POL Politiek

Discussies en diepgaande gesprekken over de politiek in de breedste zin van het woord kun je hier voeren.

Nee hoor. Jij bent kennelijk alleen niet oprecht geïnteresseerd in een antwoord, terwijl ik dat bij de PVV wel ben. Ik zoek dan ook regelmatig zaken over die partij uit, terwijl jij niet verder komt dan wat moddergooien.quote:Op dinsdag 28 maart 2017 13:07 schreef bluemoon23 het volgende:

[..]

Klaver heeft geen plan zo te horen

Als dit een PVVer was dan had jij hem tot de grond toe afgebrand

Nogmaals: vraag het hem..

[ Bericht 0% gewijzigd door keste010 op 29-03-2017 11:35:42 ]

"We do not measure a culture by its output of undisguised trivialities, but by what it claims as significant"

Neil Postman - Amusing Ourselves to Death

Neil Postman - Amusing Ourselves to Death

Gek genoeg is er weinig neoliberaal aan de Nederlandse schuldbehandeling. In Anglo-Saksische landen zijn ze vaak veel coulanter met het wegstrepen van schulden. Daar zijn hypotheken bijvoorbeeld ook af te lossen door de bank de sleutels van het onderpand te geven. Het is eerder continentaal-Europees (niet neoliberaal) dat we mensen hier aan hun schulden en sanering houden.quote:Op woensdag 29 maart 2017 00:02 schreef Klopkoek het volgende:

[..]

Die schuldhulp programma's bestaan sinds 2003 ongeveer. In ieder geval lang voor de recessie. Denk aan de Frogers.

Veel eerder kon ook niet omdat voor 1998 de schuldenwet anders in elkaar zat. Het is een typische neoliberale wet waarbij de problemen van kwaad tot erger gaan (en als er nog geen schulden zijn, dan schuift men die in je schoenen).

'Goed gaan met een land' is altijd een lastig ding. Qatar is stinkend rijk maar velen zijn er straatarm en zonder rechten.

Uiteraard is er wel een sterke correlatie tussen nationale welvaart en armoede; tussen ongelijkheid en rijkdom van landen.

Power is a lot like real estate, it's all about location, location, location.

The closer you are to the source, the higher your property value.

The closer you are to the source, the higher your property value.

Ik denk dat ook daar de trend is geweest naar steeds hardvochtiger wetgeving. Voor zover je dat kan generaliseren.quote:Op woensdag 29 maart 2017 11:26 schreef GSbrder het volgende:

[..]

Gek genoeg is er weinig neoliberaal aan de Nederlandse schuldbehandeling. In Anglo-Saksische landen zijn ze vaak veel coulanter met het wegstrepen van schulden. Daar zijn hypotheken bijvoorbeeld ook af te lossen door de bank de sleutels van het onderpand te geven. Het is eerder continentaal-Europees (niet neoliberaal) dat we mensen hier aan hun schulden en sanering houden.

Zeker, de Britse wet uit 1986 versoepelde ook het één en ander, vooral voor bepaalde typen bedrijven en sectoren (wat weer een weerslag had op acquisitiefraude e.d.). Echter, deze wet creëerde in ieder geval een hele industrie eromheen ('insolvency practicioners'), iets dat we ook in Nederland hebben gezien.

Voor de ideologische basis achter het scheppen van deze industrie:

https://books.google.nl/b(...)#v=onepage&q&f=false

Voeg dit samen met de andere trends (toegenomen langdurige armoede) en men blijft soms jarenlang in de overlevingsmodus rondhangen, waar een hele groep roofdieren van profiteren. Waarbij de incentives niet in het voordeel van de schuldenaar werken.

In de Verenigde Staten hebben de neocons van Bush in 2005 hun kans gegrepen.

http://money.cnn.com/2005/04/20/pf/bankruptcy_bill/

Een wetswijziging die mogelijk ook nog een rol had bij de implosie van de huizenmarkt.

http://www.huffingtonpost(...)osures_n_820491.html

http://www.washingtonfres(...)nkruptcy-Law-He.html

http://www.huffingtonpost(...)t_1440_b_797563.htmlquote:That homeowners would default on the unaffordable mortgages was a foregone conclusion. Indeed, it was the desired result of the business model. The preferred marketed loans tell it all: Subprimes! NINJAs! Liar’s loans! Washington helpfully changed bankruptcy law to make it more difficult for a homeowner to get out of mortgage debt in preparation for the wave of defaults that everyone knew would result. Wall Street would get the homes, and homeowners would still have to pay on the debts. Then the foreclosed property would be resold, with more fees for everyone in the finance food chain, and the whole process through to default would begin again — a nice virtuous cycle.

It might seem strange that banks would actually want default. But that is the beauty of a casino — the house always wins, and homebuyers were gambling against the casino. On the way up, fees are collected, and on the way down fees are still collected on the foreclosures and as houses are resold. And if anything should go wrong, Washington backstops the casinos.

But it was necessary to streamline foreclosure to make it as fast and cheap as possible. Enter MERS — another link in the food chain — created by the banks in 1997 in preparation for the boom and bust. MERS was set up to be a foreclosure mill. It would break the centuries-old custom that protected property rights by requiring every sale of property to be publicly recorded, and requiring that any creditor claiming a right to foreclose to demonstrate clear title, with an endorsed note in the creditor’s name and a record at the county office showing transfer of the property.

The banksters did not want to go through all that paperwork, and needed to subvert the transparency that would shine light on their crimes. Hence, they set up a fraudulent shell corporation that claimed to be the mortgagee; while the original sale would be recorded at the county office, subsequent sales and purchases of the mortgage would be recorded only by an “electronic handshake” between two “members” of MERS. Even that record was considered by the banksters to be purely voluntary — MERS did not require members to actually record transactions. If they found it more convenient to conceal the transfers, that was permitted.

http://www.slate.com/arti(...)aw_for_the_poor.htmlquote:One law for the rich, one law for the poor

Joseph Stiglitz

[...]

When it became clear that people could not pay back what was owed, the rules of the game changed. Bankruptcy laws were amended in 2005 to introduce a system of "partial indentured servitude." An individual with, say, debts equal to 100 percent of his income could be forced to hand over to the bank 25 percent of his gross, pre-tax income for the rest of his life, because the bank could add on, say, 30 percent interest each year to what a person owed. In the end, a mortgage holder would owe far more than the bank ever received, even though the debtor had worked, in effect, one-quarter time for the bank.

When this new bankruptcy law was passed, no one complained that it interfered with the sanctity of contracts: At the time borrowers incurred their debt, a more humane—and economically rational—bankruptcy law gave them a chance for a fresh start if the burden of debt repayment became too onerous.

That knowledge should have given lenders incentives to make loans only to those who could repay them. But lenders perhaps knew that, with the Republicans in control of government, they could make bad loans and then change the law to ensure that they could squeeze the poor.

[...]

Lenders complain that such a law would violate their property rights. But almost all changes in laws and regulations benefit some at the expense of others. When the 2005 bankruptcy law was passed, lenders were the beneficiaries—they didn't worry about how the law affected the rights of debtors.

Growing inequality, combined with a flawed system of campaign finance, risks turning America's legal system into a travesty of justice. Some may still call it the "rule of law," but it would not be a rule of law that protects the weak against the powerful. Rather, it would enable the powerful to exploit the weak.

Er zijn economen en historici die claimen dat Jimmy Carter de eerste "neoliberale" president was. Wat dan altijd langs komt in de beschouwing is de 1978 Bankruptcy Law wijziging.

Om een lang verhaal kort te maken (en terug te komen tot de essentie) ik denk dat dezelfde trend zich ook in de Verenigde Staten en Verenigd Koninkrijk heeft afgespeeld, en nog wel eerder begon dan de Nederlandse wetswijziging van 1998. In de VS heeft dit een 'third party debt collection' industrie geschapen van tenminste 50 miljard dollar... puur en alleen de consumenten tak.

Graag een oprecht antwoord... als jij denkt dat sinds pakweg ~1980 de relevante wetten soepeler zijn geworden - soepeler voor de schuldenaar - dan moet je dat zeggen en graag beargumenteren. Ik denk zoals gezegd van niet, en de 2005 wetswijziging door de neocons is het duidelijkste voorbeeld (inclusief het ophogen van incassokosten en rente - zie het treffende stuk van Stiglitz).

N.B. dit gaat over huiseigenaren, consumenten en personen. Niet zozeer bedrijven of de in de wet verankerde rechtspersonen, en zoals Stiglitz aan geeft gelden voor de vermogenden wéér andere regels.

[ Bericht 1% gewijzigd door Klopkoek op 29-03-2017 13:16:39 ]

Deuger & Gutmensch

"Conservatism consists of exactly one proposition, to wit: There must be in-groups whom the law protects but does not bind, alongside out-groups whom the law binds but does not protect."

"Conservatism consists of exactly one proposition, to wit: There must be in-groups whom the law protects but does not bind, alongside out-groups whom the law binds but does not protect."

Voordat we even daarop antwoord geven, even terug naar de oorspronkelijke vraag. Het ging er over of het neoliberaal was (versus Rijnlands of hoe je het ook wil noemen) dat mensen relatief eenvoudig van schulden af komen. Op Wikipedia over bankroet staat er het volgende:quote:

[..]

Ik denk dat ook daar de trend is geweest naar steeds hardvochtiger wetgeving. Voor zover je dat kan generaliseren. De Britse wet uit 1986 versoepelde ook het één en ander, vooral voor bepaalde typen bedrijven en sectoren (wat weer een weerslag had op acquisitiefraude e.d.). Deze wet creëerde in ieder geval een hele industrie eromheen ('insolvency practicioners'), iets dat we ook in Nederland hebben gezien.

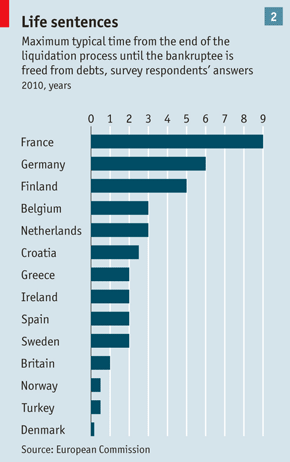

[ afbeelding ]

https://books.google.nl/b(...)#v=onepage&q&f=false

Voeg dit samen met de andere trends (toegenomen langdurige armoede) en men blijft soms jarenlang in de overlevingsmodus rondhangen, waar een hele groep roofdieren van profiteren.

In de Verenigde Staten hebben de neocons van Bush in 2005 hun kans gegrepen.

http://money.cnn.com/2005/04/20/pf/bankruptcy_bill/

Een wetswijziging die mogelijk ook nog een rol had bij de implosie van de huizenmarkt.

http://www.huffingtonpost(...)osures_n_820491.html

http://www.washingtonfres(...)nkruptcy-Law-He.html

[..]

http://www.huffingtonpost(...)t_1440_b_797563.html

[..]

http://www.slate.com/arti(...)aw_for_the_poor.html

Er zijn economen en historici die claimen dat Jimmy Carter de eerste "neoliberale" president was. Wat dan altijd langs komt in de beschouwing is de 1978 Bankruptcy Law wijziging.

Om een lang verhaal kort te maken (en terug te komen tot de essentie) ik denk dat dezelfde trend zich ook in de Verenigde Staten en Verenigd Koninkrijk heeft afgespeeld, en nog wel eerder begon dan de Nederlandse wetswijziging van 1998. In de VS heeft dit een 'third party debt collection' industrie geschapen van tenminste 50 miljard dollar... puur en alleen de consumenten tak.

[ afbeelding ]

Graag een oprecht antwoord... als jij denkt dat sinds pakweg ~1980 de relevante wetten soepeler zijn geworden - soepeler voor de schuldenaar - dan moet je dat zeggen en graag beargumenteren. Ik denk zoals gezegd van niet, en de 2005 wetswijziging door de neocons is het duidelijkste voorbeeld.

Daarnaast, in landen als de UK en de USA komen (individuele) faillissementen vaker voor en slepen ze minder lang voort. Ook kennen enkele staten in de VS (niet allemaal) een non-recourse bescherming, waarmee individuele huishoudens bescherming genieten als ze hun hypotheek niet kunnen aflossen voor hun overige bezittingen. In landen als Nederland is dit (ook nu nog) anders. Dus zowel de norm van het persoonlijk faillissement is verschillend als het effect op latere jaren. Zie hiervoor de volgende stukken, cijfers en grafieken. Dit is uiteraard met nodige tekortkomingen, maar dat niet als mistgordijn, maar wel om e.e.a. op het gebied van debt, debt relief en bankruptcy in perspectief te plaatsen:quote:In most EU Member States, debt discharge is conditioned by a partial payment obligation and by a number of requirements concerning the debtor's behavior. In the United States (US), discharge is conditioned to a lesser extent. The spectrum is broad in the EU, with the UK coming closest to the US system (Reifner et al., 2003; Gerhardt, 2009; Frade, 2010). The Other Member States do not provide the option of a debt discharge. Spain, for example, passed a bankruptcy law (ley concurs) in 2003 which provides for debt settlement plans that can result in a reduction of the debt (maximally half of the amount) or an extension of the payment period of maximally five years (Gerhardt, 2009), but it does not foresee debt discharge.

[quote]Next, the authors present empirical analysis. This part of the paper is both the most provocative and most problematic. The authors claim to find evidence that borrowers protected from recourse default more often than borrowers who are not. Specifically, they estimate a probit specification in which the dependent variable is an indicator of whether or not the borrower defaults on the mortgage, and the independent variable of interest is the amount of equity in the home interacted with whether or not the state allows lender recourse. They find a statistically significant negative effect of recourse on the propensity to default—meaning that borrowers are more likely to exercise their default option (conditional on a given value of equity) in states that do not allow lender recourse.

Bron: Non-recourse mortgages effect on mortgage crisis[/quote]

UK Insolvencies (80,000 op 56m inwoners of 1,43 per 1000)

NL Individuele faillissementen (2,046 op 17,1m inwoners of 0,43 per 1000)

Een oprecht antwoord; ik denk dat in een land als Nederland er een groter stigma zit op een persoonlijk faillissement en het volledig financieel onderuit gaan, dan in landen met een andere risicoperceptie, zoals de Verenigde Staten en de UK. Mede doordat we hier (nog) een beter sociaal stelsel hebben, zullen mensen minder begrip hebben voor faillissementen en zijn ze op huishoudniveau ook schaarser. In de VS is het dan toch meer van: "Ach, je hebt het geprobeerd, volgende keer beter." We kunnen het ons niet voorstellen dat Rutte 3 keer persoonlijk failliet was verklaard, maar in de VS is dat blijkbaar geen belemmering en toont het de ondernemingskracht van Trump.

Los daarvan ondermijn ik hiermee niet jouw stelling over eventuele Amerikaanse krachten die bij huishoudens de duimschroeven aandraaien. Je mag zeggen dat zoiets typisch neocon/neoliberaal is, maar in mijn ogen krijgt de VS hiermee eerder een Europees karakter, dan dat dit bij Nederland ook de voorbode is van hoe we met schulden om zullen gaan. We hebben hier geen enkele non-recourse hypotheek, faillissementen komen minder vaak voor en het "Repo men"-verhaal zie ik in Nederland nog niet snel afspelen, omdat onze consumptieve schuldenberg lager ligt en we vooral (en veel) lenen om onze huizen van te betalen.

Power is a lot like real estate, it's all about location, location, location.

The closer you are to the source, the higher your property value.

The closer you are to the source, the higher your property value.

Ik ontken de historisch gegroeide verschillen niet en dat maakt het ook dat failliesementsverklaringen moeilijk zijn te vergelijken. Niemand gelooft werkelijk dat Trump echt drie keer platzak was.quote:

[..]

Los daarvan ondermijn ik hiermee niet jouw stelling over eventuele Amerikaanse krachten die bij huishoudens de duimschroeven aandraaien. Je mag zeggen dat zoiets typisch neocon/neoliberaal is, maar in mijn ogen krijgt de VS hiermee eerder een Europees karakter, dan dat dit bij Nederland ook de voorbode is van hoe we met schulden om zullen gaan. We hebben hier geen enkele non-recourse hypotheek, faillissementen komen minder vaak voor en het "Repo men"-verhaal zie ik in Nederland nog niet snel afspelen, omdat onze consumptieve schuldenberg lager ligt en we vooral (en veel) lenen om onze huizen van te betalen.

Zoals ik al zei is m.i. de trend dezelfde kant op. De meest significante herzieningen in de VS dateren van 1978 en 2005. Zoals gezegd wordt Jimmy Carter o.a. hierom af en toe de eerste neoliberale president genoemd (ik laat in het midden of ik het daarmee eens ben). De meest significante herzieningen in de UK dateren van 1986 (die daarvoor van 1888!) en het laatste decennium onder Cameron.

Ten dele was een reactie noodzakelijk omdat na ~1980 de schuldenberg explodeerde (door Crouch en Mazzucato 'privatised Keynesianism' genoemd). Men moest daarmee iets doen. En hoewel het voor rechtspersonen een iets ander verhaal is, houdt die trend grosso modo een aanscherping ('Europeanisering') in.

Ik denk niet dat je de Nederlandse 'hervorming' van 1998 als Rijnlands kunt aan merken. Indien wel, dan valt dat op meerdere manieren fors uit de toon.

Vwb. Repo Man praktijken: zoiets zal heel geleidelijk gaan. De politiek van 'no alternative' en 'voldongen feiten'.

Waarom is de wetgeving dan zo aangescherpt en veranderd in 1998? Toen de verzorgingsstaat al op de weg terug was, n.b. een gedepolitiseerd gegeven door datzelfde Paarse kabinet. Dito voor het Rijnlandse model met het opheffen van verplichte SER adviezen, productagentschappen enzovoorts.quote:Mede doordat we hier (nog) een beter sociaal stelsel hebben, zullen mensen minder begrip hebben voor faillissementen en zijn ze op huishoudniveau ook schaarser.

Datzelfde geldt natuurlijk ook voor Groot Brittanië en de Verenigde Staten, waar de welvaartsstaat eveneens is gesloopt (bijv. bijstand gemaximeerd tot 5 jaar). Volgens deze theorie zou je een coulantere wetgeving mogen verwachten, maar in plaats daarvan kreeg je een door banken verlangde aanscherping in 2005. Het begrip voor 'wanbetalers' is daar in de VS, dankzij gerichte propaganda en ophitserij', helemaal niet groter geworden zelfs al zijn die 'uitvreters' doelbewust in de val gelokt met 30% boeterentes die niet eens in de geleverde voorwaarden stonden.

Deuger & Gutmensch

"Conservatism consists of exactly one proposition, to wit: There must be in-groups whom the law protects but does not bind, alongside out-groups whom the law binds but does not protect."

"Conservatism consists of exactly one proposition, to wit: There must be in-groups whom the law protects but does not bind, alongside out-groups whom the law binds but does not protect."

Waarom GL? Ligt die niet dusdanig te ver weg van de andere partijen om een goed functionerende coalitie te kunnen vormen? En GL wil vast geen PvdA worden die al haar standpunten de komende regeerperiode gaat verloochenen, want dan weten ze wel wat er met hun zetelaantal zal gebeuren bij de volgende verkiezingen.

Ik zou eerder een christelijke partij verwachten. Alleen gaan die misschien niet heel goed samen met m.n. D66, maar als je ze één puntje geeft waar ze blij van worden in ruil voor hun onvoorwaardelijke steun op de rest moet dat lukken, lijkt mij.

Ik zou eerder een christelijke partij verwachten. Alleen gaan die misschien niet heel goed samen met m.n. D66, maar als je ze één puntje geeft waar ze blij van worden in ruil voor hun onvoorwaardelijke steun op de rest moet dat lukken, lijkt mij.

Het weer zat niet mee

|

|