piekt?

quote:Ga 1 pagina terug in dit topic.Op zondag 20 september 2009 10:14 schreef edwinh het volgende:

zat er aan te komen, heeft iemand nog dat grafiekje wanneer alt a piekt?