WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

Beetje op de emoties spelenquote:Op vrijdag 21 augustus 2015 22:30 schreef WillemMiddelkoop het volgende:

[..]

Eens, maar 'More than 500 points' klinkt zo lekker dramatisch heKlinkt veel sensationeler dan -3%

Kun je uitleggen waarom het beleid van de Centrale Bank leidt tot dalende grondstofprijzen?quote:Op vrijdag 21 augustus 2015 20:00 schreef SeLang het volgende:

Olie (WTI front contract) nu onder de $40.

De olieboeren zullen nu wel flink zitten te lobbyen voor een nieuwe oorlog, ergens.

De gevolgen van catastrofaal centrale bank beleid kun je mooi zien in grondstoffen charts:

Boom en bust

[ afbeelding ]

[ afbeelding ]

Aandelen lijkt nog steeds nergens op, die lopen een beetje achter

De enige paar keren dat we een overwaardering hadden van deze omvang (1929, 2000 en 2007) eindigden allemaal in een daling van >50% vanaf de top.

[ afbeelding ]

The End Times are wild

Te goedkoop krediet > Overinvestering (nu 'Boom') > Overaanbod > Prijzen/winsten omlaag > Faillissementsgolf (nu 'Bust').quote:

Kun je uitleggen waarom het beleid van de Centrale Bank leidt tot dalende grondstofprijzen?

quote:

Wel heftig vandaag hoor. Wanneer was dit eerder?

I am a Chinese college students, I have a loving father, but I can not help him, he needs to do heart bypass surgery, I can not help him, because the cost of 100,000 or so needed, please help me, lifelong You pray Thank you!

Zelfs die grafiek geeft een te optimistisch beeld. Je moet het op een logaritmische schaal bekijken als je stijgingen en dalingen met elkaar wilt vergelijken:

Er is eigenlijk nog helemaal geen sprake van een daling. Meer een zijwaartse beweging sinds eind vorig jaar.

Er is eigenlijk nog helemaal geen sprake van een daling. Meer een zijwaartse beweging sinds eind vorig jaar.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

De AEX ook maar even met log schaal:

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

stomme vraag misschien maar waarom is log beter?

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Omdat bijvoorbeeld 100 punten daling vanaf 1000 een daling van 10% is en een daling van 100 punten vanaf 2000 maar 5% is. Op een lineaire schaal krijg je daarom een verkeerd beeld als je historische episodes met elkaar vergelijkt. Op een logaritmische schaal is eenzelfde verticale afstand op de chart overal hetzelfde percentage.quote:

stomme vraag misschien maar waarom is log beter?

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Weer wat geleerd. thanks!

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

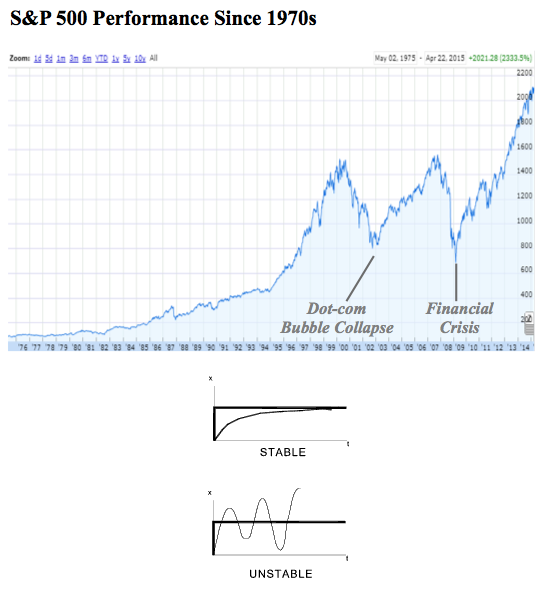

Overigens, mocht de top er inmiddels staan (geenzins zeker) dan verdient het wel een schoonheidsprijs kwa symmetrie.

Precies gelijke golflengtes voor elke boom en bust.

Techneuten herkennen hierin direct een instabiel regelsysteem, met de centrale banken als regelaar die een te hoge lusversterking toepast:

Je ziet het ook precies starten op het moment dat centrale banken (met name de Fed) echt activistisch begonnen te worden. Steeds grotere booms geven steeds hogere busts waardoor een nog weer grotere centrale bank reactie wordt uitgelokt, etc etc totdat het systeem tegen natuurlijke grenzen aanloopt. In een electronisch systeem is die grens vaak de voedingsspanning. In het centrale bank systeem is het wellicht ZIRP of schaarste aan assets die nog kunnen worden opgekocht (zie crash van EU bondmarkt dit voorjaar).

Of dit analogon klopt? Ik ben erg benieuwd...

Precies gelijke golflengtes voor elke boom en bust.

Techneuten herkennen hierin direct een instabiel regelsysteem, met de centrale banken als regelaar die een te hoge lusversterking toepast:

Je ziet het ook precies starten op het moment dat centrale banken (met name de Fed) echt activistisch begonnen te worden. Steeds grotere booms geven steeds hogere busts waardoor een nog weer grotere centrale bank reactie wordt uitgelokt, etc etc totdat het systeem tegen natuurlijke grenzen aanloopt. In een electronisch systeem is die grens vaak de voedingsspanning. In het centrale bank systeem is het wellicht ZIRP of schaarste aan assets die nog kunnen worden opgekocht (zie crash van EU bondmarkt dit voorjaar).

Of dit analogon klopt? Ik ben erg benieuwd...

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Dat weet geen hond. Maar iedereen ziet de symmetrie in het patroon. Daarnaast geven zelfs de die-hard bulls nu toe dat de markt extreem is overgewaardeerd. Niemand die long zit doet dat nog om economische redenen (wereldwijde business cycle is neerwaarts, bedrijfswinsten zijn in 2013-2014 al uitgepiekt, etc). De enige reden dat beleggers nog long zitten is de verwachting dat de centrale banken nog harder gaan pompen. Maar daar ben ik zelf niet zo zeker van. Er wordt langzaam aan een omslag zichtbaar in het denken bij centrale banken. Dat neemt niet weg dat ze misschien weer in paniek raken als het hard zou gaan dalen maar de vraag is of beleggers het dan nog geloven.quote:

Ik twijfel of we de top hebben bereikt idd Selang, wat denk jij zelf ?

Een ander probleem dat ik hier al eerder heb beschreven is dat in tegenstelling tot 2000 en 2007 nu door nieuwe bankregels banken tijdens een daling in veel mindere mate als kopers kunnen optreden, want ze mogen die risico's niet meer nemen. De markt is veel minder liquide dan het lijkt. Dus wie gaat die overgewaardeerde troep straks kopen? Ik sta wel klaar om te kopen maar dan praten we wel over een S&P500 met 3 cijfers voor de komma in plaats van 4 voordat ik überhaupt een lijstje begin te maken.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

SeLang, wat denk je van dit stukje?

De schrijver stelt dat de FED genoodzaakt is om de korte rente op te laten lopen vanwege laddered bondportfolio's en de looptijd van QE asl ik het goed gelezen heb.

De schrijver stelt dat de FED genoodzaakt is om de korte rente op te laten lopen vanwege laddered bondportfolio's en de looptijd van QE asl ik het goed gelezen heb.

Dat lijkt me de nagel aan de doodskist voor deze bullrun.quote:The Fed, QE, Rates And You*

I made this point in a couple of Tickers, and in the presentation last night. It's grossly contrary to "mainstream" opinion, and I want to explain it.

Now of course things can change, and only a fool doesn't change his opinion when the facts underlying it turn out to be different than expected. But with that said....

The Fed will cease QE on schedule. The taper is not only on, it won't be suspended. And, withdrawing liquidity, that is, allowing short rates to rise, is on the table too, and almost-certainly sooner than you think.

It doesn't matter if the market sells off, even if it sells off hard.

Here's why.

If you remember I have repeatedly pointed out the utter insanity of QE in the first place. It is much like snorting heroin -- you get a high immediately but the price is spread out. That's for the simple reason that bond portfolios work that way.

In other words, with the possible exception of a few small individual "investors" who buy a single bank CD, nobody (in their right mind anyway) buys just one bond. This is particularly true of large investment pools and those who underpin the bond market, such as insurance companies and pension funds.

All of these entities ladder their bonds.

If you're unaware of how this is done, it's simple -- the people who buy these things want a more-or-less "constant duration" because they are intending to meet some expected expense with the interest coupon. They attempt to match that duration against their perceived risk, and adjust for interest rate environment both today and what they expect tomorrow.

So let's say that after much grinding of numbers Insurance Company "A" determines it needs a 10 year duration in its portfolio in order to earn the return it wants, hedge the risk it wants, and match the two against incoming cash flows and expected claim payments.

Starting out (when the company is formed) it thus buys a set of bonds that look more or less like this:

10 year bond, 1 year to maturity.

10 year bond, 2 years to maturity.

10 year bond, 3 years to maturity.

and so on.

Now they might mix some stuff up in here too; if you think the curve is going to steepen (that is, long rates go up more than short) you would prefer to buy a 5 year bond with 3 years to maturity over a 10 year one, all things being equal (but of course they never are because the yields at those two times of issue were almost-certainly different!) The point, however, is that what you end up with in the portfolio looks like this:

10% has 1 year to maturity.

10% has 2 years to maturity.

And so on.

By the way, individual investors with a lot of money do this too. It's very popular among muni investors, for example, provided you have enough money to make it work (six figures for starters, on up) because individual bonds are typically sold in $10,000 increments and if you have enough to capital to do it you can pick exactly what risks you want as opposed to buying a mutual fund where someone else makes those decisions.

So now The Fed comes in and does QE, buying the long end. What happens? Long rates go down. A year on your 1 year to maturity bonds mature, and you must replace them. With what will you replace them? All things being equal, when you replace them you will get less interest income from the new issues.

So let's say the effect of QE is that your mortgage goes from 6% to 3%. This is a 50% reduction in your interest payment. But -- that MBS gets sold into the market. MBS have a typical maturity profile of about 7 years (which is why the 10 is the benchmark; it's the closest), fluctuating somewhat. When rates are high and falling the profile is shorter (because people refinance), when rates are low and going higher it extends (because you're a nut to refinance a 3% loan into a 4% one -- nobody does that unless you have to sell and move for some reason.)

So the guy who buys it gets a 50% reduction in his interest income, but that's only 1/10th of his portfolio. For the first year, anyway. As such his impact the first year is 5%, then 10%, then 15% and so on.

We're roughly five years into this crap now.

The pension funds and insurance companies that are the backbone of this market are probably doing plenty of screaming, and with good cause. If this keeps up their cash flow will collapse; they can't absorb it. Further, Bernanke and the rest of the Fed know that factually the damage they took on by buying those instruments during QE cannot be gotten rid of either; it has to roll off, because if you sell that bond you're going to take a capital loss and crystallize the entire loss right now instead of spreading it out!

This is what is forcing the end of QE. It is also what is going to force The Fed to pull liquidity and let the short end come up.

They don't have a choice but they will never breathe a word of this, because to confirm it would be to give a clean opportunity to gang-bang all those bondholders by Hedge Funds and others who can play in the derivatives market, and that could (read: probably would) set off a crisis far worse than 2008.

That's my read on it.

We'll see, over the next months, if I'm right.

Escaping from a liquidity trap may be impossible, much like light trapped in a black hole.

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Op zaterdag 19 november 2011 13:27 schreef Perrin het volgende: En net als van voetbal, heeft iedereen verstand van macro-economie

Prachtig verslag. Ik heb het ook doorgestuurd naar m'n moeder. Je hebt mij inspiratie gegeven voor volgend jaar.quote:

* SPAM *

Nieuw deel uit de serie: "What to do with the f*cking money?"

TRV / [Reisverslag] Kungsleden trek (420 km door Arctisch Zweden)

Ik denk ook dat ze gaan hiken, maar niet veel. Zoals je hieronder ziet prijst de obligatiemarkt dat ook in:quote:

SeLang, wat denk je van dit stukje?

De schrijver stelt dat de FED genoodzaakt is om de korte rente op te laten lopen vanwege laddered bondportfolio's en de looptijd van QE asl ik het goed gelezen heb.

[..]

Dat lijkt me de nagel aan de doodskist voor deze bullrun.

Wat interessant is is dat de laatste maanden de korte rente stijgt en de lange rente daalt. Het zou me niet verbazen als die trend zich voortzet (wijst op recessie).

Het probleem voor de Fed is dat ze wil normaliseren maar eigenlijk is dit het verkeerde moment want ze hebben een hele businesscycle overgeslagen en renteverhoging is in feite pro-cyclisch. Je ziet ook dat de TIPS over de komende 5 jaar gemiddeld slechts 1,17% inflatie inprijst. Dat is de helft van wat de Fed wil.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Dit is wel humor. "Help us out"

...in combinatie met deze grafiek, waarop er gewoon echt niets aan de hand is. Of eigenlijk juist wel: het ontbreken van een gezonde correctie in een markt die schreeuwen duur is!

Voor wie Suze Orman niet kent, dat is zo'n self made financiele goeroe die allerlei bestsellers heeft geschreven voor Henk en Ingrid over "how to get rich". Als dat soort mensen nu al in paniek begint te raken dan wordt het nog lachen!

[ Bericht 3% gewijzigd door SeLang op 23-08-2015 10:00:15 ]

...in combinatie met deze grafiek, waarop er gewoon echt niets aan de hand is. Of eigenlijk juist wel: het ontbreken van een gezonde correctie in een markt die schreeuwen duur is!

Voor wie Suze Orman niet kent, dat is zo'n self made financiele goeroe die allerlei bestsellers heeft geschreven voor Henk en Ingrid over "how to get rich". Als dat soort mensen nu al in paniek begint te raken dan wordt het nog lachen!

[ Bericht 3% gewijzigd door SeLang op 23-08-2015 10:00:15 ]

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Ik wil voor de lange termijn, ben nu 25 en tegen mijn pensioen wil ik een aardig vermogen hebben opgebouwd. Dus een horizon van ruim 40 jaar misschien wel.quote:

Omdat ik niet heel veel verstand heb van beleggen wil ik met name in trackers beleggen. Ik moet nog uitzoeken hoe ik dat precies samen ga stellen. Een aantal wereldwijde trackers, misschien een bepaalde bedrijfstak of ook wat AEX. Hoe kan ik dat het beste bepalen?

AEX 427,630 -15,24 -3,44%

Zo, de TT is wel heel ver weg nu.

Zo, de TT is wel heel ver weg nu.

Never in the entire history of calming down did anyone ever calm down after being told to calm down.

Whut??quote:Op maandag 24 augustus 2015 09:08 schreef Arcee het volgende:

AEX 427,630 -15,24 -3,44%

Zo, de TT is wel heel ver weg nu.

Olieprijs (WTI front contract) $39,20

Saudi Arabië schijnt nu een begrotingstekort te hebben van bijna 20%

Saudi Arabië schijnt nu een begrotingstekort te hebben van bijna 20%

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Vandaag?quote:

Gaan weer rap. Zouden we de 400 halen?

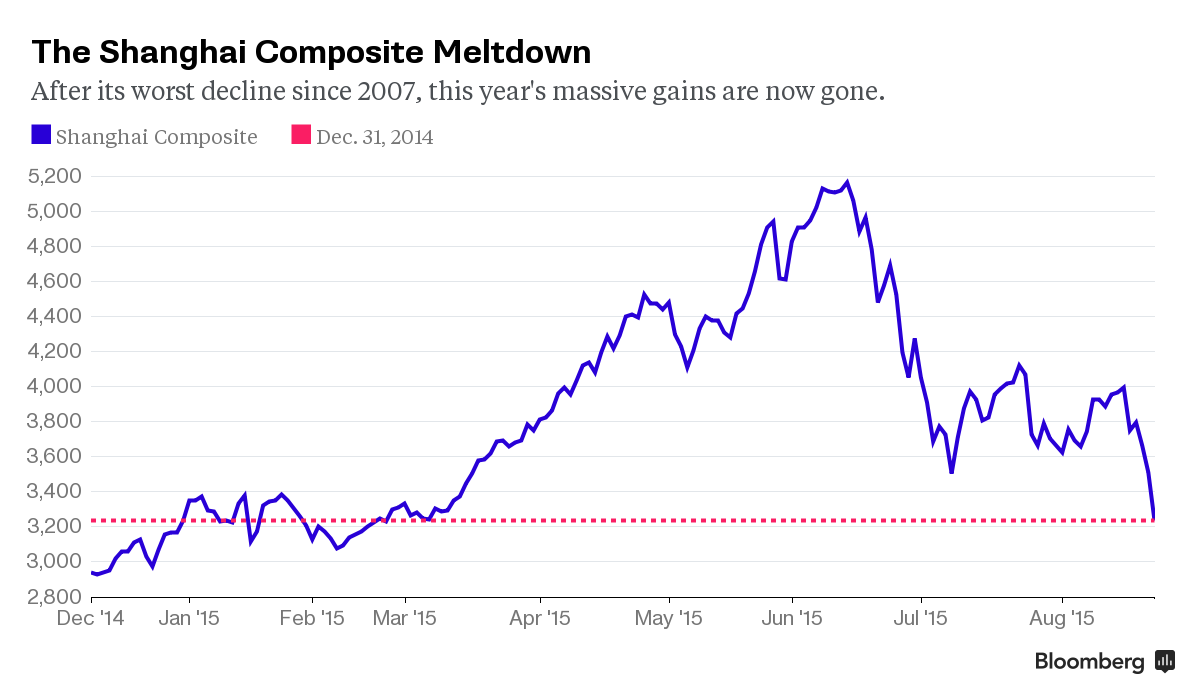

Ik hoop maar dat die bananenverkoper op tijd is uitgestaptquote:Shanghai Composite preliminary close down 8.5% at 3210, biggest fall since 2007

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Op

Op

Ik heb een fors deel van mijn obligaties verkocht en ben weer long gegaan op de AEX. Het bloed vloeit, dus dat is goed.

The End Times are wild

Eigenlijk stelt het niks voor. Shanghai -8.5% vandaag, maar dan ben je gewoon terug op het niveau van maart dit jaar. Die koersexplosie van maart-juni sloeg sowieso nergens op.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Ik geloof dat alles zo ongeveer terugstaat op de koers van Feb-Mrt dit jaar, dus valt allemaal wel mee. Alleen dat het in een week gebeurt tov dat half jaar is gewoon effe heavy.

Het is opmerkelijk dat die sterke daling in Azie in juni/juli de Europese beurzen relatief onberoerd gelaten heeft.

The End Times are wild

Hoezo niet leuk? Aandelen in de uitverkoop. Rendementen stijgen. Je kon eigenlijk niks meer kopen omdat alles overgewaardeerd was. Nu (of wat later) heb je je kans.quote:

Nog steeds is er geen fatsoenlijk rendement te halen met rente. Dus blij dat er weer een alternatief is.

The End Times are wild

De Chinese beurs op zich boeit niet erg want dat is vooral een lokale aangelegenheid. De Chinese "echte" economie is wel erg belangrijk voor ons. Natuurlijk heeft een aandelen crash in China daar indirect wel invloed op maar dat is een tweede orde effect.quote:

Het is opmerkelijk dat die sterke daling in Azie in juni/juli de Europese beurzen relatief onberoerd gelaten heeft.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Euro alweer bijna $1,15. Ik ga nog gelijk krijgen met mijn thesis dat iedereen daar te pessimistisch over was (zo'n beetje de hele financiële wereld schreef dat de euro richting $0,80-$0,90 zou gaan). Mijn reden daarvoor was dat de economische sterkte van de VS wordt overschat en dat het renteverschil met de EU zou gaan krimpen, wat de euro steunt. Dat is exact wat je nu ziet gebeuren.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Als de geschiedenis een leidraad is dan ga je met aandelen op de huidige waardering over de komende ~10 jaar niet meer verdienen dan met een spaarrekening. Ondanks een paar procent daling is dit nog steeds een extreme overwaardering.quote:

[..]

Hoezo niet leuk? Aandelen in de uitverkoop. Rendementen stijgen. Je kon eigenlijk niks meer kopen omdat alles overgewaardeerd was. Nu (of wat later) heb je je kans.

Nog steeds is er geen fatsoenlijk rendement te halen met rente. Dus blij dat er weer een alternatief is.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Ik denk dat je PE/Shiller ook moet afzetten tegen de rente. De rente daalt al 20 jaar. Met een structureel lagere rente (en ik zie geen motivatie voor de centrale banken om de rente terug te brengen naar het niveau van 2000 of daarvoor), zou een lagere PE ook acceptabel moeten zijn.quote:

[..]

Als de geschiedenis een leidraad is dan ga je met aandelen op de huidige waardering over de komende ~10 jaar niet meer verdienen dan met een spaarrekening. Ondanks een paar procent daling is dit nog steeds een extreme overwaardering.

Verder zijn de waarderingen nog steeds hoog hoor, dat zal ik niet ontkennen.

The End Times are wild

De kapitaalmarkt rente (dat is degene die er toe doet) is nu niet lager dan in de jaren '50 toen de Shiller P/E minder dan de helft was.quote:

[..]

Ik denk dat je PE/Shiller ook moet afzetten tegen de rente. De rente daalt al 20 jaar. Met een structureel lagere rente (en ik zie geen motivatie voor de centrale banken om de rente terug te brengen naar het niveau van 2000 of daarvoor), zou een lagere PE ook acceptabel moeten zijn.

Verder zijn de waarderingen nog steeds hoog hoor, dat zal ik niet ontkennen.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Goedkope shiller niveaus is imo wel een gevalletje 'this time is different'. P/e van <10 is zo'n inefficiency in principe dat de investeerder van vandaag het niet meer zover laat komen en al snel weer gaat lopen kopen.

Ik bedoel de generatie van mij (20-30) hebben al twee crises meegemaakt; mij maak je niet meer gek als het iets in elkaar valt.

Ik bedoel de generatie van mij (20-30) hebben al twee crises meegemaakt; mij maak je niet meer gek als het iets in elkaar valt.

Je hebt dus eigenlijk nog bijna niks meegemaakt want die 2 crises vielen binnen één economisch "regime". De wielen gaan er pas af als dat regime verandert. Dat is inderdaad de klassieke "this time is different" fout, dat mensen denken dat het huidige paradigma (in dit geval "almachtige" centrale banken, schuld doet er niet toe, lage munt = goed, inflatie = goed, etc) altijd zo zal blijven. Maar de geschiedenis leert dat zoiets maar een beperkte tijd duurt en dan krijg je weer iets anders.quote:

Goedkope shiller niveaus is imo wel een gevalletje 'this time is different'. P/e van <10 is zo'n inefficiency in principe dat de investeerder van vandaag het niet meer zover laat komen en al snel weer gaat lopen kopen.

Ik bedoel de generatie van mij (20-30) hebben al twee crises meegemaakt; mij maak je niet meer gek als het iets in elkaar valt.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Olieprijs $38,xx

Laagste sinds feb 2009

Laagste sinds feb 2009

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Dit is wel goed voor Fok! trouwens. Jammer dat dit dipje niet een paar maanden eerder kwam, dan hadden we het forum misschien kunnen behouden.

De ondergang van het AEX forum is de schuld van de centrale banken

De ondergang van het AEX forum is de schuld van de centrale banken

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Die neergang in grondstoffen is al erg lang aan de gang

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Zou Warren Buffett zijn eigen principes nog volgen of vertrouwt hij nu ook alleen nog maar op een nieuwe redding door de Fed?

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Als je nu eens het WGR forum flink vol gooit met ter zake doende aex topics, misschien dat er een paradigma shift in het fok beleid plaats vind en men het oprichten van een aex forum wel een goed idee vindt.quote:

Dit is wel goed voor Fok! trouwens. Jammer dat dit dipje niet een paar maanden eerder kwam, dan hadden we het forum misschien kunnen behouden.

De ondergang van het AEX forum is de schuld van de centrale banken

Het is natuurlijk koffiedik kijken, maar ik denk dat de markten bij een nieuwe downturn amper nog reageren op nieuwe stappen van de FED (als die al komen, zal dat niet tijdig zijn). De FED is dan uitgespeeld. Een nieuwe downturn zal de perceptie van omnipotente CB doen ploffen. Ik denk dat nog een heleboel mensen staan te kijken over het wrakhout dat bij een nieuwe recessie komt bovendrijven.

In het afgelopen jaar is die perceptie al duidelijk aan het draaien. Niet alleen buiten de Fed maar het lijkt ook zo te zijn binnen de Fed en andere relevante instituten. Onlangs schreef een hoge pief binnen de Fed nog dat QE had gefaald. Het BIS kwam begin dit jaar met een rapport dat er geen aanwijzingen zijn dat CPI deflatie slecht is behalve als die het gevolg is van klappende asset bubbles en dat het beleid zich dus moet richten op het voorkomen van de vorming van asset bubbles.quote:

Het is natuurlijk koffiedik kijken, maar ik denk dat de markten bij een nieuwe downturn amper nog reageren op nieuwe stappen van de FED (als die al komen, zal dat niet tijdig zijn). De FED is dan uitgespeeld. Een nieuwe downturn zal de perceptie van omnipotente CB doen ploffen. Ik denk dat nog een heleboel mensen staan te kijken over het wrakhout dat bij een nieuwe recessie komt bovendrijven.

Vandaag weer een stukje van SocGen (via ZeroHedge):

Tegenwoordig lees ik dit soort dingen bijna dagelijks. Een jaar geleden was dat echt nog niet zo!quote:Less confidence in central bank puts

As noted above, the most notable feature of recent market price action is that there has been no visible comfort taken on risky assets from the idea that central banks may step in with further liquidity injections to alleviate the situation. To our minds, this reflects two main points. First, the fact that the tremendous amounts of liquidity injected to date have produced less than spectacular economic results. Clearly, markets have lost faith in the ability of unorthodox monetary policies to kick start the economy over time. This also fits the findings of academic literature suggestion diminishing returns from subsequent rounds of QE. Second, central banks have clearly become more concerned about the potential risks to financial stability from indefinitely inflating asset prices, suggesting that they may be slower to step in.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

ja maar ik had dus nog aandelen he...quote:

[..]

Hoezo niet leuk? Aandelen in de uitverkoop. Rendementen stijgen. Je kon eigenlijk niks meer kopen omdat alles overgewaardeerd was. Nu (of wat later) heb je je kans.

Nog steeds is er geen fatsoenlijk rendement te halen met rente. Dus blij dat er weer een alternatief is.

Linkse beleggers in paniek!

AEX -5%

AEX -5%

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen