NWS Nieuws & Achtergronden

Discussieer hier diepgaander over de actualiteiten.

Achtergronden.... : De Amerikaanse huizencrisis in de praktijk.

cbsnews - House of Cards A must see docu

Wat er te koop staat (executieverkoop) in Stockton.

cbsnews - House of Cards A must see docu

Wat er te koop staat (executieverkoop) in Stockton.

Lijkt een beetje op proletarisch wonen. Ontnuchterende docu die een tipje van de sluier oplicht van wat er in Amerika aan de hand is. En de banken staan hier machteloos.quote:A tipping point? "Foreclose me ... I'll save money"

LATimes

A homeowner who can't sell his house tells the L.A.Times, "Foreclose me. ... I'll live in the house for free for 12 months, and I'll save my money and I'll move on."

Banks and lenders fear this kind of thinking -- that walking away from a house could be the smart economic move -- appears to be on the rise. Wachovia, in a conference call yesterday, warned investors that increasing numbers of homeowners are walking away from their homes by choice: "... people that have otherwise had the capacity to pay, but have basically just decided not to because they feel like they've lost equity, value in their properties..."

Calculated Risk notes this is "one of the greatest fears for lenders ... that it will become socially acceptable for upside down middle class Americans to walk away from their homes."

A commenter on L.A. Land this morning writes, "I am one of these people. My condo has dropped in value from $520K in 5/06 when I bought it to $350K now. My ARM payment will probably go up $900 per month in June.

"Despite all this, I would be willing to stay if the bank would refi the loans to a 30 year fixed, but since I'm not a 'hardship' case they'd apparently rather foreclose. I guess the only way I could qualify for loan mitigation is to get my boss to fire me, stop making payments, and wreck my credit. In fact, my bank won't even talk to me until I miss a couple of payments.

"I have purchased a cheaper place in a nearby area now, while my credit is good, and will stop making payments on house #1 after house #2 closes. I know the foreclosure will be on my credit for 7 years, but I will have saved a lot of money.

"I realize I agreed to the deal when I signed the mortgage papers, but I am within my rights to walk away from a bad deal and suffer the consequences, just as many corporations write down billions of dollars of debt, lose money for their shareholders, and lay off people as a result of their bad decisions.

"I don't really understand why people view a business decision by a homeowner as a terrible moral lapse. However, when large lending institutions, with access to more sophisticated information than any consumer could imagine, make mistakes affecting thousands of people worldwide, they are not excoriated and vilified with the same righteous zeal."

quote:globaleconomicanalysis.blogspot

Changing Social Attitudes At Forefront Of Crisis

Changing Social Attitudes About Debt have clearly moved to the forefront of the housing crisis. Even those who can afford to pay are walking away with no regrets. And with people walking away in mass, Banks Attempt To Freeze Balance Sheets is destined to fail.

This is what happens when you give people free money. Unfortunately, Bernanke, Congress, and Paulson are intent on giving away more free money to fix the problem. On the surface this might appear inflationary. However, credit destruction and bank impairments are happening far faster than Bernanke and Congress are acting.

Welcome to Deflation American Style. At the current rate of progression, Deflation American Style figures to be far worse than anything Japan ever saw.

Proletarisch? Ja, misschien, maar zoals het artikel al zegt; er wordt totaal geen energie gestoken in mensen die altijd betalen en iets willen. Je moet ergens buiten vallen voordat je aandacht krijgt. Dit is wat drastisch, maar de aandacht heb je, en als je nog eens in je recht staat is het misschien 'sociaal minder aanvaartbaar' in de ogen van banken, maar dit zal natuurlijk een rage gaan worden.

Het probleem van de banken wordt door de banken netjes teruggelegd bij de consument die nu eindelijk iets heeft gevonden om terug te slaan. En dat doen ze ook. Mensen zeggen altijd dat banken nooit geven, maar dat je wel altid moet betalen. Dat zal toch zeker meeleven in een dergelijke overweging: 'eindelijk kan ik wat geld verdienen aan mijn bank'...

Het probleem van de banken wordt door de banken netjes teruggelegd bij de consument die nu eindelijk iets heeft gevonden om terug te slaan. En dat doen ze ook. Mensen zeggen altijd dat banken nooit geven, maar dat je wel altid moet betalen. Dat zal toch zeker meeleven in een dergelijke overweging: 'eindelijk kan ik wat geld verdienen aan mijn bank'...

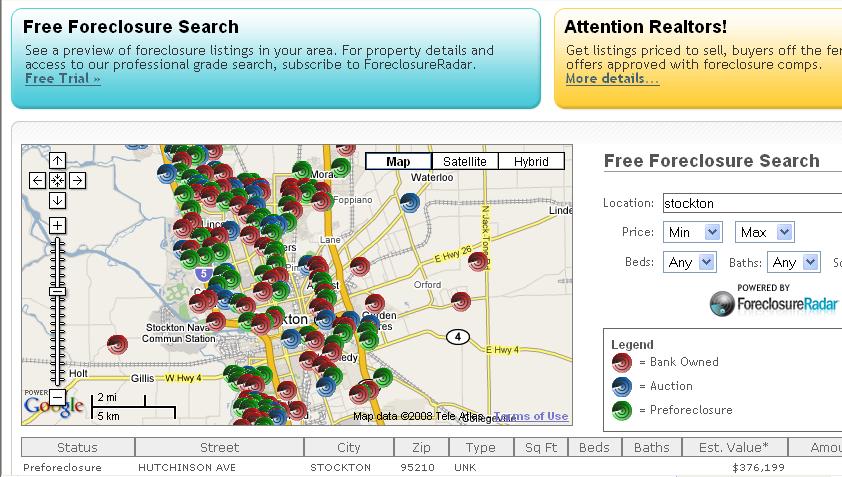

Die site http://www.foreclosureradar.com is echt "shock and awe", als je wat locaties gaat opzoeken.

San Francisco

Oakland

Het is een best wel flink probleem. Me dunkt.

[ Bericht 1% gewijzigd door Drugshond op 31-01-2008 08:11:09 ]

Het is een best wel flink probleem. Me dunkt.

[ Bericht 1% gewijzigd door Drugshond op 31-01-2008 08:11:09 ]

Gewoon verstandig zakendoen. Het is toch niet illegaal? Dan pak je de mogelijkheid met het minste verlies.quote:Op donderdag 31 januari 2008 06:45 schreef Drugshond het volgende:

Lijkt een beetje op proletarisch wonen. Ontnuchterende docu die een tipje van de sluier oplicht van wat er in Amerika aan de hand is. En de banken staan hier machteloos.

Free Assange! Hack the Planet

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

Het is wel illegaal in de zin dat je een koopcontract hebt afgesloten met verplichtingen die je niet nakomt. Maar deze handelswijze levert wellicht wel wat voordelen op.quote:Op donderdag 31 januari 2008 07:45 schreef Papierversnipperaar het volgende:

[..]

Gewoon verstandig zakendoen. Het is toch niet illegaal? Dan pak je de mogelijkheid met het minste verlies.

Het is verboden om er achter te komen dat je te weinig geld hebt om je verplichtingen na te kunnen komen? Dus al die mensen die in Nederland in de schuldhulpverlening zitten moeten naar de gevangenis?quote:Op donderdag 31 januari 2008 07:52 schreef Drugshond het volgende:

[..]

Het is wel illegaal in de zin dat je een koopcontract hebt afgesloten met verplichtingen die je niet nakomt. Maar deze handelswijze levert wellicht wel wat voordelen op.

Free Assange! Hack the Planet

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

Hmmmzz.... heropvoedingskamp wellicht.quote:Op donderdag 31 januari 2008 08:01 schreef Papierversnipperaar het volgende:

[..]

Het is verboden om er achter te komen dat je te weinig geld hebt om je verplichtingen na te kunnen komen? Dus al die mensen die in Nederland in de schuldhulpverlening zitten moeten naar de gevangenis?

Goeie vergelijking overigens... als straf een financiële sanctie zal ook niet veel helpen. Want een kale kip kun je niet plukken.

Nou zullen niet alle huiseigenaren echt te arm zijn, maar tot hoeverre kan je iemand dwingen om te duur te wonen?quote:Op donderdag 31 januari 2008 08:10 schreef Drugshond het volgende:

[..]

Hmmmzz.... heropvoedingskamp wellicht.

Goeie vergelijking overigens... als straf een financiële sanctie zal ook niet veel helpen. Want een kale kip kun je niet plukken.

Free Assange! Hack the Planet

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

[b]Op dinsdag 6 januari 2009 19:59 schreef Papierversnipperaar het volgende:[/b]

De gevolgen van de argumenten van de anti-rook maffia

Hoe erg valt hier nou een slag uit te slaan? Ik bedoel ik zie hier een huise met een 'estimated value' van 225.000 USD voor 9.422 USD verkocht worden en dat zou dan in zo'n huisje moeten zijn... Al zullen er natuurlijk wel een hele hoop haken aan zitten..

Ik heb nog wel 9k liggen hoor

Ik heb nog wel 9k liggen hoor

jij bent druk bezig

maar doe es humor, en tiep in: "living from your car" in google

maar doe es humor, en tiep in: "living from your car" in google

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

ik zou iig nog ff wachten hoor. we zitten nog niet op het hoogte dieptepuntquote:Op donderdag 31 januari 2008 08:20 schreef Xith het volgende:

Hoe erg valt hier nou een slag uit te slaan? Ik bedoel ik zie hier een huise met een 'estimated value' van 225.000 USD voor 9.422 USD verkocht worden en dat zou dan in zo'n huisje moeten zijn... Al zullen er natuurlijk wel een hele hoop haken aan zitten..

Ik heb nog wel 9k liggen hoor

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Om even een vergelijking te maken, dit is polonium-sushi serveren aan de wereldeconomie.quote:"They were getting loans in excess of 100 percent of the value of the property," Abbott says. "That type of thing. So, most of 'em were actually putting a little bit of money in their pocket at close of escrow."

"So, they were getting paid to buy a house?" Kroft asks.

"They were getting paid to buy a house. Yes. Yeah," Abbott says.

And strangely enough, it didn't seem to bother the lenders either, who were collecting huge fees just for landing the loans.

"Whatever they wanted to state for their income. The bank accepted that at face value and made the loan based on that income," Abbott says.

Abbott says borrowers got the money, without a down payment.

Jim Grant calls it an invitation to fraud. "You apply to a bank, or a mortgage broker for a loan. And you would fill out a form. And you would say, 'I have an income of, oh, $400,000 a year.' They say, 'You do? Fine. Just sign right there.' And they would nod, and because they were being paid, not by the veracity of the information, but by the consummation of the deal. The lending office would say, 'Ah. You have verified this?' 'Why, yes, we have.' And the lending officer would say, 'Great. So do I,'" Grant says.

"And he got a cut, too?" Kroft asks.

"Yes, oh, yes. Everyone gets a cut," Grant says.

Almost all of the people involved in the transactions made huge amounts of money, then passed the risk onto someone else. Instead of keeping the dicey loans in their own portfolios, the big banks and giant mortgage companies that originally underwrote them, resold the mortgages to big New York investment houses.

Firms like Bear Stearns and Merrill Lynch sliced the loans into little pieces and packaged them up with other investments, then sold them to their best customers around the world as high-yield mortgage-backed securities, turning sows' ears into silk purses, all with the blessing of rating agencies like Standard & Poor’s.

And what rough beast, its hour come round at last,

Slouches towards Bethlehem to be born?

Slouches towards Bethlehem to be born?

dat is wat er gebeurt als je je hypotheek niet meer kan betalen. de bank legt dan beslag op je huis (wat immers onderpand was voor je hypotheek) en jij moet eruit.quote:Op donderdag 31 januari 2008 09:12 schreef NT-T.BartMan het volgende:

Kan iemand met relevante kennis even kort toelichten wat 'foreclosure' is??

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Aha. En de grap is in deze dan dat de bank het huis óók niet verkocht krijgt? Of begrijp ik de tekst niet goed?quote:Op donderdag 31 januari 2008 09:14 schreef simmu het volgende:

[..]

dat is wat er gebeurt als je je hypotheek niet meer kan betalen. de bank legt dan beslag op je huis (wat immers onderpand was voor je hypotheek) en jij moet eruit.

ze krijgen het in ieder geval niet verkocht voor de prijs ter hoogte van de hypotheek, da's de grap.quote:Op donderdag 31 januari 2008 09:19 schreef NT-T.BartMan het volgende:

[..]

Aha. En de grap is in deze dan dat de bank het huis óók niet verkocht krijgt? Of begrijp ik de tekst niet goed?

stel: iemand koopt een huis van 300.000 in september 2005 met een ARM (adjustable rates mortgage) hypotheek, waarvan de eerste 2 jaar de rente (uit de lucht gegrepen getallen, die wel het idee weergeven) 4 % bedraagt, na die 2 jaar (dus vanaf oktober 2007) reset naar het marktpercentage (dat zal dan zo'n 8 a 9 % zijn). nu is het oktober 2007, de rent resets, de maandlasten voor de woning worden flink hoger, en helaas: dan blijkt de persoon die niet meer te kunnen betalen, want hij kon om te beginnen alleen die lage rente betalen. dus hij moet verkopen.

da's de situatie van de persoon. nu de economische situatie:

jarenlang stegen de huizenprijzen. makelaars, banken, alles en iedereen die bij "huizen kopen en verkopen" betrokken was profiteerden. uiteraard was het in hun belang om huizenprijzen hoog in te schatten. hoger en hoger en hoger dus. The sky is the limit! er werden boeken over geschreven: "how to profit from the housing boom" en 'flippers' (mensen die een huis kopen, en na een half jaartje ofzo weer verkopen en de dan gekweekte overwaarde als winst pakken) maakten flinke winst. banken vonden het niet langer nopdig om kredietaanvragen goed te controleren, aangezien een paar missers ruim goedgemaakt werden door de algeheel hoge prijzen. dit noemt men de 'liarloans'. mensen die eigenlijk geen hypotheek konden betalen konden dat opeens wel, door liarloans en arm hypotheken zonder aanbetaling. maar: arms resetten, en als mensen veel minder inkomen hebben dan ze aangaven, kunnen ze de hypotheek niet meer betalen. heel veel mensen. dus de vraag naar nieuwe huizen daalt, dus de prijzen dalen!

terug naar die persoon: die heeft nu een hypotheek van 300.000 (een lening die hij moet betalen) waarvan niets is afgelost, een veel te hoge rente die hij niet kan betalen en een huis wat nog maar 250.000 waard is (en nu ben ik heel genereus). dat betekent dus een faillisement of een restschuld.

ok, da's allemaal diep triest en naar. maar vanwaar dan nu deze crisis? nou: die banken he: die hebben dergelijke leningen heel veel afgesloten, en zitten nu met huizen die niet veel meer waard zijn, en die ze nog niet aan de straatstenen verkocht krijgen. consumenten hebben geen cent te makken dus kopen niks, dus producenten kunnen niets verkopen, maken verlies, etc etc etc...

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Met andere woorden: de banken moeten niet janken wegens ernstig boter op hun hoofd? Op meerdere nivo's ontvengen mensen provisie op de leningen en kijken daarom niet zo precies naar de inhoud?

Jammer dat dat dan weer invloed moet hebben op de wereldeconomie...

Jammer dat dat dan weer invloed moet hebben op de wereldeconomie...

daarmee heb je het correct samengevatquote:Op donderdag 31 januari 2008 10:36 schreef NT-T.BartMan het volgende:

Met andere woorden: de banken moeten niet janken wegens ernstig boter op hun hoofd? Op meerdere nivo's ontvengen mensen provisie op de leningen en kijken daarom niet zo precies naar de inhoud?

Jammer dat dat dan weer invloed moet hebben op de wereldeconomie...

maar het wordt nog erger. die hypotheken werden in pakketjes bij elkaar gestopt en doorverkocht als investeringen (creditvard schulden e.d. trouwens ook). er werden (veel te gunstige!) beoordelingen gegeven voor het risico (a.d.h.v. de inhoud van zo'n pakketje, zonder kennis van de individuele hypotheken!).

en nu blijkt dus dat veel van die leningen, dus ook die pakketjes oninbaar zijn/worden, terwijl niemand precies weet welk huis waar zit, en inmiddels de hele wereld over verhandeld is.

uiteraard: om zaken dan nog wat door te drijven, veel van die pakketjes waren uiteraard ook verzekerd. a.d.h.v. diezelfde (veel te gunstige!) beoordelingen.

zoek het maar eens op op wikipedia: het is het ultieme spel "the greatest fool"

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dikke crosspost.Om ff aan te geven dat we het hier hebben over flinke bedragen.

quote:S&P voorziet subprime-verliezen tot boven USD 265 mrd

Beurs

(tbm) - Amsterdam (BETTEN FINANCIAL NEWS) - Kredietbeoordeelaar Standard & Poor's verwacht dat de verliezen van financiele instellingen op investeringen gerelateerd aan de Amerikaanse markt voor risicovolle hypotheken mogelijk op kunnen lopen tot meer dan USD 265 miljard. Dat heeft het Amerikaanse kredietratingsbureau donderdag bekendgemaakt.

Hoewel de grote zakenbanken als Citigroup en Merrill Lynch momenteel verantwoordelijk zijn voor het grootste deel van de huidige USD 90 miljard aan afschrijvingen, zal de volgende ronde van afschrijvingen volgens S&P komen van de kleinere financiele instellingen in Europa, Azie en de Verenigde Staten.

Woensdag werden de ratings voor USD 534 miljard aan obligaties en schuldverplichtingen met onderpand, de zogenoemde CDO's, gerelateerd aan risicovolle hypotheken door S&P verlaagd of onder review geplaatst. Deze verlaging of review van de ratings door S&P zal volgens marktpartijen leiden tot verdere afschrijvingen op hypotheekgerelateerde investeringen door financiele instellingen.

Niet alleen het vertrouwen van de banken onderling is weg, het vertrouwen van de particulier in de banken is ook foetsie.

Zal dit de doorbraak betekenen van P2P lending?

Zal dit de doorbraak betekenen van P2P lending?

Maar kan je nou zomaar zo'n foreclosure huis kopen alsof het direct van een makelaar komt? Ik zie een huisje in centraal SF met een est. value van 500k voor 9k... dat kan toch niet kloppen

als ik het goed begrijp is de US een land vol met katvangers

Als je cheap een huiis in de US wil kopen heb je nu de kans

[ Bericht 37% gewijzigd door henkway op 31-01-2008 16:13:29 ]

Als je cheap een huiis in de US wil kopen heb je nu de kans

[ Bericht 37% gewijzigd door henkway op 31-01-2008 16:13:29 ]

|

|