WGR Werk, Geldzaken, Recht en de Beurs

Hier kun je alles kwijt over sollicitaties, werksituaties, belastingen, (handelen op) de beurs, hypotheken, beleggingen en salarissen, arbeidscontracten of geschillen met je (huis)baas. Alles over werk, geldzaken en recht dus.

Er zit nog 826 miljoen in het potje.....

Do the math...

Bank 34 was op Tuesday, May 19th, 2009

Bank 69 was op Sunday, August 2nd, 2009

(4971 - 826) = 4145 miljoen verdampt in 4,5 mnd.

Grofweg kunnen we zeggen dat de FDIC volgende maand out of options is.

Warning Related To The FDIC

I'm going to put this bluntly, at the risk of being called an "extreme doomer", even though the scenario I am outlining here has only, at this point, a reasonably-small (perhaps 10-20%?) chance of happening.

During the S&L Crisis many people who had (up to $100,000 at the time) money below insured limits were prevented from getting all their money at once.

The circumstances?

The same as we have today: State-run insurance, which insured some S&L accounts, ran out of money, just as the FDIC is out of money under any rational accounting.

Note that these insurance funds were "backed" by the full faith and credit of the respective government just as is the FDIC. Nobody lost money, and so Sheila Bair's (and Suze Orman's) claim that "nobody has ever lost a penny in insured deposits" (so far) is true.

However, some people were only able to get a limited amount of money - in some cases $750 to $900 a month or so - out of their accounts, and that state of affairs persisted for quite some time.

It is thus my position that even if you are well under FDIC limits you must move money around now so you have multiple bank accounts and thus if your withdrawals and access to your funds are "rationed" in a similar fashion you will be able to access what you need to pay your electric bill, put gas in your car and buy your food.

Remember, getting your money back doesn't mean getting it all right now, and government agencies can be very inflexible when what they have decided to do conflicts with what you want.

Since the government is not going to do the right thing with regard to these financial institutions and their alleged "assets", say much less crooked accounting and disclosures - a fact that now, two years into this mess, should be the inescapable conclusion reached by anyone with a brain in their head - you need to protect yourself.

With Alabama musing calling up the National Guard in Jefferson County, the utter refusal of any regulatory or law enforcement agency to enforce any part of the law when it comes to the outrageously fraudulent actions in our financial system up and down the line for the previous five years, documented conspiracy between OTS and Thrifts (only one of several that was named) with backdating of deposits and the fact that the FDIC will need to go to Treasury for a lot more funds - which Treasury will have to try to raise in the bond market into an environment of fear due to the FDIC's request for that money.

If that issuance happens without sentiment cracking due to the failures that result in this need, then we might get through that event without major trauma.

If, on the other hand, those failures cause a shift in sentiment then the nightmare scenario - a sell-off in all of stocks, bonds and the dollar - at the same time - is very likely.

The damage that would result from such an event would make last fall and the early-spring selloffs look like a cake walk.

God helps those who help themselves.

===========================================================================

FDIC tells banks to recognize mortgage losses promptly

SAN FRANCISCO (MarketWatch) -- The Federal Deposit Insurance Corp. said late Monday that banks should recognize losses on home loans promptly and warned that failure to do so could delay efforts to mitigate the financial impact.

Institutions must analyze the collectibility of the loans they hold for investment at least every quarter, the FDIC said in a statement on its Web site.

Banks then have to keep an appropriate allowance for loan and lease losses, covering estimated credit losses on individually evaluated loans that are deemed to be impaired, and on groups of loans with similar risk characteristics, the regulator said.

"When estimating credit losses on each group of loans with similar risk characteristics, an institution should consider its historical loss experience on the group, adjusted for changes in trends, conditions, and other relevant factors in the current economic environment," the FDIC said.

This is especially important for loans secured by junior liens on 1-4 family residential properties in areas where there have been declines in the value of such properties, the regulator said.

"Failure to timely recognize estimated credit losses could delay appropriate loss mitigation activity, such as restructuring junior lien loans to more affordable payments or reducing principal on such loans to facilitate refinancings," the FDIC said

===================================================================================

De vraag is heel simpel... als de FDIC niets meer kan garanderen hoelang gaat het duren voordat er een run op de FDIC banken komt. Mijn gevoel zegt 1 mnd als er geen oplossing komt.

O ja dat is denk ik ook de hoofdreden dat Geitners plan toast is --> Geitners plan....what are the stakes ? lees ff de OP.

Voordat het plan opgetuigd kon worden liepen de gegarandeerde verliezen van banken die omvallen al te hoog op.

Voordat het plan opgetuigd kon worden liepen de gegarandeerde verliezen van banken die omvallen al te hoog op.

njah er zijn dagen dat ik minder op zak heb.quote:

National Suicide: How Washington is Destroying the American Dream

Over een paar jaar koop je daar net een ijsje voor, net als in Zimbabwe.quote:Op donderdag 6 augustus 2009 07:44 schreef edwinh het volgende:

[..]

njah er zijn dagen dat ik minder op zak heb.

De FDIC zal ook wel 'gered' worden met bijgedrukt geld.

Goud kan je niet bijdrukken

No problem, just rape the taxpayer once more...

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Begin 2008 was de situatie als volgt.

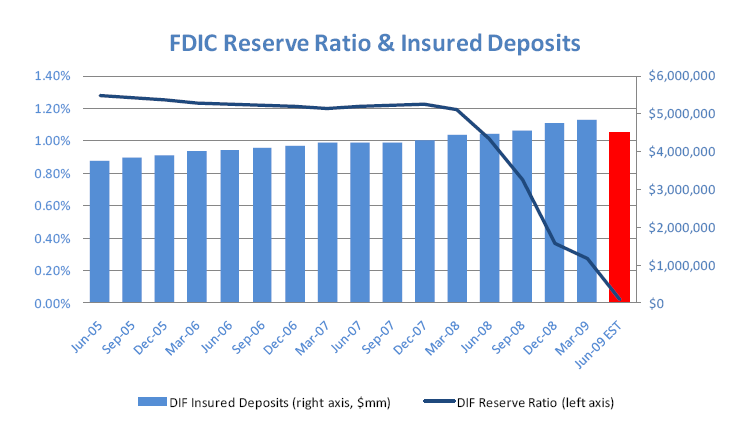

The fund held $52.4 billion at the beginning of 2008. One year and 25 bank failures later, the fund held $18.9 billion.

En nu nog minder dan 1 biljoen.

M.a.w. 51,5 biljoen verdampt....... and the show must go on. En dat zijn wel klinkende cijfers.

The fund held $52.4 billion at the beginning of 2008. One year and 25 bank failures later, the fund held $18.9 billion.

En nu nog minder dan 1 biljoen.

M.a.w. 51,5 biljoen verdampt....... and the show must go on. En dat zijn wel klinkende cijfers.

O ja... in maart dit jaar is er nog een poging ondernomen om de bijdrage van banken te verhogen zonder veel succes.... Nu gaat men de trier 1 ratio verlagen van 15 naar 10 %..... het zogenaamde bookcooking (om banken overeind te houden).

Ddan valt het mee wil je zeggen.quote:Op vrijdag 7 augustus 2009 01:30 schreef JodyBernal het volgende:

Het gaat volgens mij niet om biljoenen, maar 'slechts' om miljarden. ;-)

Ik zie greenshoots, in 2008 heeft men dus 44 miljard laten verdampen en dit jaar nog maar 4 miljard. Dat is 90 % minder.quote:Op vrijdag 7 augustus 2009 01:17 schreef Drugshond het volgende:

M.a.w. 51,5 biljoen verdampt....... and the show must go on. En dat zijn wel klinkende cijfers.

idd positief bekijkenquote:Op vrijdag 7 augustus 2009 11:08 schreef Basp1 het volgende:

[..]

Ik zie greenshoots, in 2008 heeft men dus 44 miljard laten verdampen en dit jaar nog maar 4 miljard. Dat is 90 % minder.

1/10 Van de rappers dankt zijn bestaan in Amerika aan de Nederlanders die zijn voorouders met een cruiseschip uit hun hongerige landen ophaalde om te werken op prachtige plantages.

"Oorlog is de overtreffende trap van concurrentie."

"Oorlog is de overtreffende trap van concurrentie."

Veel commercial real estate zit bij die locale banken waarvan klanten deposits door de FDIC worden gegarandeerd.

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

As of Friday August 14, 2009, FDIC is Bankrupt

Binnen 2 weken dusquote:Op woensdag 5 augustus 2009 22:41 schreef Drugshond het volgende:

Mijn gevoel zegt 1 mnd als er geen oplossing komt.

Ik was dit topic alweer vergeten.

Dus nu zal het garantiestelsel wel een bailout krijgen...

Dus nu zal het garantiestelsel wel een bailout krijgen...

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Wat een oppertunisten slingerden er toch 10 jaar lang rond

quote:Now-needy FDIC collected little in premiums

With fund going strong, banks didn't pay for decade

By Michael Kranish

Globe Staff / March 11, 2009

WASHINGTON -

The federal agency that insures bank deposits, which is asking for emergency powers to borrow up to $500 billion to take over failed banks, is facing a potential major shortfall in part because it collected no insurance premiums from most banks from 1996 to 2006.

Graphic Deposit Insurance Fund Balance The Federal Deposit Insurance Corporation, which insures deposits up to $250,000, tried for years to get congressional authority to collect the premiums in case of a looming crisis. But Congress believed that the fund was so well-capitalized - and that bank failures were so infrequent - that there was no need to collect the premiums for a decade, according to banking officials and analysts.

.......

En momenteel onderschat iedereen ook nog eens de kosten van bankfaillisementen omdat Obama de 'mark to fantasy' accounting heeft uitgebreid zodat banken zelf kunnen bepalen tegen welke waarde ze dingen in hun boeken zetten. Assets die bijv 60% van hun facevalue waard zijn staan tegen 100% in de boeken. Het gaat weer beter met de banken! Green shoots!  . Als de bank uiteindelijk onvermijdelijk failliet gaat dan staat je een leuke verrassing te wachten

. Als de bank uiteindelijk onvermijdelijk failliet gaat dan staat je een leuke verrassing te wachten

Obama

Obama

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Ze hopen natuurlijk dat de economie snel weer aantrekt en dat alle verliezen daardoor snel verwateren. Vervolgens kan ook 'mark to fatasy' accounting weer stilletjes worden afgeschaft.quote:Op zaterdag 15 augustus 2009 18:27 schreef SeLang het volgende:

En momenteel onderschat iedereen ook nog eens de kosten van bankfaillisementen omdat Obama de 'mark to fantasy' accounting heeft uitgebreid zodat banken zelf kunnen bepalen tegen welke waarde ze dingen in hun boeken zetten. Assets die bijv 60% van hun facevalue waard zijn staan tegen 100% in de boeken. Het gaat weer beter met de banken! Green shoots!

Obama

Echter, die economie gaat niet snel weer aantrekken zolang de consument de hand op de knip houdt. Door dit alles zijn banken nu inderdaad extra kwetsbaar, en als het over enige tijd weer verkeerd gaat, trekken de banken in één keer het hele land met zich mee de afgrond in.

Ik las ergens dat de boekhoudregels binnenkort waarschijnlijk weer worden aangescherpt en dat er een plan is om te verplichten dat zowel 'mark to market' als 'mark to fantasy' worden gerapporteerd. Natuurlijk zullen beleggers de 'mark to fantasy' cijfers dan erg kritisch gaan bekijken als er een groot verschil is met 'mark to market'. ALS ze zoiets gaan invoeren kun je weer lekker wat volatiliteit verwachten in bankaandelen

"If you want to make God laugh, tell him about your plans"

Mijn reisverslagen

Mijn reisverslagen

Nou ze willen de boekhoudkundige regels weer transparant/uniform maken. Ze zijn nu bezig om deze regels flink aan te scherpen (nieuwe protocol). Diverse gerenommeerde accountantskantoren willen zeker niet de klap opvangen als je ziet hoe sommige financiële jaarverslagen de laatste tijd creatief zijn opgeleukt.quote:Op zondag 16 augustus 2009 01:56 schreef SeLang het volgende:

Ik las ergens dat de boekhoudregels binnenkort waarschijnlijk weer worden aangescherpt en dat er een plan is om te verplichten dat zowel 'mark to market' als 'mark to fantasy' worden gerapporteerd.

Yup...quote:Natuurlijk zullen beleggers de 'mark to fantasy' cijfers dan erg kritisch gaan bekijken als er een groot verschil is met 'mark to market'. ALS ze zoiets gaan invoeren kun je weer lekker wat volatiliteit verwachten in bankaandelen

Ach, er kunnen nog duizenden banken failliet gaan zonder dat er een echt probleem ontstaat. Wat écht een probleem zou zijn is wanneer de drukpers kapot gaat. Dan pas is het tijd voor paniek.

The End Times are wild

|

|