WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

Mish

Alle bailouts ten spijt... we zaten er al vorig jaar in.

Wat ik al een tijdje roep.... na LEH zitten we al in een systeemcrash. Zoiets gaat niet van *plof*... maar de gevolgen zijn nu wel duidelijk nu ook de reele economie aan de hefboom begint te drukken.quote:US banks levered cash to loans at 25:1 and liabilities at 33:1 at the credit bubble peak. The long term historic average ratios are about 5-7:1, and 7-10:1 respectively.

Moreover, historically, the ratio of real estate loans to cash averaged 1.25 to 2 (!!!) on a sustained basis, whereas the ratio at the unprecedented hyper-leveraged point in 2007-2008 reached 12-13:1, with real estate loans as a share of all bank loans reaching almost 60%. Real estate loans/GDP topped out at 26-27% (!!!).

Were the banks' cash ratio to "unreal" estate loans to return to the historically sustainable range, banks would either need to (1) triple and quadruple their cash assets from $1T to $3T-$4T and/or (2) write down real estate assets commensurately or a combination thereof.

Wells Fargo is loaded to the rafters with eventually non-performing residential and commercial real estate loans in the US Pacific Northwest the last region of the country to enter the Kuznets Cycle bust to date.

Consider what virtually no growth in real estate loans combined with a tripling or quadrupling of banks' cash assets means to the real estate market and US overall investment, consumption, government receipts, and payrolls going forward.

The negative effects of bank liquidation and reverse leverage risk outright systemic collapse.

Alle bailouts ten spijt... we zaten er al vorig jaar in.

Er zijn te veel fusies, te veel bedrijfskunde studenten en ook te veel zakenbanken. (en dit alles omdat er waarschijnlijk te veel geld in de economie gepompt is)

En wij zijn zo stom om dit zooitje een bailout te geven.

[ Bericht 4% gewijzigd door TubewayDigital op 25-01-2009 00:27:24 ]

En wij zijn zo stom om dit zooitje een bailout te geven.

[ Bericht 4% gewijzigd door TubewayDigital op 25-01-2009 00:27:24 ]

Santander valt positief op, ondanks de overname van delen van ABN.

Waar slaat de vergelijking met tosti's op ?

?

Waar slaat de vergelijking met tosti's op

Op maandag 30 november 2009 19:30 schreef Ian_Nick het volgende:

Pietje's hobby is puzzelen en misschien ben jij wel het laatste stukje O+

Pietje's hobby is puzzelen en misschien ben jij wel het laatste stukje O+

Toast !quote:Op zaterdag 24 januari 2009 21:52 schreef PietjePuk007 het volgende:

Santander valt positief op, ondanks de overname van delen van ABN.

Waar slaat de vergelijking met tosti's op

Multiply it by infinity, and take it to the depth of forever, and you will still have barely a glimpse of what I'm talking about.

Jammer dat ING niet is opgenomen die heeft op een gegeven moment toch ook een market kap gehad van +60miljard . Fortis was ook best groot dacht ik, maar ja die kan je niet mee opnemen omwille van de totale verdeeldheid nu, Frotis was trouwens iets kleiner dan ING.

Omdat ze zo slim waren die meteen weer door te verkopen.quote:Op zaterdag 24 januari 2009 21:52 schreef PietjePuk007 het volgende:

Santander valt positief op, ondanks de overname van delen van ABN.

Waar slaat de vergelijking met tosti's op

Heel simpel....een boel banken lees grote banken zijn verdomd. Door hun verliezen en afschrijving enop de assets/aandelen is hun eigen vermogen zo goed als weg. Alle steunoperaties ten spijt. Technisch zijn deze banken niet of nauwelijks solvabele te noemen. Deleveraging waarmee ?!. Er is niet veel meer nodig om ze te laten struikelen.quote:Op zondag 25 januari 2009 12:18 schreef SjonLok het volgende:

Ik snap de relatie tussen de afbeelding en de tekst niet. Kan iemand me dat uitleggen.

En de economische neergang is pas net begonnen (dat worden weer flinke afschrijvingen).

Zover zelfs dat banken genationaliseerde instituten worden.... en de laatste bubble (die je nog kunt bedenken) flink wordt opgeblazen.. Staatsobligaties... daarna kun je de schuld op niemand meer afwentelen.

[ Bericht 6% gewijzigd door Drugshond op 25-01-2009 16:38:47 ]

No comment...quote:Bernanke: Game Over?

Bloomberg is allegedly reporting that Bernanke is "contemplating" buying the long end of the Treasury Curve due to "bond market instability."

Here's what he's unhappy about:

There is nothing "unstable" about any of this. Rates are going higher. Why? Gee, let's see, Obama says he's going to blow $1 trillion on a "stimulus" package, the other $350 billion of the TARP was released, the GAO says we're going to run well north of a Trillion in deficits, and people are wondering why the bond market expects the government to pay up in higher interest rates for the right to borrow more than 10% (and that's almost certainly a LOW estimate) of the total outstanding debt in one freaking year after having added 16% in the last one?

You're kidding, right? America is acting like a subprime credit-card customer who has decided to go nuts in the local "bigbox" electronics retailer, and the market is (appropriately) reacting to that by repricing RISK.

Bernanke thinks he will simply cap the market by intervening?

Let us dwell for a few minutes on how our government financials and currency actually work.

Treasury prints up T-Bills which it then sells. The Fed is the purveyor of currency, which it produces by buying T-bills with "newly minted" dollars, expanding the total amount of dollars in the system when it so chooses.

Ok.

The market determines all interest rates. Yes, even the "Fed Funds" rate; if you think The Fed leads the market, you need to go study some charts. The Fed does not set rates, it is compelled to follow the market, because if it tries to force rates to where they do not want to go it can obtain that result in exactly two ways:

1. It must provide or draw an infinite amount of money into or out of the system in order to drive and maintain it outside of equilibrium OR

2. It must crowd out all private parties from a particular area of investment, thereby allowing The Fed to effectively "take over" from private parties.

The second is non-intuitive - you need to contemplate how the markets (for anything) work for a few minutes before it makes sense.

Consider a situation where The Fed "wants" the GSE funding cost to be, say, 2%. The market wants it to be 4%, because the market perceives more risk than The Fed would like to have it admit.

The Fed can cause the GSE paper to trade at 2%, but if it does so it will be the only buyer of said paper, because nobody else will buy at a 2% coupon.

The same thing is about to happen here. If Bernanke actually attempts to suppress the Treasury Market's interest rates, that is, "support the long end of the curve's price", then he will wind up having to buy all, or essentially all, of the supply. People who own Treasuries will sell to him, surmising that he is overpaying, and gleefully taking what is an "extra" profit from his hands.

If you're wondering why the commercial and consumer lending market has gone straight to hell, this is the reason. Bernanke has interfered with the private credit market in virtually every area, and in each place where he has "supported" the price of debt instruments (suppressing yields) he has wound up as effectively the only buyer in short order.

This is bad when we're talking about the private credit markets but if it shifts to Treasuries then the game is literally over immediately, because at that point you have just created a circle jerk.

Treasury prints Ts to finance its operations but the guy who buys them is the guy who prints the money in exchange. Therefore every additional Treasury sale is no longer a debt sale, it is an act of printing money by the Central Bank and destroys the standard of living of everyone in The United States.

This, should Ben engage in it, is a willful act of destruction of your private property rights, your wealth, and your income. It is not an accident, it is not "necessary" and it solves exactly nothing.

It is simply an attempt to defraud - yet again - the American People, this time by attempting to "make ok" the financing of deficit spending that the market simply will not support at the price Treasury wishes to pay.

Down this road lies the near-immediate implosion of all commercial credit as there will no longer be a "fair" reference against which it can be based. We've already tampered with the commercial paper and mortgage security markets; this will complete the "transition" from a market economy in bonds to a command economy, complete with a self-appointed King who has simply ignored the provisions of The Federal Reserve Act when it suited him.

Bernanke will literally have reached the end game where he is the lender not only of last resort, but of the first and only resort at the same time, with all of his lending "decisions" being made by fiat instead of by the market's approximation and evaluation of risk.

Once this begins expect mass bankruptcies in the commercial sector as private credit provisioning will immediately disappear. Bernanke's ability to replace that functionality is fanciful and he will soon learn this lesson the only way the market knows how to teach it - the hard way - just as he has had every other "plank" in his Doctoral Thesis destroyed - one at a time.

No, it is not inflationary when your job disappears because the place you work for goes under; while Ben can try to replace the entirety of the private credit market I wish him the best of luck in that endeavor, given that it is some fifty trillion dollars. How much faith will the world have in The Fed when it tries to backstop a $50 trillion marketplace with under $1 trillion in banknotes? It has already doubled its balance sheet - but this would require expanding it by twenty five more times.

He's going to fail at this endeavor in truly-spectacular fashion.

maar bere interessant en het einde want vanaf dat moment wordt alles gedumpt.quote:

“Snowboarding is an activity that is very popular with people who do not feel that regular skiing is lethal enough.”

En het failliet van een land/staat.quote:Op dinsdag 27 januari 2009 14:02 schreef shilizous_88 het volgende:

[..]

maar bere interessant en het einde want vanaf dat moment wordt alles gedumpt.

Zit ff te denken over de definitie van inflatie/deflatie... (BBB-reeks, zie simmu). Maar past hier ook wel bij.

Een of ander staat of valt met de bijbehorende schuldenlast in correlatie met de valuta en correctief vermogen.

Denk niet dat veel landen de illusie hebben dat de schuldenlast van Amerika oplosbaar is (nu niet... nooit niet). Tenminste niet in papierenvorm die na tig jaar opgeblazen kunnen worden door hyperinflatie (waardoor ze waardeloos worden). Anderzijds doen veel landen nu een beetje hetzelfde met soort gelijke bailouts of drop in commodities in vergelijking tot hun BNP waardoor er een offset/tijdvertraging of zelfs van buiten hun systeemgrenzen een negatieve versterking optreedt (Oostblok, Iran e.d.). En nu is het een darwinistisch systeem geworden (van wie kan het langste nog geloofwaardige garanties afgeven die de markt nog kunnen prikkelen). Feitelijk kun je beter spreken van "Everybody Must Get Stoned - B.Dylan"-systeem of je nu door de hond of de kat gebeten wordt.

Dus het blijft zeker niet bij Amerika alleen.... hoewel de volgende prikkel hoe idioot ook wel weer eens uit Amerika zou kunnen komen. Ze hebben een president die leuk kan speechen, en een leger/backbone waar je oh' tegen zegt.

Wellicht kun je beter terug blikken naar wat geschiedenislessen... In de middeleeuwen kende veel volkeren ook wel eens tegenslagen... maar no way dat ze hun rijkdom klakkeloos overgaven. Dat ging altijd te voet of te paard met wat strijd.. (iets wat we wellicht ook terug zullen zien).

Diegene die straks de strategische assets hebben = king. Of dat nu goud, olie of diamanten zijn is om het even. Qua bully-talk kan Amerika ons op korte termijn veranderen (zoiets is nu al een beetje bezig tegen MO en nu met China (sinds Obama)... van back off).

[ Bericht 0% gewijzigd door Drugshond op 27-01-2009 14:52:55 ]

En nu ff in een suck-it mode / blog modus.

quote:American Debtor Psycho: $49 Trillion in Debt. The Real Reason why the Credit Crisis is Bigger than you Think.

This report may come as a surprise to you. It is often thrown around that we as a nation are heavily in debt. We hear the words billions and now even trillions being thrown around with really no breakdown of where the debt is flowing to. In this article, we are going to breakdown every single major area of debt in our country. You will soon realize why the credit crisis has the potential to be much bigger than once thought.

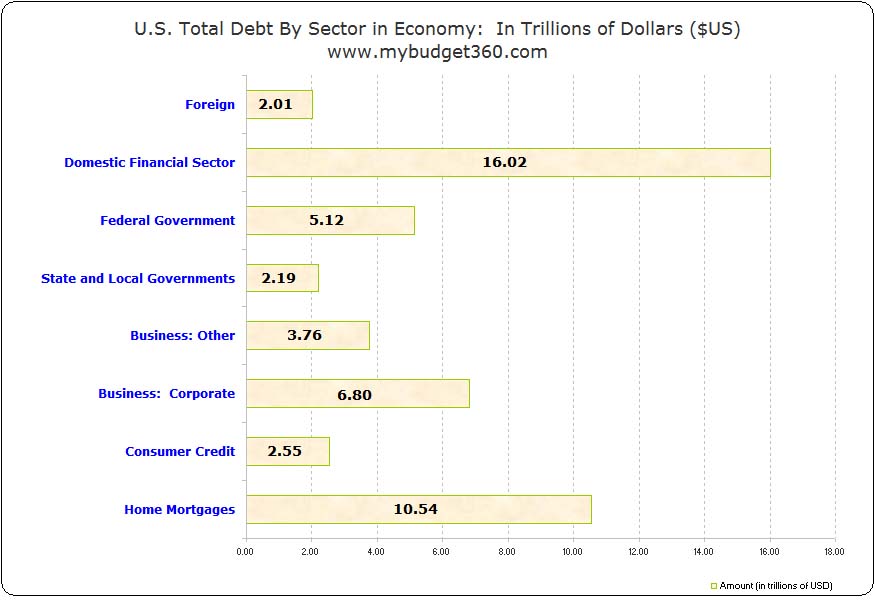

There are 8 major areas where Americans are heavily in debt. When most Americans think of the total debt outstanding they usually think of the U.S. National Debt which has gone over $10 trillion recently and is increasing at an alarming rate of $3.4 billion a day. Yet there are more troubling areas that even dwarf this astounding number. Overall there is $49 trillion in total outstanding debt in the United States.

I have constructed a graph highlighting the 8 major areas from the latest Federal Reserve Flow of Funds Account which was released late last month:

Total US debt

Debt Area #1 - Foreign

Amount: $2.01 Trillion

This is one of the smaller areas (if you can call $2.01 trillion small). Foreign debt as represented in the Federal Reserve report is amounts borrowed by foreign financial and non-financial entities in U.S. markets only. Given the global nature of this credit crisis you will understand why it was so vital for a global concentrated effort to provide funds across the world. That is why many counties in the Euro-zone have recapitalized their ailing financial industries during this credit crisis. Just as there are foreign firms in the U.S. that borrow heavily within our markets, we have our own companies in foreign locations that borrow heavily as well. We are all coupled together in this mess.Debt Area

#2 - Domestic Financial Service

Amount: $16.02 Trillion

This is buy far the largest sector of debt in our country. So when you hear about the massive injections to Wall Street, you can see that it also goes to the most heavily indebted area. Main Street Americans get a lot of flack from Wall Street types trying to usher the blame onto people who didn’t live within their means. Clearly, we rarely hear about this number in the mainstream media probably because most of these people also own a part of the media stations. You wouldn’t bite the hand that feeds you right? Easier to blame consumer debt for all this mess. This is also a major reason why the Fed has also stepped in to inject major capital into 9 of the largest U.S. banks in effect nationalizing a part of the institution. Do you see the Fed injecting money into your bank account? Probably not.

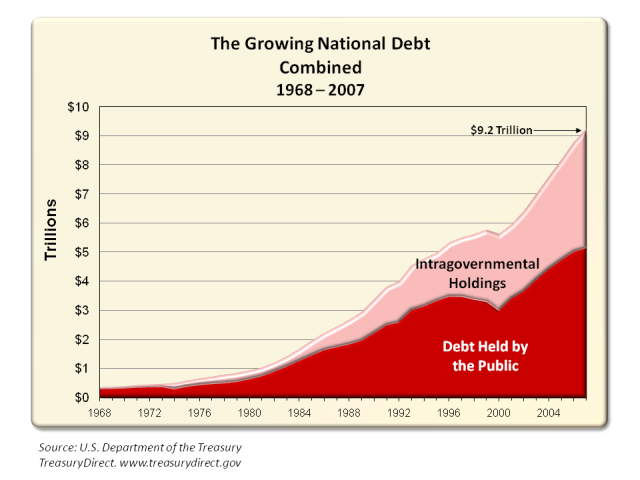

Debt Area #3 - Federal Government

Amount: $5.12 Trillion

What is often quoted in the media is the $10+ trillion in national debt. This is probably the most cited number of the entire $50 trillion outstanding. However, the reality is that approximately $4 trillion of this amount is actually future commitments to programs such as Social Security and Medicare while over $5 trillion is held by the public. The best chart I have seen on this is incredibly by Ross Perort:

Whatever you may think of his politics at least he does a good job explaining the massive debt floating out there. Keep in mind the above chart does not have the recent bailout bill which already has increased the debt ceiling to $11.3 trillion. Not a good sign.

Debt Area #4 - State and Local Governments

Amount: $2.19 Trillion

States like their big daddy in the Federal government also have no modulation on spending control. They also spend with no censorship. One perfect example of this is California. The state stalled out and had its longest budget stalemates. Finally, the budget was signed with a patchwork of piecemeal agreements. It was kick the can down the street plan. This plan didn’t even last a few weeks and the state had to go out and issue $5 billion in bonds simply to stay liquid. Welcome to the perpetual motion of debt on top of debt. Would you expect anything different from states when the Federal government is setting a culture of crony capitalism? That is, bail out the major financial sectors while letting the average American family fall further and further behind.

Debt Area #5 - Business: Other

Amount: $3.76 Trillion

The new model of business is high leverage. Even during the credit crisis, we were hearing stories about certain small businesses who were unable to pay their bills or meet payroll because of the freeze up in the credit markets. These people are also leveraged to the hilt. Everyone is nuts with debt!

Debt Area #6 - Business: Corporate

Amount: $6.8 Trillion

Corporate folks are notorious for going into debt. All you need to do is pull up a few random companies from the Dow Jones Industrial Average and we can quickly see how much debt is on their books:

Caterpillar Inc: $50.9 billion in total liabilities

General Electric: $717 billion in total liabilities

Johnson and Johnson: $41 billion in total liabilities

Now this isn’t to say they are in trouble. For example, a solid company should have a strong total equity base. For example, Johnson and Johnson has total assets of $88 billion so they have a total equity value of $46 billion.

total assets - total liabilities = total equity

But again, this is to highlight how dependent our society is with credit. The credit markets freezing up impact every single area of what we now know of as our hybrid market system. I hesitate to call it a free market since we are seeing a mix of corporate socialism here. Hardened free market fundamentalist have a hard time saying socialism especially when they are the ones calling for it. But that is what it is. Look at what was done with the domestic automakers. This was the same thing that was done for the big financial institutions.

Debt Area #7 - Consumer Credit

Amount: $2.55

You would think that this area would be bigger but it looks small in relation to the other areas. Yet this area has the biggest perceptible bang for the buck. In this area we have auto loans and credit cart debt. You will also find student loan debt here. The growth in this area is really astonishing. We went from $1.5 trillion in 1999 to $2.55 trillion currently. Why this is astonishing is that Americans have seen stagnant wages over this time. What this means is the American consumer used debt to keep their quality of life up. A façade that couldn’t last forever. Many reports state that consumption is roughly 70 percent of our GDP:

GDP = consumption + gross investment + government spending + (exports - imports)

With a GDP of $14 trillion this would be a very large amount of money. Now given that folks also purchase things in “cash” for example groceries, gas, or maybe tickets to a ball game, not everything bought is put on the plastic. Many folks are simply taking out I.O.U.s for instant gratification. This is now coming to a stunning and spectacular halt. The consumption side of the equation is now faltering badly. A widely watched report showed that retail sales fell 1.2% last month causing the market to slump drastically the day the report was issued. This area in fact may be the next major shoe to drop. Many Americans are now using one credit card to pay another one off doing a financial juggling act only destined to have all balls drop sometime in the near future. With a deteriorating employment situation where is the money going to come from?

Debt Area #8 - Mortgage Debt

Amount: $10.54 Trillion

This may be the most troubling of all the above sectors because it hits many Americans squarely in their largest financial investment. Seeing your equity disappear while your debt remains the same is not pleasant. The Case-Shiller Index which is now widely used to view price changes is off by 19% from its peak price. Given that at the peak it was estimated that U.S. residential wealth was at $24 trillion, we now have seen $4.5 trillion in housing equity disappear:

$24 trillion x 19 percent = $4.56 trillion in equity gone from peak

What this does is it also hurts the financial ratio of equity to debt with a homeowner:

Peak: $10 trillion debt / $24 trillion real estate value = 59% equity in homes

Current: $10.54 trillion debt / $19.44 trillion real estate value = 46% equity in homes

So what happens, is the amount of equity Americans have in their homes is now falling as values fall. But what hurts the equation even more is debt remains the same. This is also one of the reasons foreclosures are jumping since many Americans are unable to make ends meet and having no equity, they are unable to sell since they are underwater. How so? Say you bought a $400,000 home in a bubble area with zero down. The home is now worth $300,000. In order for you to sell at the current market price, you would need to put in $100,000 of your own money to move the home. No one economically speaking will do this. So many will ask their lender for a short sale. An amount this large will normally not get approved although many lenders are now wising up to the current economic crisis. However many more are simply not sending in payment anymore and letting the foreclosure process take over.

Total Debt: $49 Trillion

This is a big problem since most would agree we are now in a recession. Certainly many states are. With so much debt, it would seem the only way out is for much of this debt to be written down. This is already occurring. Foreclosures are forcing banks to realize losses. Credit card delinquencies are rising. Auto loans are going into default at record rates. This is also a form of money destruction. And it has to occur. There is no other way. Incomes are stagnant and it would appear that we have a few years before things bottom out. This will be a serious challenge for many of us to confront.

What you are going to see for the next few years is a healthy aversion to debt. Otherwise you are going to drive yourself mad trying to digest these absurd numbers.

haaaaaai

ff een snelle tvp, beursbaby wenst aandacht ik zal der zo eens voorlezen.

ik zal der zo eens voorlezen.

ff een snelle tvp, beursbaby wenst aandacht

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

nog steeds is een van de oorzaken het idee dat schuld gelijk is aan geld. dat is het niet. je kan schuld aangaan op grond van waarde in je bezit. het probleem nu is dat op vele fronten de achterliggende waarde van de schuld veel te laag is t.o.v de schuld. defaulting it iss dan he

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Een andere oorzaak is toch ook dat sommige waardes waarop weer nieuwe schulden verstrekt werden toch niet zo waardevol bleken te zijn. ( o.a. de leuke hypotheek pakketjes)quote:Op dinsdag 27 januari 2009 16:21 schreef simmu het volgende:

nog steeds is een van de oorzaken het idee dat schuld gelijk is aan geld. dat is het niet. je kan schuld aangaan op grond van waarde in je bezit. het probleem nu is dat op vele fronten de achterliggende waarde van de schuld veel te laag is t.o.v de schuld. defaulting it iss dan he

eerder een gevolg dan. en het blijft hetzelfde onderliggende probleem: zodra je in iets gaat handelen heeft het waarde. schuld = waarde = geld. wordt een mooie keten zo.quote:Op dinsdag 27 januari 2009 19:32 schreef Basp1 het volgende:

[..]

Een andere oorzaak is toch ook dat sommige waardes waarop weer nieuwe schulden verstrekt werden toch niet zo waardevol bleken te zijn. ( o.a. de leuke hypotheek pakketjes)

Your mind don't know how you're taking all the shit you see

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

Dont believe anyone but most of all dont believe me

God damn right it's a beautiful day Uh-huh

quote:Bankers' Worst Nightmare Materialize

Amidst soaring chargeoffs and ever increasing job layoff announcement, Bankers' Fear of Unemployment Materialize.

Bankers' worst nightmare is the unemployment rate climbing toward 10%, a level at which credit losses could balloon unpredictably because of high defaults among people with previously strong credit histories.

Bight now, bank balance sheets don't appear in a position to deal with unemployment moving sharply higher from its current 7.2% rate.

Building up bad-loan reserves to deal with a 9% to 10% rate could produce enormous losses and pulverize capital when banks are trying to preserve the thin cushions they have. And fear of rising unemployment could deter lending when the government wants banks to expand credit. True, the Obama administration's stimulus plan could reduce unemployment expectations. But right now, banks are hoisting their joblessness forecasts.

Last week, consumer lender Capital One Financial increased its unemployment forecast to 8.7% by the end of 2009, from its previous expectation of 7% by midyear. And Capital One added that it is building more-severe unemployment scenarios into lending decisions.

Also last week, Kelly King, chief executive of regional bank BB&T, said unemployment of 8% to 8.5% is "kind of manageable," but 9% to 10% would "have a dramatic impact on our scenarios."

Why the trepidation of going above 9%? Take a regular credit-card book. Past data show that a percentage-point increase in unemployment leads to roughly a percentage-point rise in the charge-off rate, the amount of defaulted loans written off at a loss.

But as unemployment exceeds 9%, bankers think charge-offs will start to increase by more than the increase in unemployment. The reason? A high rate could cause an unprecedented wave of defaults among prime borrowers, who tend to have bigger loan balances.

"The situation is so extreme and beyond what we've seen in past cycles that management teams are becoming reluctant to predict the relationship between unemployment and credit losses," said Kevin Fitzsimmons, analyst at Sandler O'Neill & Partners.

Hulde voor het plaatsen van Karl Denninger blogposts!  Ik volg hem nu al een hele tijd en tot nu toe heeft hij het altijd bij het rechte eind gehad, behalve dat hij *iets* te lang positief bleef, hoewel hij daar nu langzaam maar zeker op terug komt.

Ik volg hem nu al een hele tijd en tot nu toe heeft hij het altijd bij het rechte eind gehad, behalve dat hij *iets* te lang positief bleef, hoewel hij daar nu langzaam maar zeker op terug komt.

"One man looks at a dying bird and thinks there's nothing but unanswered pain. That death's got the final word, it's laughing at him. Another man sees that same bird, feels the glory, feels something smiling through it."

Hoe staat het eigenlijk met individuele staten binnen de VS?

Niet zo lang geleden nog gelezen dat er staten waren met gigantische schulden o.a. California.

Niet zo lang geleden nog gelezen dat er staten waren met gigantische schulden o.a. California.

Ceterum censeo Turciam delendam esse.

Ze hebben pas het minimumloon verlaagd.quote:Op donderdag 29 januari 2009 18:07 schreef BlaZ het volgende:

Hoe staat het eigenlijk met individuele staten binnen de VS?

Niet zo lang geleden nog gelezen dat er staten waren met gigantische schulden o.a. California.

Ook zo'n 1929 maatregel

Het verschilt per staat hoe groot de problemen zijn en hoe de regeringen het proberen op te lossen. Zoals het er nu uitziet hebben alleen de staten Alaska, Montana, North Dakota, Wyoming en West Virginia een vrij stabiele staatsbudget. De andere 45 staten zullen zeker tekorten gaan krijgen.quote:Op donderdag 29 januari 2009 18:07 schreef BlaZ het volgende:

Hoe staat het eigenlijk met individuele staten binnen de VS?

Niet zo lang geleden nog gelezen dat er staten waren met gigantische schulden o.a. California.

Hier staat per staat wat het begrote gat is tussen inkomsten en uitgaven: http://www.cbpp.org/9-8-08sfp.htm

Dit is ook een duidelijk plaatje over de problemen per staat

Sommige staten zullen gebruikmaken van hun Rainy Day Fund, waar ze hun centjes hebben opgeslagen voor bare tijden: http://www.cbpp.org/2-21-08sfp2.htm.

Vooral Alaska zit er bijzonder warmpjes bij, alleen California heeft een groter fonds. Met het kleine detail natuurlijk dat in Alaska ongeveer 0,7 miljoen mensen wonen en in California 36,8 miljoen.

Ook Iowa, Nebraska, New Mexico, North Dakota, Oklahoma, South Dakota, West Virginia en Wyoming hebben relatief grote fonds in vergelijking met hun inwonersaantal.

quote:RT Guest February 11, 2009, 4:40 0 Russia Today

Gerald Celente

In 2009 we’re going to see the worst economic collapse ever, the ‘Greatest Depression’, says Gerald Celente, U.S. trend forecaster. He believes it’s going to be very violent in the U.S., including there being a tax revolt.

RT: The fragile U.S. economy has been met with bank bailouts and stimulus plans. So what’s to come in 2009? Joining me now to answer that question is Gerald Celente, founder and director of the Trends Research Institute. Thank you for joining me.

Gerald Celente: My pleasure.

RT: How would you define the economic trend that you have forecasted for 2009?

G.C.: We’re going to see the economic collapse the likes of which the world has never seen before. It’s not only in the United States; it’s going global. At the end of 2008 we saw Christmas retail sales: women’s apparel down 23%; home furnishings and electronics off 27%; luxury items down 35%. These are Depression Era collapses. We saw major bankruptcies, such as retailers Circuit City and Linens and Things. One bankruptcy after another. Then we saw store closings. Starbucks, Home D&D Power and down the line.

The question becomes who is going to take all of the vacant retail space? Who is going to rent it? The answer is - nobody. Now we look at the financial collapse in 2008, we saw the Merrill Lynch mob go under the bed and the Lehman boys went bankrupt. You saw bond companies, brokerage firms, and banks go belly up. Who is going to rent all the vacant commercial business space that they used to occupy? The answer is - nobody. The commercial real estate collapse that’s going to happen in 2009 is going to dwarf the residential real estate collapse.

RT: You use the Great Depression as an analogy, as a comparison. During the Great Depression unemployment was 25%. Now it has increased, it’s I think over 7.2. Is that number going to get much, much bigger?

G.C.: We have to look at the real number. There are two sets of books that the government keeps. When they measure up unemployment they don’t add in the people who are no longer looking for jobs because they have become discouraged since they cannot find employment after looking so long. And they don’t include part-time workers. When you put that number into it, the number is 13.7%. And that’s a government number. And this is just beginning. And again, current events form future trends.

What did we see? We saw in one day some 61,000 jobs evaporate off the map. You’re going to see Great Depression numbers. Because, as I mentioned, with this commercial real estate collapse, all of these retail stores closing, like Starbucks and Macy’s, you go down the line. You look not only at people who work for these places that no longer have jobs, but how about all the supportive industries - the advertising, the manufacturers, the products. They’re going to be laying off people as well. We’re going to see Great Depression numbers. In that effect, this is going to be worse than the Great Depression.

RT: What are we going to see happening to the society, to people’s day-to-day lives in terms of how they treat one another, how they behave, crime?

G.C.: When I say it’s going to be worse than the Great Depression, we call it the Greatest Depression. By the way, to be using 1930s models to get the U.S. out of this is really stupid. Back then when we first crashed most people didn’t have homes. There was no such thing as home equity loan. And back then, people didn’t have credit cards. The consumer wasn’t 14 trillion dollars in debt. We had a manufacturing base that built the world out of the Great Depression following World War Two. We no longer have that.

Now people are at the edge. They’re stressed out. Look, the Americans are the most depressed nation on the world already. They take more antidepressant drugs than anybody, plus the other kinds of drugs that they are taking. You’re going to see crime levels in America that are going to rival the third world. Welcome Mexico City. You’re going to start seeing people being kidnapped in this country like they do in other underdeveloped nations. So it’s going to be very violent in America.

RT: You’re not exaggerating?

G.C.: I’m not exaggerating, the facts are there. I have a saying: when people lose everything and they have nothing to lose, they lose it. You’re going to see people saying, off with their heads. There’s going to be another revolution in this country.

RT: When will this revolution that you have forecasted in your Trends journal happen and what will ignite it?

G.C.: It’s going to be a tax revolt. We’re going to start seeing a tax revolt in the United States. People are one job away from losing everything. We’re seeing more and more closures, people are being laid off. People are stretched to the limits. And what do they do in New York State? Some130 new taxes are being proposed, they’re raising sales taxes. There’s going to be a tax revolt in this country from property taxes first and school taxes second. That’s what we’re going to see start to happen.

RT: Do you feel people are not hopeful that Obama will make a difference?

G.C.: People are hopeful, they are desperate and they are fearful. And they’ll hang on to anything. Let’s look at the facts. A man of change, who did he bring into Washington? You know they say by their deeds you shall know them. Let’s look at his Treasury Secretary, Timothy Geithner, former Robert Rubin from the Clinton administration, the former president of the New York Federal Reserve Bank. Change? How about Larry Summers, the former Clinton Secretary of Treasury? I mean, I’ve been around a long time. I never remember a newly elected president bringing in basically the national security team from the last administration who happen to be from another party.

RT: Do you not think Obama’s different in any way?

G.C.: By their deeds you shall know them! If I bring in a baseball hitter that strikes out every time and I want him to play in the World Series is he going to hit the ball over the fence? They brought in Larry Summers, Timothy Geithner. Look at the crew. Look who they are. They’re strike out artists, every one of them. The only thing that they know how to do is not to get their finger nails dirty.

RT: There was a sentence in your report, the Trends Journal, that really caught my attention. You wrote: ‘On 9/11, those who listened to the authorities and returned to their offices went down with the towers.’ So are you saying that Americans should not be listening to the officials who are saying the Stimulus Plans are going to make everything better? Is that the analogy?

G.C.: Read my lips. No new taxes. I didn’t have sex with that woman, Monica Lewinski.

I smoked but I didn’t inhale. Saddam Hussein has weapons of mass destruction and ties to Al-Qaeda. Why would anybody believe these people?

RT: So what are Americans supposed to do if they’re not supposed to trust their leaders?

G.C.: Personally, I buy gold. And I’ve been talking about gold since the Trends Journal 2001. We peg the bottom and we said it would start going up at 275. Number two, you don’t spend a dime you don’t need to spend.

RT: What would be the good jobs to benefit from in this year?

G.C.: Anything having to do with health. Anything. It’s going to be a growth industry. And fortunately a lot of them are going to pay a lot of money in that field because a lot of that is going to be care for the elderly. And the other thing really is anything having to do with conservation engineers, anything that’s going to prove technologically sound and smart to save money and to make money.

RT: What about geopolitics, what trends are we going to see in terms of the relationships between the United States and the rest of the world?

G.C.: Well the rest of the world is very hopeful, using the word ‘hope’, with the Obama administration. And again, we’re going to have to see what transpires, but so far, and again, by their deeds you shall know them.

Obama, when he first started to run, he was going to be out of Iraq. As soon as he became president he was going to start bringing soldiers home. Now they won’t be out for 16 months and now their reports say they’re going to bring upwards of 40,000 more troops to Afghanistan. He was also talking about preventive strikes in Pakistan. So it really doesn’t look like it’s going to be much of a smoothing of geopolitical relations.

The one factor we’re looking at, at a time that could only be the worst time for it to happen, is what’s going on in the Middle East, in the Israel-Gaza war. Israel, as they said, they were trying to do as the reports have come out, if they attack Iran at any level, it will begin World War Three. Because if this war spreads beyond Gaza, it’s going to inflame the Middle East. It can cause an oil crisis as we saw in 1973, that’s what ended the Arab-Israeli war when they embargoed oil going into the U.S. That’s our major concern. We’re also seeing, and we’re going to wonder, if Obama continues with putting the so-called missile defense shield in Poland and in Czech Republic in Eastern Europe and if they keep pushing more and more into Georgia. If that keeps happening we’re going to see a reignition of the Cold War.

RT: You have been trend casting since 1980, more than two decades. How do you compile your information and why do you believe you’ve been so spot-on most of the time?

G.C.: Current events form future trends. You can see what’s going on. A great scholar said, “In today already walks tomorrow.” So we say current events form future trends. But when people look at the trends, they colour them or shade them with their own ideology, their own beliefs. It’s what they want, what they hope for, what they wish for.

I’m a political atheist. I look at things for the way they are, not the way I want them to be. I don’t colour them or try to change them because of an ideology. The other major factor that we do differently at Trends Research Institute than anywhere else is we look at over 300 different categories on a global basis. So we’re looking at economics, we’re looking at politics, we’re looking at changes in the family, we’re looking at geopolitics. We’re making connections between different fields continually.

RT: How can America get out of the situation?

G.C.: All you have to do is to look back to the 1990s when America entered into a recession. We had 7.2 unemployment rate in 1993. What got the U.S. out of the 1990s recession was something called the ‘internet revolution’ that had a productive capacity. Products were invented, designed, manufactured, marketed and serviced. So you’re asking about new jobs, ask about alternative energies. Anything that’s going to advance the U.S. into the 21st century in an intelligent way. That’s where the job opportunities are going to be.

RT: Gerald Celente, founder of the Trends Research Institute, thank you very much for taking time to speak with us.

Ik wordt nooit vrolijk van dit subforum

1/10 Van de rappers dankt zijn bestaan in Amerika aan de Nederlanders die zijn voorouders met een cruiseschip uit hun hongerige landen ophaalde om te werken op prachtige plantages.

"Oorlog is de overtreffende trap van concurrentie."

"Oorlog is de overtreffende trap van concurrentie."

Als dat echt allemaal uitkomt en doorgaat, kan Nostradamus best eens gelijk hebben met zijn Oost West oorlog rond 2012-2016. De beste manier om een economische crisis te boven te komen is nog altijd een goede oorlog geweest. Lekker wat werklozen weg en na de tijd lekker bouwen.

Rik: Hey guys, wouldn't it be AMAZING if all this money was real?

Vyvyan: Rik, that is the single most predictable and BORING thing anyone could ever say whilst playing Monopoly.

Vyvyan: Rik, that is the single most predictable and BORING thing anyone could ever say whilst playing Monopoly.

quote:We are threatened by veritable disaster

I must confess to having read only a bit of economist Axel Leijonhufvud's writings, but what I have seen, I have liked very much.

Leijonhufvud's current post at VoxEU does a very good job of looking at the economic mess the US is in and assesses policy options. It is a remarkably straightforward piece. Most of the information cited will be familiar to many readers, but he connects them and concludes that stimulus will almost certainly be ineffective unless undertaken on a scale that would produce very serious inflation.

From VoxEU:

This recession is different. Balance sheets of consumers, firms, and banks are under strain. The private sector is bent on reducing debt and this offsets Keynesian stimulus more than standard flow calculations would suggest. Bank deleveraging is by far the most dangerous. Fiscal stimulus will not have much effect as long as the financial system is deleveraging.

This is not an ordinary recession that differs from other recent episodes simply by being somewhat more severe. It differs in kind.

Past recessions and the reallocation of employment

The end of the Cold War brought a decline in military spending and a recession which impinged most heavily on the states, like California, where the military-industrial complex was an important part of the local economy. The nationwide unemployment rate rose from 5.25% in 1989 to 7.5% in 1992. It then fell every year reaching just under 4% in 2000. The “free market” took care of the recession of the early 1990’s. Resources moved from the defence industries, trickling into other uses through innumerable channels. The federal government did not need to take a hand. Beginning in 1993, the federal deficit in fact shrank every year turning into a modest surplus in 1998. That was a very ordinary recession.

If the current situation were at all similar we would expect a recession in residential construction with unemployment among construction workers and mortgage brokers. Naturally, recent boom areas would be hard hit but we would expect resources gradually to trickle into alternative employment. Instead, we are threatened by a veritable disaster.

Balance sheet recessions

What is the difference? It resides in the state of balance sheets. The financial crisis has put much of the banking system on the edge – or beyond -- of insolvency. Large segments of the business sector are saddled with much short-term debt that is difficult or impossible to roll over in the current market. After years of near zero saving, American households are heavily indebted.

The holes that have opened up in the balance sheets of the private sector are very large and still growing. A recent estimate by Jan Hatzius and Andrew Tilton of Goldman Sachs totes up capital losses of $2.1 trillion; Nouriel Roubini thinks the total is likely to be $3 trillion. About half of these losses belong to financial institutions which means that more banks are insolvent – or nearly so – than has been publicly recognised so far.

So the private sector as a whole is bent on reducing debt. Businesses will use depreciation charges and sell off inventories to do so. Households are trying once more to save. Less investment and more saving spell declining incomes. The cash flows supporting the servicing of debts are dwindling. This is a destabilising process but one that works relatively slowly. The efforts by financial firms to deleverage are the more dangerous because they can trigger a rapid avalanche of defaults (Leijonhufvud 2009).

The Japanese example

Richard Koo (2003) coined the term “balance sheet recession” to characterise the endless travail of Japan following the collapse of its real estate and stock market bubbles in 1990. The Japanese government did not act to repair the balance sheets of the private sector following the crash. Instead, it chose a policy of keeping bank rate near zero so as to reduce deposit rates and let the banks earn their way back into solvency. At the same time it supported the real sector by repeated large doses of Keynesian deficit spending. It took a decade and a half for these policies to bring the Japanese economy back to reasonable health.

The Great Depression counterexample

The US Great Depression saw no consistent policy of deficit spending on adequate scale in the 1930’s. War spending not only brought the economy back to full resource utilisation but also crowded out private consumption to a degree (Barro 2009).1 The deficits run during the war meant that:

At war’s end, the federal government’s balance sheet showed a debt of a size never before seen, but also

The balance sheets of the private sector were finally back in good shape.

At the time, a majority of forecasts predicted that the economy would slip back into depression once defence expenditures were terminated and the armed forces demobilised. The forecasts were wrong. This famous postwar “forecasting debacle” demonstrated how simple income-expenditure reasoning, ignoring the state of balance sheets, can lead one completely astray.

Lessons from the two cases: Fill the financial sinkholes first

The lesson to be drawn from these two cases is that deficit spending will be absorbed into the financial sinkholes in private sector balance sheets and will not become effective until those holes have been filled. During the years that national income fails to respond, tax receipts will be lower so that the national debt is likely to end up larger than if the banking sector’s losses had been “nationalised” at the outset.

Sweden’s successful policy mix: Don’t forget the mega devaluation

The Swedish policy following the 1992 crisis has been often referred to in recent months. Sweden acted quickly and decisively to close insolvent banks, and to quarantine their bad assets into a special fund.2 Eventually, all the assets, good and bad, ended up in the private banking sector again. The stockholders in the failed banks lost all their equity while the loss to taxpayers of the bad assets was minimal in the end. The operation was necessary to the recovery but what actually got the economy out of a very sharp and deep recession was the 25-30% devaluation of the krona which produced a long period of strong export-led growth. Needless to say, the US is in no position to emulate this aspect of the Swedish success story.

Yves here. I wouldn't bet on that. In fact, if I were the Fed, I'd very much want a cheaper dollar, but the conundrum is how to achieve that without causing more global instability. Back to the article:

Perils, present and future

Strong contractionary forces are at work in the US emanating both from the capital and the income accounts. Stabilisation requires major policy actions on both fronts.

First, the financial system must be recapitalised so as to remove the relentless pressure to deleverage from the banks

Second, a spending stimulus sufficient to reverse the rapidly worsening decline in incomes must be administered.

When the entire private sector is bent on shortening its balance sheet and paying down debt, the public sector’s balance sheet must move in the opposite, offsetting direction. When the entire private sector is striving to save, the government must dis-save. The political obstacles to doing these things on a sufficient scale are formidable.

If banking system losses are of the magnitude estimated by Goldman Sachs or Roubini, the banks need capital injections of at least another $200-300 billion. Even if injections equal to all their losses could be effected, the banks might still want to contract, now that they know how dangerous their leverage of yesteryear was.

US policy: A strangely contrived way out of a political impasse

The American public understands clearly that the present disaster was fashioned on Wall Street (albeit with some stimulus from Fed policy). Outright bail-outs are a “hard sell” therefore. But the American ideological taboo against “nationalisation” also stands in the way of dealing with the matter in the straightforward way that Sweden did. The present administration, like the last, would like to recapitalise the banks at least partly by attracting private capital. That can hardly be accomplished as long as the value of large chunks of the banks’ assets remains anybody’s guess. Government guarantees against (some part of) losses that may be incurred might solve this problem. But it would be a strangely contrived way out of a political impasse.

Fiscal stimulus + financial deleveraging = zero impact

Fiscal stimulus will not have much effect as long as the financial system is deleveraging. Even if that problem were to be more or less solved, the government deficit would have to offset both the decline in industry investment and the rise in household saving – a gap that is rising as the recession deepens. Here, too, the public is sceptical and prone to conclude that a program that only slows or stops the decline but fails to “jump start” the economy must have been a waste of tax payers’ money. The most effective composition of such a program is also a problem.

US states and local governments undoing the federal spending boost

Almost all American states now suffer under self-imposed constitutional balanced budget requirements and are consequently acting as powerful amplifiers of recession with respect to both income and employment. The states will have a spending propensity of one, as will a great many local governments. Income maintenance for unemployed and other low income households will also be effective.3 Tax cuts will have considerably lower spending propensities. However, the political prospects seem to portend a less than ideal program mix.

The danger of deflation, or inflation

If government programs end up not being large enough to turn the recession around, we have to look forward to a deflationary period of indeterminate length. If they do succeed, however, severe inflationary pressures may surface quite quickly.

The US ratio of federal debt to GNP is not particularly high at this time. But it does not take into account the very large off-balance liabilities of entitlement programs. Since the present crisis began, moreover, the Federal Reserve System and other federal agencies have made bail-out, loan and credit guarantee commitments totalling many trillions of dollars with uncertain eventual implications for the consolidated federal balance sheet.

If the US’s foreign creditors balk, inflation will be hard to contain

Much will depend on the willingness of the nation’s foreign creditors to continue to accumulate or at least to hold dollars at low rates of interest. Should this willingness falter, inflation will be hard to contain.

There is much to fear beyond fear itself.

quote:Op vrijdag 13 februari 2009 16:03 schreef icecreamfarmer_NL het volgende:

Ik wordt nooit vrolijk van dit subforum

Simmu beschreef het al goed een aantal weken terug.

Ach laat maar klappen, alles wat we destijds hebben geschreven in de BBB-reeks komt nu uit.

Laten we het maar over economische definities hebben om er een zinvolle draai aan te geven. Wordt het nu deflatie of inflatie.... bovenstaand artikel is daar ook niet helemaal stipt in.

Wat we nu zien zijn deflationistische verschijnselen. Maar of dat zo blijft ?!? Ik twijfel ernstig omdat deze downswing ook ernstige gevolgen als de economie weer zijn weg omhoog gaat vinden.

Gebeurt er nix = Deflatie.

Gebeurt er wel iets = 2 strijd tussen deflatie en inflatie.

[ Bericht 22% gewijzigd door Drugshond op 15-02-2009 09:15:34 ]

Voorlopig is het deflatie, zeker in de landen aan de oostkant van Europa is het pure deflatie boven de 10% tot en met forse loonsverlagingen.quote:Op zondag 15 februari 2009 09:10 schreef Drugshond het volgende:

[..]

Simmu beschreef het al goed een aantal weken terug.

Ach laat maar klappen, alles wat we destijds hebben geschreven in de BBB-reeks komt nu uit.

Laten we het maar over economische definities hebben om er een zinvolle draai aan te geven. Wordt het nu deflatie of inflatie.... bovenstaand artikel is daar ook niet helemaal stipt in.

Wat we nu zien zijn deflationistische verschijnselen. Maar of dat zo blijft ?!? Ik twijfel ernstig omdat deze downswing ook ernstige gevolgen als de economie weer zijn weg omhoog gaat vinden.

Gebeurt er nix = Deflatie.

Gebeurt er wel iets = 2 strijd tussen deflatie en inflatie.

quote:Treasurys Are 'Disaster Waiting to Happen': Dr. Doom

>> Check het filmpje op bovengenoemde link <<

The Federal Reserve has no option but to start buying Treasurys as the government's needs for financing are huge, but the government bond market is a disaster in the making, Marc Faber, editor and publisher of The Gloom, Boom & Doom Report, told CNBC.

Current DateTime: 01:05:45 18 Mar 2009

Federal Reserve policymakers start a two-day meeting on Tuesday, weighing options on how to spur lending to help cash-strapped consumers kickstart the economy.

Economists expect them to leave rates at zero and look to other ways of boosting liquidity, such as buying government bonds – a measure which has already been taken by the Bank of England.

"Well I think other central banks have done it already around the world but basically what it amounts to is money printing and in fact I don't think that it will help the bond market at all in the long run," Faber told CNBC's Martin Soong.

The yield on the 30-year Treasurys touched a low of 2.51 percent last year in December but now it is back up at 3.77 percent, he said.

"Yields have already backed up pretty substantially and I tell you, I think the US government bond market is a disaster waiting to happen for the simple reason that the requirements of the government to cover its fiscal deficit will be very, very high," Faber said.

"I think we may still have a rally (in the S&P) until about the end of April and probably then a total collapse in the second half of the year sometimes, when it becomes clear that the economy is a total disaster," Faber said.

|

|