WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

2 Onafhankelijke gegevens stromen die hetzelfde willen zeggen.

Lange posting maar geeft wel het spanningsveld aan in onze Eurozone.

Italy The Achilles Heel of Europe

It is ironic and only fitting that Italy is shaped like a boot. Italy is loved and often the travel destination by many Americans and for good reason, it is downright charming. Way back in 2011 Nouriel Roubini warned that Italy needed to pursue an orderly restructuring of it's debt to avert a default in coming years. At the time he saw the ECB and Berlin could impose a depression on Rome if things were to continue as they were. Almost everyone agrees that Italy’s public debt is unsustainable and needs an orderly restructuring to avert a default, but as usual in the Euro-zone no action is happening. In many ways Italy could be viewed as the Achilles heel of Europe.

Italy A European Debt Bomb Waiting To Explode

Italy is the third largest economy of the Euro-zone after Germany and France, unfortunately it holds the largest public debt totaling over 2 trillion euro. This debt has been growing at an astonishing pace, even in more recent times and particularly as a ratio to GDP. The fact that the GDP is contracting has exacerbated the problem. This is not sustainable and the country is held together only because of the direct intervention of the ECB which made over 102 billion euro of Italian bond purchases in 2011-2012 alone. This has continued since then and the sum has gotten much larger. Only through the LTRO can the finances of the Italian state be kept afloat.

The truth is that in all reality Italy went bankrupt in summer 2011. Back then we saw interest rates on the national debt spike going out of control and Italy lost access to the financial markets. At that time the ECB and political authorities in Europe agreed to create around the country’s finances an artificial market to give the impression of stability and the appearance that Italy could work its way through its problems. Italy it appears is now forced to stay on this artificial support until the economic conditions improve and confidence is restored to where the country will have again access to real and normal credit markets. This most likely will never happen because not only is the country mired in debt it is also a mess politically.

Because of the sheer dimensions of Italy as an economy and as a debtor it dwarfs the problems posed by the PIGS that had received so much attention. We must remember to put this in proper prospective, all countries are not equal in size and the reason for their woes will vary. However, propping up an economy is not a long term fix and the ECB loaning money to banks to have them purchase government-issued bonds is a scheme and instrument that allows international investors to do an orderly withdrawal from Italy. The French and German's, whose share of this public debt is falling reflects the rise of Italian banks purchasing public debt.

We should not let this important signal go unnoticed, it goes in the opposite direction of an increased interdependency which would be expected from a monetary union preparing for a political union. It seems that many investors are actually systematically reducing their exposure in South Europe, possibly hoping that a future breakup of the common currency will have less harmful consequences if their involvement in the financial and economy destiny of those countries has been reduced and curtailed to the minimum. For Euro-sceptics, it is a signal that, once foreign investors withdraw, Italy will crumbly under the weight of its debt.

=====================================================================================

Miracle Not Enough to Save Italy; Disruptive Eurozone Breakup Awaits

Analysis of what's happening and what to do about problems are two different things.

Financial Times writer Wolfgang Münchau provides an excellent example in Italy Debt Burden is a Problem For Us All.

Münchau's opening gambit is "We need extreme and co-ordinated policy to make it possible for Italy to ultimately stay in the eurozone."

Münchau states, "I think it is high time to address the consequences of failure with more clarity than is usually done. Put bluntly, Italy’s economic position is unsustainable and will result in eventual debt default unless there is a sudden and durable change in economic growth. At that point, Italy’s future in the eurozone would also be in doubt – and indeed the future of the euro itself."

High Time For Honest Assessment

Actually, it is indeed "high time" for something. What we need is an honest assessment from political leaders and euro puppets that the euro is doomed.

The flaws of the euro are well understood. I am 100% certain that Münchau could write a playbook on them with ease.

Münchau even admits that it would be "naive" to believe economic reforms can save Italy.

"The economic adjustment needed goes much beyond a few structural reforms. Italy needs changes in the legal system, it needs to bring taxes down to the eurozone average, and to improve the quality and efficiency of the public sector. It needs, in other words, to change the entire political system. Even that may not be enough."

According to Münchau (and I wholeheartedly agree), Italy needs economic reform, a new legal system, lower taxes, less government spending, pension reform, and more productivity. And even that might not be enough!

Nonetheless, to support his political beliefs, he seeks a miracle.

Miracle Requested

"I could see the ECB buying a wide range of debt instruments, starting with asset-backed securities and covered bonds as already announced. On top of that, it could buy other types of financial securities – bonds from the European Stability Mechanism, the eurozone’s rescue umbrella, and from the European Investment Bank. The Commission could use the EIB to launch a big programme of infrastructure bonds. The best hope for Italy is that some of that trickles down into the real economy. I am optimistic that these programmes will have a noticeable positive effect on the eurozone as a whole, but much less certain of their effect on Italy."

Miracle Might Not Be Enough!

Münchau asks for that set of miracles from the ECB, yet is "less certain of their effect on Italy". Why? because "radical reform is not enough".

Note the irony in Münchau's conclusion "Italian debt sustainability requires policies at eurozone level that have so far been ruled out. This is where the eurozone’s success or failure will be decided."

Eurozone Already Failed

Spain's unemployment rate is close to 25%. Its growth and unemployment prospects are nil.

Spain has no chance of meeting budget targets. Nor do France and Italy. Greece and Cyprus are in depressions. France is waiting on deck with problems as big as Italy's.

Any thinking person with an ounce of common sense he would readily admit the eurozone has already failed and it cannot and will not be revived by wishful thinking.

Miracles are not coming. However, there are choices, all of them unpalatable, to the eurozone nannycrat.

Eurozone Choices

1. Voluntarily dismantle the eurozone in the least destructive manner

2. Dismantle the eurozone by populist choice with huge financial disruptions

3. Suffer through decades of stagnant growth and extremely high unemployment

Option 4, pray for a miracle is not a logical choice.

Unless done voluntarily, it's easy to predict what will eventually happen: After suffering long enough in option 3, a populist office-seeker will stand before the voters, hold up a copy of the EU treaty and declare all the bailouts and debt foisted on their country to be null and void. That person will be elected.

What to Do About It

No miracle can keep the eurozone project intact. If Münchau was honest with himself, he would admit it.

The only thing that makes any sense to do is dismantle the eurozone, by choice, before someone like Marine Le Pen in France, Beppe Grillo in Italy, or an unknown person in Spain or elsewhere does it by force.

Disruptive Eurozone Breakup Awaits

Instead of seeking miracles that won't work and are not coming in the first place, how about an honest dialog on the best way to break up the eurozone?

Unfortunately, that will not happen because it is politically unacceptable. A disruptive breakup of the eurozone awaits.

Addendum

Reader Marian states "If indeed Italy's problems are it's legal system, tax rates, quality and efficiency of the public sector, then simply dissolving the EU, even in an orderly way, would not address these fundamental issues."

Marian is of course correct! But why should the rest of Europe have to suffer with bailing out Italy when that approach cannot possibly fix the problem?

Can-kicking exercises only make the problem worse for all involved. By dissolving the eurozone, countries would be forced to address the real issues instead of praying for miracles from the ECB.

================================================================================

ff natte vingerwerk. De schuld van Italie en Frankrijk is nagenoeg gelijk (2 Triljoen). Alleen Frankrijk is 2e economische motor van Europa en Italie derde. Dus relatief gezien staat Italie er een stuk beroerder slechter voor.

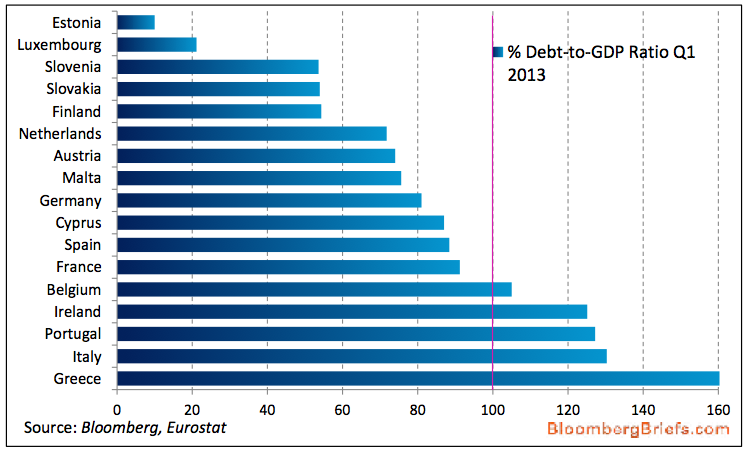

Schuld versus GDP.

Groei van het GDP

En voor een stabiel Europa zou elk land zo rond de 60 % moeten zitten. Er is maar 1 land wat het nog slechter doet dan Italië en dat is Griekenland.

Creditrating Italy : Baa2 (Stable).

Het gaat al niet goed met hun schuldenberg, en hun indicatoren wijzen naar negatief.

Moeten we straks de schuld opkopen van Italië (M.Dragi gaat alvast al wel die kant op bewegen, maar of Duitsland hierin blijft volgen is nog maar zeer de vraag). Dat land is echt way-way too big to fail om de eurozone nog instant te kunnen houden.

[ Bericht 0% gewijzigd door Drugshond op 01-10-2014 15:09:52 ]

Lange posting maar geeft wel het spanningsveld aan in onze Eurozone.

Italy The Achilles Heel of Europe

It is ironic and only fitting that Italy is shaped like a boot. Italy is loved and often the travel destination by many Americans and for good reason, it is downright charming. Way back in 2011 Nouriel Roubini warned that Italy needed to pursue an orderly restructuring of it's debt to avert a default in coming years. At the time he saw the ECB and Berlin could impose a depression on Rome if things were to continue as they were. Almost everyone agrees that Italy’s public debt is unsustainable and needs an orderly restructuring to avert a default, but as usual in the Euro-zone no action is happening. In many ways Italy could be viewed as the Achilles heel of Europe.

Italy A European Debt Bomb Waiting To Explode

Italy is the third largest economy of the Euro-zone after Germany and France, unfortunately it holds the largest public debt totaling over 2 trillion euro. This debt has been growing at an astonishing pace, even in more recent times and particularly as a ratio to GDP. The fact that the GDP is contracting has exacerbated the problem. This is not sustainable and the country is held together only because of the direct intervention of the ECB which made over 102 billion euro of Italian bond purchases in 2011-2012 alone. This has continued since then and the sum has gotten much larger. Only through the LTRO can the finances of the Italian state be kept afloat.

The truth is that in all reality Italy went bankrupt in summer 2011. Back then we saw interest rates on the national debt spike going out of control and Italy lost access to the financial markets. At that time the ECB and political authorities in Europe agreed to create around the country’s finances an artificial market to give the impression of stability and the appearance that Italy could work its way through its problems. Italy it appears is now forced to stay on this artificial support until the economic conditions improve and confidence is restored to where the country will have again access to real and normal credit markets. This most likely will never happen because not only is the country mired in debt it is also a mess politically.

Because of the sheer dimensions of Italy as an economy and as a debtor it dwarfs the problems posed by the PIGS that had received so much attention. We must remember to put this in proper prospective, all countries are not equal in size and the reason for their woes will vary. However, propping up an economy is not a long term fix and the ECB loaning money to banks to have them purchase government-issued bonds is a scheme and instrument that allows international investors to do an orderly withdrawal from Italy. The French and German's, whose share of this public debt is falling reflects the rise of Italian banks purchasing public debt.

We should not let this important signal go unnoticed, it goes in the opposite direction of an increased interdependency which would be expected from a monetary union preparing for a political union. It seems that many investors are actually systematically reducing their exposure in South Europe, possibly hoping that a future breakup of the common currency will have less harmful consequences if their involvement in the financial and economy destiny of those countries has been reduced and curtailed to the minimum. For Euro-sceptics, it is a signal that, once foreign investors withdraw, Italy will crumbly under the weight of its debt.

=====================================================================================

Miracle Not Enough to Save Italy; Disruptive Eurozone Breakup Awaits

Analysis of what's happening and what to do about problems are two different things.

Financial Times writer Wolfgang Münchau provides an excellent example in Italy Debt Burden is a Problem For Us All.

Münchau's opening gambit is "We need extreme and co-ordinated policy to make it possible for Italy to ultimately stay in the eurozone."

Münchau states, "I think it is high time to address the consequences of failure with more clarity than is usually done. Put bluntly, Italy’s economic position is unsustainable and will result in eventual debt default unless there is a sudden and durable change in economic growth. At that point, Italy’s future in the eurozone would also be in doubt – and indeed the future of the euro itself."

High Time For Honest Assessment

Actually, it is indeed "high time" for something. What we need is an honest assessment from political leaders and euro puppets that the euro is doomed.

The flaws of the euro are well understood. I am 100% certain that Münchau could write a playbook on them with ease.

Münchau even admits that it would be "naive" to believe economic reforms can save Italy.

"The economic adjustment needed goes much beyond a few structural reforms. Italy needs changes in the legal system, it needs to bring taxes down to the eurozone average, and to improve the quality and efficiency of the public sector. It needs, in other words, to change the entire political system. Even that may not be enough."

According to Münchau (and I wholeheartedly agree), Italy needs economic reform, a new legal system, lower taxes, less government spending, pension reform, and more productivity. And even that might not be enough!

Nonetheless, to support his political beliefs, he seeks a miracle.

Miracle Requested

"I could see the ECB buying a wide range of debt instruments, starting with asset-backed securities and covered bonds as already announced. On top of that, it could buy other types of financial securities – bonds from the European Stability Mechanism, the eurozone’s rescue umbrella, and from the European Investment Bank. The Commission could use the EIB to launch a big programme of infrastructure bonds. The best hope for Italy is that some of that trickles down into the real economy. I am optimistic that these programmes will have a noticeable positive effect on the eurozone as a whole, but much less certain of their effect on Italy."

Miracle Might Not Be Enough!

Münchau asks for that set of miracles from the ECB, yet is "less certain of their effect on Italy". Why? because "radical reform is not enough".

Note the irony in Münchau's conclusion "Italian debt sustainability requires policies at eurozone level that have so far been ruled out. This is where the eurozone’s success or failure will be decided."

Eurozone Already Failed

Spain's unemployment rate is close to 25%. Its growth and unemployment prospects are nil.

Spain has no chance of meeting budget targets. Nor do France and Italy. Greece and Cyprus are in depressions. France is waiting on deck with problems as big as Italy's.

Any thinking person with an ounce of common sense he would readily admit the eurozone has already failed and it cannot and will not be revived by wishful thinking.

Miracles are not coming. However, there are choices, all of them unpalatable, to the eurozone nannycrat.

Eurozone Choices

1. Voluntarily dismantle the eurozone in the least destructive manner

2. Dismantle the eurozone by populist choice with huge financial disruptions

3. Suffer through decades of stagnant growth and extremely high unemployment

Option 4, pray for a miracle is not a logical choice.

Unless done voluntarily, it's easy to predict what will eventually happen: After suffering long enough in option 3, a populist office-seeker will stand before the voters, hold up a copy of the EU treaty and declare all the bailouts and debt foisted on their country to be null and void. That person will be elected.

What to Do About It

No miracle can keep the eurozone project intact. If Münchau was honest with himself, he would admit it.

The only thing that makes any sense to do is dismantle the eurozone, by choice, before someone like Marine Le Pen in France, Beppe Grillo in Italy, or an unknown person in Spain or elsewhere does it by force.

Disruptive Eurozone Breakup Awaits

Instead of seeking miracles that won't work and are not coming in the first place, how about an honest dialog on the best way to break up the eurozone?

Unfortunately, that will not happen because it is politically unacceptable. A disruptive breakup of the eurozone awaits.

Addendum

Reader Marian states "If indeed Italy's problems are it's legal system, tax rates, quality and efficiency of the public sector, then simply dissolving the EU, even in an orderly way, would not address these fundamental issues."

Marian is of course correct! But why should the rest of Europe have to suffer with bailing out Italy when that approach cannot possibly fix the problem?

Can-kicking exercises only make the problem worse for all involved. By dissolving the eurozone, countries would be forced to address the real issues instead of praying for miracles from the ECB.

================================================================================

ff natte vingerwerk. De schuld van Italie en Frankrijk is nagenoeg gelijk (2 Triljoen). Alleen Frankrijk is 2e economische motor van Europa en Italie derde. Dus relatief gezien staat Italie er een stuk beroerder slechter voor.

Schuld versus GDP.

Groei van het GDP

En voor een stabiel Europa zou elk land zo rond de 60 % moeten zitten. Er is maar 1 land wat het nog slechter doet dan Italië en dat is Griekenland.

Creditrating Italy : Baa2 (Stable).

Het gaat al niet goed met hun schuldenberg, en hun indicatoren wijzen naar negatief.

Moeten we straks de schuld opkopen van Italië (M.Dragi gaat alvast al wel die kant op bewegen, maar of Duitsland hierin blijft volgen is nog maar zeer de vraag). Dat land is echt way-way too big to fail om de eurozone nog instant te kunnen houden.

[ Bericht 0% gewijzigd door Drugshond op 01-10-2014 15:09:52 ]

Dus men zal het niet toestaan dat Italië kapot-gespeculeerd wordt.quote:Op woensdag 1 oktober 2014 13:38 schreef Drugshond het volgende:Moeten we straks de schuld opkopen van Italië (M.Dragi gaat alvast al wel die kant op bewegen, maar of Duitsland hierin blijft volgen is nog maar zeer de vraag). Dat land is echt way-way too big to fail om de eurozone nog instant te kunnen houden.

Dat is goed geld tegen slecht geld smijten.quote:Op woensdag 1 oktober 2014 13:55 schreef 99.999 het volgende:

[..]

Dus men zal het niet toestaan dat Italië kapot-gespeculeerd wordt.

Mogelijk, of door een harde opstelling voorkomen dat er met dat geld gesmeten moet worden.quote:

[..]

Dat is goed geld tegen slecht geld smijten.

Tja dat hebben we al gezien in Griekenland. Uiteindelijk heeft de ECB als zowel het IMF de reddende engel moeten spelen. En daar betalen we via een omweg aan mee.quote:

[..]

Mogelijk, of door een harde opstelling voorkomen dat er met dat geld gesmeten moet worden.

Nee, dat hebben gezien toen Draghi aankondigde al het nodige te zullen doen om de Euro te redden. In de praktijk hoefde daarvoor niet veel te gebeuren want de markten slikten het.quote:

[..]

Tja dat hebben we al gezien in Griekenland. Uiteindelijk heeft de ECB als zowel het IMF de reddende engel moeten spelen. En daar betalen we via een omweg aan mee.

Betalen=we lenen geld uit?quote:

[..]

Tja dat hebben we al gezien in Griekenland. Uiteindelijk heeft de ECB als zowel het IMF de reddende engel moeten spelen. En daar betalen we via een omweg aan mee.

The fate of our times is characterized by rationalization and intellectualization and, above all, by the disenchantment of the world.

Geleend geld dat weer terug moet vloeien. De terug betalingstermijn is al opgerekt.quote:

En verder is het risico van afstempelen torenhoog.

Dat laatste lijkt vooralsnog allemaal wel mee te vallen, maar mocht dat alsnog gebeuren; de kosten van andere scenario's zijn in ieder geval hoger.quote:

[..]

Geleend geld dat weer terug moet vloeien. De terug betalingstermijn is al opgerekt.

En verder is het risico van afstempelen torenhoog.

The fate of our times is characterized by rationalization and intellectualization and, above all, by the disenchantment of the world.

Schuld blijft schuld zeker als je het niet of nauwelijks weg kunt inflateren. En de bijbehorende economie het laat afweten. Dus wezenlijke vraag is eigenlijk wie staat er uiteindelijk borg voor.quote:

[..]

Dat laatste lijkt vooralsnog allemaal wel mee te vallen, maar mocht dat alsnog gebeuren; de kosten van andere scenario's zijn in ieder geval hoger.

Als er weinig of geen inflatie is en de economie is wel redelijk stabiel dan is het probleem ook te overzien. Zeker gezien de efficiencyslag die men nog wel kan maken in Italië.quote:

[..]

Schuld blijft schuld zeker als je het niet of nauwelijks weg kunt inflateren. En de bijbehorende economie het laat afweten. Dus wezenlijke vraag is eigenlijk wie staat er uiteindelijk borg voor.

The solution to Italy’s woes is quite simple – leave the euro

Unless something big starts to change soon, Italy is on course for the mother and father of a sovereign default

If the eurozone implodes, Britain will go with it

"What Italy needs most immediately is decent economic growth"

By Roger Bootle

21 Sep 2014

No country epitomises the European economic malaise better than Italy. People often say that Italy cannot get into trouble because it is so rich. It is. Rich in natural beauty and historical treasures, with wonderful cities and beautiful countryside, lovely people, marvellous food and wine and an attractive way of life. But as a country it doesn’t really work.

Some aspects of the problem have been there for ages; some are comparatively new. Before the war, much of Italy was poor. During the 1950s and 1960s, although Italian politics were chaotic and government was dysfunctional, as it industrialised the economy grew very fast and it climbed up the GDP leagues. In 1979, in respect of measured GDP, Italy even overtook the UK, an event that the Italians rejoiced in, calling it Il Sorpasso.

The underlying problems were disguised. Although there was a tendency for inflation to be high, relief was always close at hand in the shape of a weaker lira. And the economy kept growing. But then it all started to go wrong. The UK overtook Italy again in 1995 and the gap between the two economies has been widening ever since.

To get the problem in perspective, all G7 countries except Italy and Japan have now exceeded the level of GDP they enjoyed before the Great Recession. Canada is 9pc above the 2008 level, while Italian GDP is still 9pc below. What’s more, the economy is contracting.

This is not a bolt from the blue. Since the euro was formed in 1999 the annual average growth rate of the Italian economy has been only 0.3pc – in other words, next to nothing.

Mind you, not all of this is due to the euro. There is a desperate need for reform yet the political system seems incapable of delivering what is needed. And Italy has been one of the prime sufferers from the rise of the emerging markets.

Whereas Germany produces high-spec, large consumer durables and machinery, Italy has been specialised in precisely the low-to mid-spec consumer goods which China and others have come to produce more cheaply.

The euro has certainly not helped because, from the start, Italian costs continued to rise faster than they did in Germany and other core countries. This time, though, there was no let out from the exchange rate. So Italian costs and prices were left high and dry.

True, the inflation rate has come down sharply. Indeed, it is now slightly negative. This is hardly surprising given that the unemployment rate is running at 12.6pc. Unlike some of the other peripheral members of the euro, however, Italy has not done much to reduce the competitiveness gap. With so much spare capacity, it is possible that pay and other costs will start to fall markedly, as they have in Spain, Greece and Ireland. But if this happens, although it will eventually make Italian products more competitive, it will also worsen Italy’s other big problem – debt.

Although at 3pc, the government’s deficit is not particularly high, the real financial problem lies with the stock of debt, built up through a long run of deficits. Strikingly, during the recent period of “austerity”, the debt ratio has been rising. It now stands at about 130pc of GDP. If the economy stagnates and prices drop, then nominal GDP will fall. That would cause the ratio of debt to GDP to rise even if the budget were in balance so that the amount of debt had stopped rising.

Italy is very close to the situation that economists call a “debt trap”, that is to say when the debt ratio rises exponentially. From this the only escape is through inflation or default. Italy cannot itself inflate while it has no separate currency. So, unless something big starts to change pretty soon, Italy is on course for the mother and father of a sovereign default.

You frequently hear the view that a government debt crisis in Italy is impossible because the Italians have such a high personal savings rate and, accordingly, there are always the funds to buy the debt. Equally, it is often argued that, unlike Portugal or Greece, the Italian external position is not too bad, with liabilities to foreigners only larger than external assets to the tune of about 30pc of GDP. This means that Italian debt is mostly owed to Italians.

This is largely true – so far as it goes. Admittedly, because Italy is not a big external debtor there is limited risk of a crisis of international indebtedness of the sort that periodically afflicts various emerging markets. But there can still be a fiscal crisis. Just because Italians have large savings does not mean that they will willingly pour money into government bonds, particularly when the unsustainability of the public finances implies that at some stage there will be a default.

As we have seen, Greek debt can be “restructured” without shaking the financial system. This is because Greece is small. But Italy is decidedly not. The Italian government bond market is the third largest in the world, after the US and Japan. Someone somewhere is sitting on some huge stocks of Italian debt – mostly Italian banks. So a debt crisis would morph into a banking crisis.

Not that you’d think there was a problem if you looked at market interest rates. The markets are happy to lend to the Italian government for 10 years at 2.4pc, only 1.3pc above the German equivalent. Mind you, before a crisis hits this is exactly what markets are typically like. Their speciality is to shift from insouciance to panic in a jiffy.

How could Italy escape from all this? The deep-seated problems will not improve overnight. The country needs fundamental reform of its political system, its courts, its tax system and its labour laws. Even if all this were achieved, though, Italy would still be mired in public debt.

Like the rest of the eurozone, what Italy needs most immediately is decent economic growth. Perhaps some Europe-wide upturn will be achieved through a combination of ECB boldness and German fiscal relaxation. But I wouldn’t bank on it.

The radical option is for Italy to leave the euro and allow a weak currency to generate an export boom, higher inflation, more taxes and an easier debt burden. I wonder how many more wasted years Italy can stand until it finally dawns on its leaders that this is the only way forward.

Unless something big starts to change soon, Italy is on course for the mother and father of a sovereign default

If the eurozone implodes, Britain will go with it

"What Italy needs most immediately is decent economic growth"

By Roger Bootle

21 Sep 2014

No country epitomises the European economic malaise better than Italy. People often say that Italy cannot get into trouble because it is so rich. It is. Rich in natural beauty and historical treasures, with wonderful cities and beautiful countryside, lovely people, marvellous food and wine and an attractive way of life. But as a country it doesn’t really work.

Some aspects of the problem have been there for ages; some are comparatively new. Before the war, much of Italy was poor. During the 1950s and 1960s, although Italian politics were chaotic and government was dysfunctional, as it industrialised the economy grew very fast and it climbed up the GDP leagues. In 1979, in respect of measured GDP, Italy even overtook the UK, an event that the Italians rejoiced in, calling it Il Sorpasso.

The underlying problems were disguised. Although there was a tendency for inflation to be high, relief was always close at hand in the shape of a weaker lira. And the economy kept growing. But then it all started to go wrong. The UK overtook Italy again in 1995 and the gap between the two economies has been widening ever since.

To get the problem in perspective, all G7 countries except Italy and Japan have now exceeded the level of GDP they enjoyed before the Great Recession. Canada is 9pc above the 2008 level, while Italian GDP is still 9pc below. What’s more, the economy is contracting.

This is not a bolt from the blue. Since the euro was formed in 1999 the annual average growth rate of the Italian economy has been only 0.3pc – in other words, next to nothing.

Mind you, not all of this is due to the euro. There is a desperate need for reform yet the political system seems incapable of delivering what is needed. And Italy has been one of the prime sufferers from the rise of the emerging markets.

Whereas Germany produces high-spec, large consumer durables and machinery, Italy has been specialised in precisely the low-to mid-spec consumer goods which China and others have come to produce more cheaply.

The euro has certainly not helped because, from the start, Italian costs continued to rise faster than they did in Germany and other core countries. This time, though, there was no let out from the exchange rate. So Italian costs and prices were left high and dry.

True, the inflation rate has come down sharply. Indeed, it is now slightly negative. This is hardly surprising given that the unemployment rate is running at 12.6pc. Unlike some of the other peripheral members of the euro, however, Italy has not done much to reduce the competitiveness gap. With so much spare capacity, it is possible that pay and other costs will start to fall markedly, as they have in Spain, Greece and Ireland. But if this happens, although it will eventually make Italian products more competitive, it will also worsen Italy’s other big problem – debt.

Although at 3pc, the government’s deficit is not particularly high, the real financial problem lies with the stock of debt, built up through a long run of deficits. Strikingly, during the recent period of “austerity”, the debt ratio has been rising. It now stands at about 130pc of GDP. If the economy stagnates and prices drop, then nominal GDP will fall. That would cause the ratio of debt to GDP to rise even if the budget were in balance so that the amount of debt had stopped rising.

Italy is very close to the situation that economists call a “debt trap”, that is to say when the debt ratio rises exponentially. From this the only escape is through inflation or default. Italy cannot itself inflate while it has no separate currency. So, unless something big starts to change pretty soon, Italy is on course for the mother and father of a sovereign default.

You frequently hear the view that a government debt crisis in Italy is impossible because the Italians have such a high personal savings rate and, accordingly, there are always the funds to buy the debt. Equally, it is often argued that, unlike Portugal or Greece, the Italian external position is not too bad, with liabilities to foreigners only larger than external assets to the tune of about 30pc of GDP. This means that Italian debt is mostly owed to Italians.

This is largely true – so far as it goes. Admittedly, because Italy is not a big external debtor there is limited risk of a crisis of international indebtedness of the sort that periodically afflicts various emerging markets. But there can still be a fiscal crisis. Just because Italians have large savings does not mean that they will willingly pour money into government bonds, particularly when the unsustainability of the public finances implies that at some stage there will be a default.

As we have seen, Greek debt can be “restructured” without shaking the financial system. This is because Greece is small. But Italy is decidedly not. The Italian government bond market is the third largest in the world, after the US and Japan. Someone somewhere is sitting on some huge stocks of Italian debt – mostly Italian banks. So a debt crisis would morph into a banking crisis.

Not that you’d think there was a problem if you looked at market interest rates. The markets are happy to lend to the Italian government for 10 years at 2.4pc, only 1.3pc above the German equivalent. Mind you, before a crisis hits this is exactly what markets are typically like. Their speciality is to shift from insouciance to panic in a jiffy.

How could Italy escape from all this? The deep-seated problems will not improve overnight. The country needs fundamental reform of its political system, its courts, its tax system and its labour laws. Even if all this were achieved, though, Italy would still be mired in public debt.

Like the rest of the eurozone, what Italy needs most immediately is decent economic growth. Perhaps some Europe-wide upturn will be achieved through a combination of ECB boldness and German fiscal relaxation. But I wouldn’t bank on it.

The radical option is for Italy to leave the euro and allow a weak currency to generate an export boom, higher inflation, more taxes and an easier debt burden. I wonder how many more wasted years Italy can stand until it finally dawns on its leaders that this is the only way forward.

Dat zijn vele politieke wetten en hervormingen die er (nog) niet snel zullen komen. Het probleem is hier de niet innoverende overheid.quote:

[..]

Als er weinig of geen inflatie is en de economie is wel redelijk stabiel dan is het probleem ook te overzien. Zeker gezien de efficiencyslag die men nog wel kan maken in Italië.

Als ze maar komen. Het hoeft ook niet van vandaag op morgen. Italië stort ook dit jaar niet in hoor.quote:

[..]

Dat zijn vele politieke wetten en hervormingen die er (nog) niet snel zullen komen. Het probleem is hier de niet innoverende overheid.

Viel me wel op dat er opeens allerlei berichten naar buiten komen zo in September dat er voor Italië snel iets moet gaan gebeuren. De trigger is no doubt neerwaartse GDP bijstelling = alweer negatief. En ze zitten nu ook al in de deflationaire zone (voor het eerst sinds 1959).quote:

[..]

Als ze maar komen. Het hoeft ook niet van vandaag op morgen. Italië stort ook dit jaar niet in hoor.

-----------------------------------------------------------------------------

Only a monetary 'nuclear bomb' can save Italy now, says Mediobanca

The OECD has drastically cut its growth forecast for Italy. The depression will drag on though most of 2015.

The economy will contract by 0.4pc this year. It will remain stuck in the doldrums next year with growth of just 0.1pc.

If so, Italy’s public debt will spiral to dangerous levels next year, ever further beyond the point of no return for a country without its own sovereign currency and central bank.

“This is catastrophic for the finances of the country. We’re heading for a debt ratio of 145pc next year,” said Antonio Guglielmi, global strategist for Mediobanca.

“Who knows the maximum number that the market will tolerate? The number is already scary, but for the time being Draghi’s poker game is proving successful, and there is now the smell of QE keep the game going for a bit longer.”

“It is going to take a nuclear bomb to turn this around. If Draghi ends up doing almost nothing – and there is a lot of scepticism about the ECB's plans – Italy is dead,” he said.

It has been an abominable few days for the Italian economy. ISTAT said today that industrial output fell by 1pc in July (m/m), and 1.8pc from a year ago. It is down a fifth since 2008.

Exports from the regions fell 2.5pc in the second quarter (q/q). The figures for the South were nothing less than catastrophic: Sicilia (-11.1), Sardegna (-11.2), Basilicata (-24.6). It seems that the Mezzogiorno is falling off the bottom of the Italian economy.

The OECD also slashed France’s growth by half a percentage point to 0.4pc this year. It cut Brazil by 1.5pc to 0.3pc. The Brazilian miracle is by now a structural wreck.

Yet it is the eurozone that remains the epicentre of hopelessness. “The recovery in the euro area has remained disappointing, notably in the largest countries: Germany, France and Italy. Confidence is again weakening, and the anaemic state of demand is reflected in the decline in inflation, which is near zero in the zone as a whole and negative in several countries.”

It called for QE, yet again, but such pleas are meaningless without a concrete number.

Italy’s debt reached 135.6pc of GDP in the first quarter, galloping upwards at a rate of 5pc of GDP each year. This is happening despite – or because of – a series of austerity packages, and even though the country is running a large primary budget surplus of 2pc-3pc of GDP. Plans to stabilise the debt have been blown to pieces.

Note that the Monti government said three years ago that the ratio would end 2014 at 115pc. That Panglossian estimate is likely to be wrong by 25 percentage points of GDP. That is a staggering error in such a short space of time. Was it bad luck, or were those crafting policy in denial about the fundamental nature of Italy’s EMU-rooted crisis?

Zolt Darvas from the Bruegel think tank in Brussels said Italy’s nominal GDP is flat or contracting, meaning that it must sustain a rising debt load on a static base. This is a classic debt-compound trap.

“The OECD forecast for Italy is a negative shock. Everything now depends on growth dynamics, and that depends on the ECB. I don’t think the ECB is yet doing enough,” said Mr Darvas.

He said markets are mistaken if they think that the forthcoming blast of ECB lending (TLTROs) will act as super-stimulus merely because it boosts the ECB’s balance sheet (perhaps by €1 trillion over time). “The balance sheet is not a meaningful indicator. It has very few implications for monetary policy. Only purchases of assets will really make a difference,” he said.

Exactly so, and we don’t yet know whether that will be a token gesture – like its earlier purchases of €60bn of covered bonds – or on a relevant scale. The ECB’s Yves Mersch said in a speech last week that this would be nothing like Anglo-Saxon QE, and nor is it intended to be. It is worth reading for a salutary cold douche.

Italy’s rock star leader Matteo Renzi must by now have realised that his first gamble has failed. He thought he could ride a wave of recovery after snatching power in February in a remarkably audacious move in February, only to discover that Europe is not in fact recovering, and that his country is trapped, with no way out under the current deflationary/contractionary policies of the EMU regime.

If Italy slashes wages and deflates the economy further to regain lost competitiveness within EMU, the “denominator effect” will automatically cause the debt ratios to rise. There is no plausible remedy to this unless EMU switches tack to massive reflation, which the ECB is not in fact about to do.

Mr Renzi will soon have to make a second gamble, whether to go along meekly with further austerity and fiscal cuts – chasing his tail in a perpetual vicious circle – and suffer the disastrous fate of French leader Francois Hollande. Or think of a better idea.

I hand it over to Italian readers to suggest which of the two he might choose given his tempestuous character.

[ Bericht 14% gewijzigd door Drugshond op 01-10-2014 16:08:20 ]

Mr Renzi's choice is not the currency but fixing the structural problems which are paralyzing the country. These are the real issues and, unfortunately, the current political system based on patronage, nepotism and salotti buoni capitalism is unlikely to allow him to make the necessary reforms

Een van de reakties.

Een van de reakties.

Het is niet makkelijk maar uiteindelijk wel de enige uitweg. Structurele hervormingen en dus pijnlijke maatregelen.quote:

Mr Renzi's choice is not the currency but fixing the structural problems which are paralyzing the country. These are the real issues and, unfortunately, the current political system based on patronage, nepotism and salotti buoni capitalism is unlikely to allow him to make the necessary reforms

Een van de reakties.

Ik denk dat ze een belastingdienst moeten optuigen, zitten ze in no time in een begrotingsoverschot, en de officiele GDP schiet omhoog.quote:

[..]

Het is niet makkelijk maar uiteindelijk wel de enige uitweg. Structurele hervormingen en dus pijnlijke maatregelen.

so long and thanks for all the fish

Haha, dat zal flink schelen inderdaadquote:

[..]

Ik denk dat ze een belastingdienst moeten optuigen, zitten ze in no time in een begrotingsoverschot, en de officiele GDP schiet omhoog.

Nee, ik heb mijn handen al vol met POL-SC.quote:

En offtopic, Drugshond, wordt jij de nieuwe AEX mod?

Je ken toch wel multitasken? Copy paisten gaat al heel behoorlijk zie ik.quote:Op woensdag 1 oktober 2014 20:27 schreef Drugshond het volgende:

[..]

Nee, ik heb mijn handen al vol met POL-SC.

so long and thanks for all the fish

Ach, ik kon het proberen, hequote:

Nee ik ben al ooit mod geweest. Het is leuk geweest,

so long and thanks for all the fish

|

|