NWS Nieuws & Achtergronden

Discussieer hier diepgaander over de actualiteiten.

Hoezo oninbaar? Dat geld komt toch met rente terug?quote:Op woensdag 17 juni 2015 12:06 schreef Digi2 het volgende:

[..]

Bankrun neemt onhoudbare proporties aan. Hoeveel verliezen is de ECB bereid te nemen? Als alle tegoeden opgenomen zijn bij de griekse banken (ca 100 miljard euro nog). Dat zou betekenen dat de EU+eurozone straks ca 500 miljard kunnen afschrijven als oninbare tegoeden

Bedankt Hans.

Aha, dus de EU wil de Grieken dwingen tot een rechts-ideologische oplossing van een door rechtse ideologie veroorzaakt probleem, in weerwil van de uitkomst van een wel democratisch proces?quote:,,Varoufakis houdt hiermee de voortgang in de onderhandelen op,'' constateert Roel Beetsma, hoogleraar macro-economie aan de UvA. ,,De andere EU-landen willen concrete voorstellen voor hervormingen zien, zoals bezuinigingen op overheidsuitgaven of flexibilisering van de arbeidsmarkt. Zonder zulke maatregelen is de resterende noodsteun weggegooid geld.''

Het heeft er alle schijn van dat er een voorbeeld gesteld moet worden, de wel democratisch tot stand gekomen linkse regeringen moeten gekneveld worden, er volgt een strafexpeditie als je niet meedoet met de neoliberale 'oplossingen' van privatisering, bezuiniging op de overheidsuitgaven en verslechtering van de positie van de werknemer. Waag het niet de plannetjes om steeds meer geld van de werkenden naar de banken te verplaatsen te dwarsbomen, dan wordt je gepakt.

Wees gehoorzaam. Alleen samen krijgen we de vrijheid eronder.

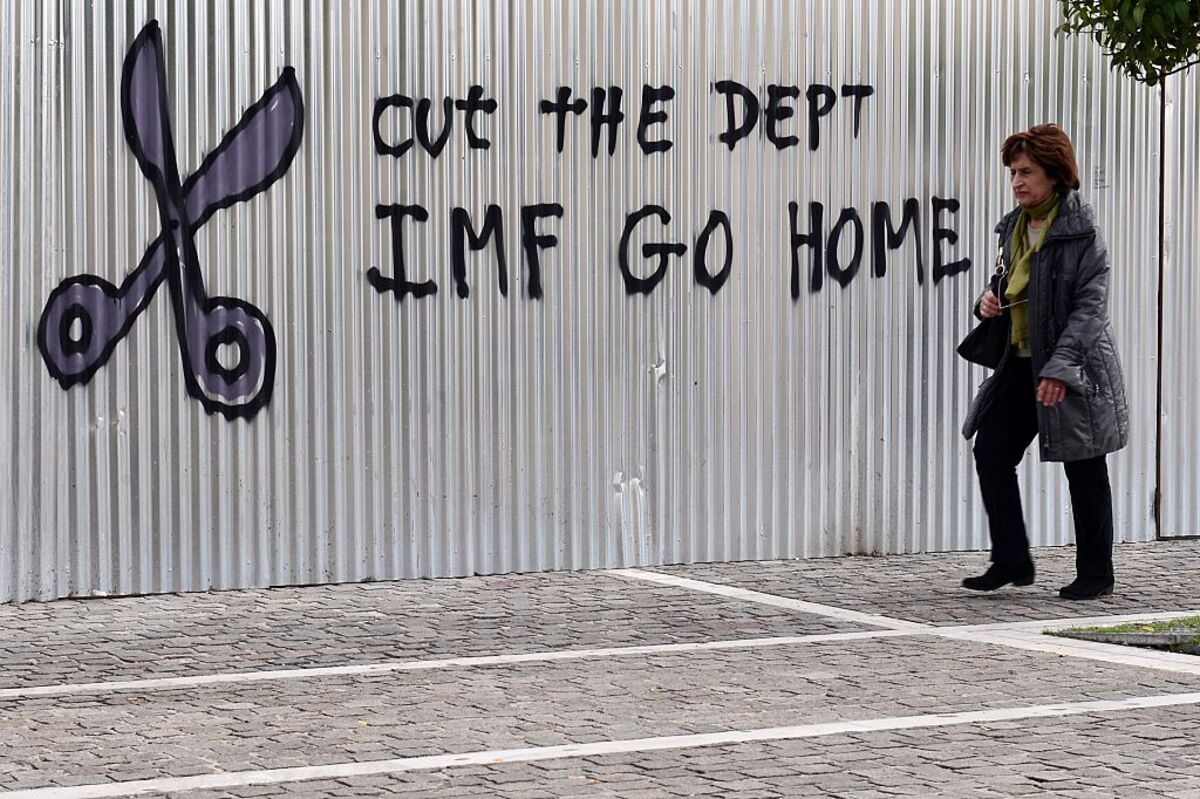

IMF Warns Eurogroup Loan Measures Not Enough for Greek Debt

• Greek debt is highly unsustainable; measures not specific

• Debt will jump as high as 275 percent of GDP by 2060

Greece’s public debt and financing needs will prove “explosive” in decades to come unless Europe overhauls its bailout program to ease the load, the International Monetary Fund says in a draft report as the country seeks a fresh loan payout.

In the IMF’s baseline scenario, Greece’s government debt will reach 275 percent of its gross domestic product by 2060, when its financing needs will represent 62 percent of GDP, the report obtained by Bloomberg says. The government estimates public debt around 180 percent of GDP at present.

The European Union’s view of the evolution of Greek debt is “more benign” and based on “significantly more optimistic assumptions,” the IMF notes. The document also says some Greek debt proposals by euro-area finance ministers “are not specific enough to enable a full assessment” of how they would affect sustainability.

Greece and its creditors are locked in negotiations on how the nation can close its fiscal gap, in line with the requirements of the 86 billion-euro ($92 billion) aid program agreed with the European Commission, the European Central Bank and the IMF. Failure to strike a deal would hold up the release of the next portion of bailout funding.

Europe Responds

The IMF board is set to discuss Greece’s ability to service its debt on Feb. 6. The fund has resisted pressure from countries including Germany and the Netherlands to contribute to the bailout program, seeing it as doomed unless Greece takes further steps to rein in spending or euro-area governments ease the terms of the loans.

Europe’s aid program for Greece is credible and backed by contingency measures to handle unforeseen events, a spokesman for the European Stability Mechanism, an EU agency that provides bailout loans to Greece, said in e-mailed statement Sunday.

“We see no reason for an alarmistic assessment of Greece’s debt situation,” the spokesman said, adding that Europe has made clear commitments to support the country with additional debt relief after the program. The statement makes no direct reference to the IMF draft.

IMF Proposals

As in the past, the IMF is proposing that Europe extend grace periods and maturity dates on the loans. The document also calls for further deferral of interest payments and to lock in interest rates.

For its part, Greece needs to tackle tax evasion and broaden its tax base, the IMF says, repeating recommendations in previous reports. It also needs to re-balance spending away from pensions and deal with bad loans that are weighing on banks.

Greek debt is “highly unsustainable” and “even with the full implementation of policies agreed under the European Stability Mechanism program, public debt and financing needs will become explosive in the long run,” the document says. A “substantial restructuring” of European loans to Greece is required to restore debt sustainability, it says.

The IMF agrees with Greece’s euro-area creditors on one point. Both want Greece to introduce a law triggering austerity measures if the country fails to maintain a budget surplus before interest payments of 3.5 percent of GDP. Greek Finance Minister Euclid Tsakalotos last week rejected that demand as “unacceptable.”

==============================================

De 3e bailout is bijna verdampt door de schuldenberg.

==============================================

Grexit? Greece again on the brink as debt crisis threatens break with EU

Country faces critical few weeks as it struggles to meet bailout conditions and pressures rise in Germany and US

In the week of Groundhog Day it seemed entirely appropriate: Greek farmers, many on tractors, have once again been blockading roads and border posts amid mounting signs that the country long at the centre of Europe’s debt woes is – once again – teetering towards crisis.

Protesting farmers have been a regular feature of the social unrest that has sporadically gripped Greece. It is now more than seven years since the Greek financial crisis erupted and the debt drama has often had a deja vu quality about it.

Eclipsed last year by the UK’s vote to exit the EU, and Donald Trump’s equally unlikely US electoral victory, the nation’s epic struggle to keep bankruptcy at bay has been out of the spotlight.

Greece has three weeks to deal with 'potentially disastrous' debt

Bailout negotiations between Athens and its creditors have stalled. The possibility of Grexit, or euro exit, has re-emerged and bond yields have soared. The yield on two-year Greek government bonds has risen from 6% to 10% in less than two weeks as spooked investors have dumped their holdings. And the shrill rhetoric last seen at the height of the crisis in 2015 has returned.

Analysts sensing dangerous deadlock are sounding the alarm – an alarm that the embattled prime minister, Alexis Tsipras, was expected to raise in talks with the German chancellor and other European leaders in Malta on Friday.

“I am very worried we are heading towards a rupture with the EU,” said Pantelis Kapsis, a prominent political commentator. “There are lots of signs that at the back of their minds people in Syriza [the ruling leftist party] are entertaining various ideas of going it alone. What is sure is that we are entering a very difficult period which quite possibly could lead us to a point of no return.”

As always, time is of the essence. Shored up by a third EU-led bailout, Athens was told this week that further rescue funds would not be forthcoming until it concluded a compliance review of terms attached to the €86bn (£74bn) aid package. In July Greece faces debt repayments of €7.4bn, raising the spectre of default because state coffers by then will have run dry.

The impasse has turned into a standoff as creditors demand additional austerity once the current bailout expires. Without further reduction of pensions – already cut 12 times since the crisis began – and the tax-free threshold of personal incomes, the International Monetary Fund (IMF) argues, the debt-stricken country will never be able to achieve its agreed fiscal goal of a primary surplus of 3.5% of GDP from 2018.

In a fiery parliamentary debate late on Wednesday, Tsipras dug in, insisting his two-party coalition – in power with a wafer-thin majority of two – would not cave in to demands that his government has repeatedly called absurd. “The IMF’s demands go beyond any democratic and constitutional logic and value,” he railed.

Alexis Tsipras arriving in Valletta, Malta, for the EU summit.

Facebook Twitter Pinterest

Alexis Tsipras arriving in Valletta, Malta, for the EU summit. Photograph: Leon Neal/PA

Completion of the review is essential to Greece, exiled from international capital markets, being included in the European Central Bank’s 9 March bond-buying programme, key to the country regaining market access. If the deadline is missed few believe Athens will be able to keep itself afloat without a fourth bailout once the latest loans end.

The stories you need to read, in one handy email

Read more

And in a Europe preoccupied with other matters – and in fear of an anti-establishment ascendant far right – the prospect of that happening is slim. “What we are witnessing is a disaster for the real economy because everything is on hold,” said Costas Panagopoulos who heads the Alco polling institute. “Once again we are talking about economic catastrophe, once again we are talking about Grexit,” he told the Guardian. “The next few weeks are critical. If an agreement isn’t reached, if there is more uncertainty, we don’t know how Greeks will react.”

On Thursday, amid widespread rumours of his own resignation, the finance minister Euclid Tsakalotos attempted to deflect the spiralling tensions. In a written statement the Marxist economics professor said that while a third of the bailout review had been “totally completed” and a third “totally agreed”, the rest remained subject to “political negotiation” – raising little hope of the talks concluding any time soon.

But what happens next is dependent not only on what happens in Athens. To a great degree events in Europe and Washington will also play a role.

Ahead of Germany’s general election in September, Berlin’s finance minister Wolfgang Schäuble has also raised the stakes with growing criticism of Greece – a tactic that has proved popular with voters who might otherwise support Germany’s far-right AfD party. Earlier this week Bild, the mass-selling newspaper, stoked passions further by suggesting the German government was warming to the idea of Greece leaving the euro – a notion Schäuble has openly supported in the past.

“Grexit is not our agenda, it is the agenda of those who want the breakup of Europe,” said Sia Anagnostopoulou, a leading Syriza MP and former alternate European affairs minister. “It is what Mr Schäuble wants,” she added, echoing the commonly held view that Athens is hostage to Germany.

Complicating matters further is the direction the IMF will take now that President Trump is in power. In his former role as a billionaire businessman, Trump tweeted that the Greeks were “wasting time” in the eurozone.

Last week, the IMF delivered its gloomiest assessment yet of Greece’s debt burden, arguing that it was not only unsustainable but eventually likely to become “explosive”. The IMF’s board will formally discuss the issue on 6 February but has already hinted that without a commitment of debt relief from the EU it will be unable to contribute further loans. Germany, the biggest contributor to the nearly €300bn of emergency funds assigned to Greece, insists further aid depends exclusively on IMF participation.

Analysts are undecided whether the government is deliberately stalling in the hope of getting a better deal as repayment season approaches and fears of a disorderly default mount, or whether it is playing with fire.

Syriza, like every governing party before it, has been hollowed out by the eviscerating effects of having to apply policies that it came to power vowing to oppose. On Tuesday its parliamentary spokesman took Greeks by storm proposing that Grexit be discussed “without taboo” in the 300-member house.

The once unassailable popularity of Tsipras, meanwhile, has been pummelled by the implementation of some of the harshest measures to date and few believe he has the political capital to enforce another round of austerity.

“It is not a can but a bomb being kicked down the road,” said one western diplomat. “In a world where liberal values are under threat we could be looking at a very dangerous scenario where the cradle of democracy also collapses.”

Bereft of growth and battered by cuts and tax increases, Greeks have become poorer and ever more cognizant of their own insolvency in a state where sovereignty exists in little more than name. One in three now live below the poverty line and unemployment hovers around 23%. The latest impasse has not only seen emigration levels rise and non-repayment of household and business loans soar but also nostalgia for the drachma grow.

That is what worries Panagopoulos, the pollster, most. What was once a minority view is changing fast, with the majority of Greeks in a recent Alco survey saying it was wrong to have joined the euro.

“We have become a society that has no hope, not even a slice or piece of hope for the future,” he sighed. “The only reason people want to stay in the euro is because they fear the consequences if we were to leave, but if things don’t get better that will change too.”

• Greek debt is highly unsustainable; measures not specific

• Debt will jump as high as 275 percent of GDP by 2060

Greece’s public debt and financing needs will prove “explosive” in decades to come unless Europe overhauls its bailout program to ease the load, the International Monetary Fund says in a draft report as the country seeks a fresh loan payout.

In the IMF’s baseline scenario, Greece’s government debt will reach 275 percent of its gross domestic product by 2060, when its financing needs will represent 62 percent of GDP, the report obtained by Bloomberg says. The government estimates public debt around 180 percent of GDP at present.

The European Union’s view of the evolution of Greek debt is “more benign” and based on “significantly more optimistic assumptions,” the IMF notes. The document also says some Greek debt proposals by euro-area finance ministers “are not specific enough to enable a full assessment” of how they would affect sustainability.

Greece and its creditors are locked in negotiations on how the nation can close its fiscal gap, in line with the requirements of the 86 billion-euro ($92 billion) aid program agreed with the European Commission, the European Central Bank and the IMF. Failure to strike a deal would hold up the release of the next portion of bailout funding.

Europe Responds

The IMF board is set to discuss Greece’s ability to service its debt on Feb. 6. The fund has resisted pressure from countries including Germany and the Netherlands to contribute to the bailout program, seeing it as doomed unless Greece takes further steps to rein in spending or euro-area governments ease the terms of the loans.

Europe’s aid program for Greece is credible and backed by contingency measures to handle unforeseen events, a spokesman for the European Stability Mechanism, an EU agency that provides bailout loans to Greece, said in e-mailed statement Sunday.

“We see no reason for an alarmistic assessment of Greece’s debt situation,” the spokesman said, adding that Europe has made clear commitments to support the country with additional debt relief after the program. The statement makes no direct reference to the IMF draft.

IMF Proposals

As in the past, the IMF is proposing that Europe extend grace periods and maturity dates on the loans. The document also calls for further deferral of interest payments and to lock in interest rates.

For its part, Greece needs to tackle tax evasion and broaden its tax base, the IMF says, repeating recommendations in previous reports. It also needs to re-balance spending away from pensions and deal with bad loans that are weighing on banks.

Greek debt is “highly unsustainable” and “even with the full implementation of policies agreed under the European Stability Mechanism program, public debt and financing needs will become explosive in the long run,” the document says. A “substantial restructuring” of European loans to Greece is required to restore debt sustainability, it says.

The IMF agrees with Greece’s euro-area creditors on one point. Both want Greece to introduce a law triggering austerity measures if the country fails to maintain a budget surplus before interest payments of 3.5 percent of GDP. Greek Finance Minister Euclid Tsakalotos last week rejected that demand as “unacceptable.”

==============================================

De 3e bailout is bijna verdampt door de schuldenberg.

==============================================

Grexit? Greece again on the brink as debt crisis threatens break with EU

Country faces critical few weeks as it struggles to meet bailout conditions and pressures rise in Germany and US

In the week of Groundhog Day it seemed entirely appropriate: Greek farmers, many on tractors, have once again been blockading roads and border posts amid mounting signs that the country long at the centre of Europe’s debt woes is – once again – teetering towards crisis.

Protesting farmers have been a regular feature of the social unrest that has sporadically gripped Greece. It is now more than seven years since the Greek financial crisis erupted and the debt drama has often had a deja vu quality about it.

Eclipsed last year by the UK’s vote to exit the EU, and Donald Trump’s equally unlikely US electoral victory, the nation’s epic struggle to keep bankruptcy at bay has been out of the spotlight.

Greece has three weeks to deal with 'potentially disastrous' debt

Bailout negotiations between Athens and its creditors have stalled. The possibility of Grexit, or euro exit, has re-emerged and bond yields have soared. The yield on two-year Greek government bonds has risen from 6% to 10% in less than two weeks as spooked investors have dumped their holdings. And the shrill rhetoric last seen at the height of the crisis in 2015 has returned.

Analysts sensing dangerous deadlock are sounding the alarm – an alarm that the embattled prime minister, Alexis Tsipras, was expected to raise in talks with the German chancellor and other European leaders in Malta on Friday.

“I am very worried we are heading towards a rupture with the EU,” said Pantelis Kapsis, a prominent political commentator. “There are lots of signs that at the back of their minds people in Syriza [the ruling leftist party] are entertaining various ideas of going it alone. What is sure is that we are entering a very difficult period which quite possibly could lead us to a point of no return.”

As always, time is of the essence. Shored up by a third EU-led bailout, Athens was told this week that further rescue funds would not be forthcoming until it concluded a compliance review of terms attached to the €86bn (£74bn) aid package. In July Greece faces debt repayments of €7.4bn, raising the spectre of default because state coffers by then will have run dry.

The impasse has turned into a standoff as creditors demand additional austerity once the current bailout expires. Without further reduction of pensions – already cut 12 times since the crisis began – and the tax-free threshold of personal incomes, the International Monetary Fund (IMF) argues, the debt-stricken country will never be able to achieve its agreed fiscal goal of a primary surplus of 3.5% of GDP from 2018.

In a fiery parliamentary debate late on Wednesday, Tsipras dug in, insisting his two-party coalition – in power with a wafer-thin majority of two – would not cave in to demands that his government has repeatedly called absurd. “The IMF’s demands go beyond any democratic and constitutional logic and value,” he railed.

Alexis Tsipras arriving in Valletta, Malta, for the EU summit.

Facebook Twitter Pinterest

Alexis Tsipras arriving in Valletta, Malta, for the EU summit. Photograph: Leon Neal/PA

Completion of the review is essential to Greece, exiled from international capital markets, being included in the European Central Bank’s 9 March bond-buying programme, key to the country regaining market access. If the deadline is missed few believe Athens will be able to keep itself afloat without a fourth bailout once the latest loans end.

The stories you need to read, in one handy email

Read more

And in a Europe preoccupied with other matters – and in fear of an anti-establishment ascendant far right – the prospect of that happening is slim. “What we are witnessing is a disaster for the real economy because everything is on hold,” said Costas Panagopoulos who heads the Alco polling institute. “Once again we are talking about economic catastrophe, once again we are talking about Grexit,” he told the Guardian. “The next few weeks are critical. If an agreement isn’t reached, if there is more uncertainty, we don’t know how Greeks will react.”

On Thursday, amid widespread rumours of his own resignation, the finance minister Euclid Tsakalotos attempted to deflect the spiralling tensions. In a written statement the Marxist economics professor said that while a third of the bailout review had been “totally completed” and a third “totally agreed”, the rest remained subject to “political negotiation” – raising little hope of the talks concluding any time soon.

But what happens next is dependent not only on what happens in Athens. To a great degree events in Europe and Washington will also play a role.

Ahead of Germany’s general election in September, Berlin’s finance minister Wolfgang Schäuble has also raised the stakes with growing criticism of Greece – a tactic that has proved popular with voters who might otherwise support Germany’s far-right AfD party. Earlier this week Bild, the mass-selling newspaper, stoked passions further by suggesting the German government was warming to the idea of Greece leaving the euro – a notion Schäuble has openly supported in the past.

“Grexit is not our agenda, it is the agenda of those who want the breakup of Europe,” said Sia Anagnostopoulou, a leading Syriza MP and former alternate European affairs minister. “It is what Mr Schäuble wants,” she added, echoing the commonly held view that Athens is hostage to Germany.

Complicating matters further is the direction the IMF will take now that President Trump is in power. In his former role as a billionaire businessman, Trump tweeted that the Greeks were “wasting time” in the eurozone.

Last week, the IMF delivered its gloomiest assessment yet of Greece’s debt burden, arguing that it was not only unsustainable but eventually likely to become “explosive”. The IMF’s board will formally discuss the issue on 6 February but has already hinted that without a commitment of debt relief from the EU it will be unable to contribute further loans. Germany, the biggest contributor to the nearly €300bn of emergency funds assigned to Greece, insists further aid depends exclusively on IMF participation.

Analysts are undecided whether the government is deliberately stalling in the hope of getting a better deal as repayment season approaches and fears of a disorderly default mount, or whether it is playing with fire.

Syriza, like every governing party before it, has been hollowed out by the eviscerating effects of having to apply policies that it came to power vowing to oppose. On Tuesday its parliamentary spokesman took Greeks by storm proposing that Grexit be discussed “without taboo” in the 300-member house.

The once unassailable popularity of Tsipras, meanwhile, has been pummelled by the implementation of some of the harshest measures to date and few believe he has the political capital to enforce another round of austerity.

“It is not a can but a bomb being kicked down the road,” said one western diplomat. “In a world where liberal values are under threat we could be looking at a very dangerous scenario where the cradle of democracy also collapses.”

Bereft of growth and battered by cuts and tax increases, Greeks have become poorer and ever more cognizant of their own insolvency in a state where sovereignty exists in little more than name. One in three now live below the poverty line and unemployment hovers around 23%. The latest impasse has not only seen emigration levels rise and non-repayment of household and business loans soar but also nostalgia for the drachma grow.

That is what worries Panagopoulos, the pollster, most. What was once a minority view is changing fast, with the majority of Greeks in a recent Alco survey saying it was wrong to have joined the euro.

“We have become a society that has no hope, not even a slice or piece of hope for the future,” he sighed. “The only reason people want to stay in the euro is because they fear the consequences if we were to leave, but if things don’t get better that will change too.”

wat is die 200 miljard.quote:

Een Grexit had de ECB in 2012 meer dan 150 miljard gekost, in 2015 is dat bedrag nog maar 50 miljard en dalende. Het heeft de Europese belastingbetaler ~200 miljard gekost om Griekenland (en de rest van de Eurozone) te redden en dat is gelukt.

[ afbeelding ]

Kortom, het maakt nu onder de streep voor Duitsland niet veel meer uit of Griekenland eruit stapt of niet. Daarnaast zijn Ierland en Portugal alweer 'veilig' dus de kans dat er een crisis ontstaat is ontzettend klein. Tot slot was het nooit een kwestie van geld, de EU had sowieso genoeg geld om de Euro te redden, maar is het altijd een politieke kwestie geweest.

de ECB print elke maand 80 miljard bij uit het niets.

http://www.vpro.nl/progra(...)7/geldscheppers.html

Dat na 300 miljard euro van de Europese belastingbetaler afhandig te hebben gemaakt?quote:

'Duitse regering kan leven met Grexit'

BERLIJN -

De Duitse regering zou er geen problemen meer mee hebben als Griekenland uit de euro stapt. Volgens bondskanselier Angela Merkel en minister van Financiën Wolfgang Schäuble zou de Eurozone een Grexit kunnen overleven.

Dat meldt het Duitse tijdschrift Der Spiegel op gezag van anonieme regeringsbronnen.

Merkel en Schäuble denken dat de Europese economie nu een stuk weerbaarder is dan drie jaar geleden. Een Grexit zou tot problemen in andere eurolanden kunnen leiden, maar de zwakkere economieën zouden inmiddels voldoende zijn aangesterkt en de EU zou over voldoende instrumenten beschikken om een nieuwe financiële crisis het hoofd te bieden.

Volgens de Duitse regering is een Grexit onvermijdelijk als de linkse partij Syriza aan de macht komt na de Griekse verkiezingen eind deze maand.

Bron: Telegraaf, Der Spiegel.

Note. Dit is een topic uit begin 2015!!

ik ben niet gek.. ik ben volstrekt niet gek, ik ben helemaal niet gek... ik ben een nagemaakte gek

gooi alles weg neem een besluit, doe als het moet alles opnieuw

gooi alles weg neem een besluit, doe als het moet alles opnieuw

Och, er zit nog ruim 1400 miljard in de Nederlandse pensioenpot dus de EU heeft iets om op terug te vallen !

Als je geen kop hebt kan je niet uit het raam kijken.

Een pensioenpot die schadevrij was gebleven bij het omvallen van Griekenland (cs!) in 2015? Echt?quote:

Och, er zit nog ruim 1400 miljard in de Nederlandse pensioenpot dus de EU heeft iets om op terug te vallen !

Waar zeg ik dat ?quote:Op zondag 5 februari 2017 07:57 schreef VEM2012 het volgende:

[..]

Een pensioenpot die schadevrij was gebleven bij het omvallen van Griekenland (cs!) in 2015? Echt?

Het is gewoon een feit dat de EU met begerige ogen naar die pot zit te loeren en het ook niet lang meer zal duren dat ze daar uit gaan lopen graaien. Uiteraard onder het mom dat Nederland geen schade zal ondervinden..

Als je geen kop hebt kan je niet uit het raam kijken.

O, jij hebt een glazen bol? Nee, duidelijk.quote:

[..]

Waar zeg ik dat ?

Het is gewoon een feit dat de EU met begerige ogen naar die pot zit te loeren en het ook niet lang meer zal duren dat ze daar uit gaan lopen graaien. Uiteraard onder het mom dat Nederland geen schade zal ondervinden..

Niemand kan Merkel verwijten, dat de Grieken eerst geen voldoende kansen gekregen hebben.

Ik blijf bij mijnoude standpunt, dat de schuld van Griekenland zo uit de hand is gelopen, doordat wij (als EU) Grieks Cyprus lid hebben gemaakt van de EU in 2004.

Dit tegen de afspraak vooraf, dat alleen een verenigd Cyprus lid kon worden.

Hierdoor kreeg Griekenland extra ongedekte financieringen van de Grieks Cypriotische banken (à la de IJslandse banken). Zonder ie financieringen was de problematiek van Griekenland nu veel beheersbaarder geweest.

Ik blijf bij mijnoude standpunt, dat de schuld van Griekenland zo uit de hand is gelopen, doordat wij (als EU) Grieks Cyprus lid hebben gemaakt van de EU in 2004.

Dit tegen de afspraak vooraf, dat alleen een verenigd Cyprus lid kon worden.

Hierdoor kreeg Griekenland extra ongedekte financieringen van de Grieks Cypriotische banken (à la de IJslandse banken). Zonder ie financieringen was de problematiek van Griekenland nu veel beheersbaarder geweest.

Ja, ik vrees dit ook.quote:

[..]

Waar zeg ik dat ?

Het is gewoon een feit dat de EU met begerige ogen naar die pot zit te loeren en het ook niet lang meer zal duren dat ze daar uit gaan lopen graaien. Uiteraard onder het mom dat Nederland geen schade zal ondervinden..

Wij kunnen beter nu de pensioenen met 20% verlagen, en de pensioenpot nu ook met 20% afromen. Daardoor zakt onze staatsschuld met zo'n 300 miljard euro tot onder de 150 miljard euro.

Dan heeft de generatie die de aardgaspot heeft opgesoupeerd dit nu weer terugbetaalt en voorkomt daar tevens mee dat de toekomstige generaties met hun schulden opgezadeld blijven

Bedoel je nu die generatie die 300 miljard (toevallig net het bedrag wat jij noemt) in het ABP heeft geflikkerd, waardoor wij, itt tot de rest in Europa, als jongeren dat bedrag niet op hoeven te hoesten voor ambtenarenpensioenen?quote:

[..]

Ja, ik vrees dit ook.

Wij kunnen beter nu de pensioenen met 20% verlagen, en de pensioenpot nu ook met 20% afromen. Daardoor zakt onze staatsschuld met zo'n 300 miljard euro tot onder de 150 miljard euro.

Dan heeft de generatie die de aardgaspot heeft opgesoupeerd dit nu weer terugbetaalt en voorkomt daar tevens mee dat de toekomstige generaties met hun schulden opgezadeld blijven

Als de huidige pensioenen met 20% worden verlaagd, en de toekomstige pensioen op 60% van het loon gezet worden, dan kan de pensioenpot ook met 20% worden verminderd.quote:

[..]

Bedoel je nu die generatie die 300 miljard (toevallig net het bedrag wat jij noemt) in het ABP heeft geflikkerd, waardoor wij, itt tot de rest in Europa, als jongeren dat bedrag niet op hoeven te hoesten voor ambtenarenpensioenen?

Het voordeel van de huidige jongeren (tot 45 jaar) is dat zij behoorlijk minder pensioenpremies hoeven op te hoesten, waardoor ze netto meer te besteden krijgen.

En volgens mij blijft Nederland dan nog (bijna) het hoogste pensioenstelsel van Europa houden.

Ik meende dat vorig jaar voor 33 miljard euro premiegeld in de bedrijfstak pensioenfondsen is gestopt.

En pas de laatste jaren betalen we in Nederland in totaliteit iets meer dan 50 miljard euro aan inkomstenbelasting en loonheffing.

Deze verhouding vind ik volkomen scheef.

En pas de laatste jaren betalen we in Nederland in totaliteit iets meer dan 50 miljard euro aan inkomstenbelasting en loonheffing.

Deze verhouding vind ik volkomen scheef.

Je mist mijn punt.quote:

[..]

Als de huidige pensioenen met 20% worden verlaagd, en de toekomstige pensioen op 60% van het loon gezet worden, dan kan de pensioenpot ook met 20% worden verminderd.

Het voordeel van de huidige jongeren (tot 45 jaar) is dat zij behoorlijk minder pensioenpremies hoeven op te hoesten, waardoor ze netto meer te besteden krijgen.

En volgens mij blijft Nederland dan nog (bijna) het hoogste pensioenstelsel van Europa houden.

Jouw stelling was dat er een generatie is die de aardgaspot heeft opgemaakt en dat die maar moeten bloeden zodat de jongeren meer te besteden krijgen.

Nou wil ik best mee met dat er goed gekeken mag worden naar een juiste balans tussen lasten voor ouderen en lasten voor jongeren, maar als je net gaat doen alsof er op de pof geleefd is, dan wil ik best de feiten presenteren. En dat is dat diezelfde generatie 300 miljard heeft gespaard en dat die 300 miljard de Nederlandse jongeren zal ontlasten bij het betalen van ambtenarenpensioenen, waar in alle andere landen om ons heen dat geld wel door de jongeren in de toekomst opgehoest moet worden.

Daarom vond ik jouw opmerking getuigen van weinig kennis en ik breng het jou graag onder de aandacht.

Ja, ik ben het met je eens, dat ik hier te kort bocht schiet.quote:

[..]

Je mist mijn punt.

Jouw stelling was dat er een generatie is die de aardgaspot heeft opgemaakt en dat die maar moeten bloeden zodat de jongeren meer te besteden krijgen.

Nou wil ik best mee met dat er goed gekeken mag worden naar een juiste balans tussen lasten voor ouderen en lasten voor jongeren, maar als je net gaat doen alsof er op de pof geleefd is, dan wil ik best de feiten presenteren. En dat is dat diezelfde generatie 300 miljard heeft gespaard en dat die 300 miljard de Nederlandse jongeren zal ontlasten bij het betalen van ambtenarenpensioenen, waar in alle andere landen om ons heen dat geld wel door de jongeren in de toekomst opgehoest moet worden.

Daarom vond ik jouw opmerking getuigen van weinig kennis en ik breng het jou graag onder de aandacht.

Maar in grote lijnen zie ik dit als goede mogelijkheid om zowel de staatsschild als de toekomstige pensioenverplichtingen te verlagen.

De jongeren kunnen hun bijdrage aan de staatsschuld beter betalen door de HRA maar af te schaffen.

Afschaffen van de HRA is prima. Maar voor alle maatregelen geldt dat we dat doordacht moeten doen om extreme inkomensverschuivingen tegen te gaan.quote:

[..]

Ja, ik ben het met je eens, dat ik hier te kort bocht schiet.

Maar in grote lijnen zie ik dit als goede mogelijkheid om zowel de staatsschild als de toekomstige pensioenverplichtingen te verlagen.

De jongeren kunnen hun bijdrage aan de staatsschuld beter betalen door de HRA maar af te schaffen.

Iemand die geen verdiencapaciteit heeft ineens flink korten op zijn inkomsten is erg lastig. Om maar eens wat te noemen.

De staatsschuld in Nederland is ook bepaald niet problematisch. Boekhoudkundig is het 470 miljard. Trek je daar het belegd vermogen van het ABP vanaf kom je op 90 miljard. Dat is 14% van het Bbp.

Misschien zou het beter zijn als je de pensioenverplichtingen van de andere landen bij hun staatsschuld op gaat tellen, alleen krijg je dan van die verdomd irritante 3cijferige percentages.

Mijns inziens kunnen we beter goed investeren in onderwijs en nuttige infrastructuur (gericht op de toekomst, dus brainport in plaats van mainport bv), in plaats van ons druk te maken over lasten die we minder kunnen verminderen dan we aan de inkomstenkant de verdiencapaciteit kunnen verhogen.

Bewust voor dit topic gekozen vanwege 4 dingen.quote:

• Het is weer actueel

• Wat gaat Duitsland doen. Als het IMF de trekker eruit trekt (Trump heeft hier wel een troefkaart om de EU uit elkaar te spelen).

• En de Griekse-schuldenlast was bij toetreding tot de EU al onhoudbaar omdat hun cijfers nooit hebben geklopt.

• Is is Griekenland de eerste domino een gedwongen testcase voor wat er straks met Italië gaat gebeuren.

In 2015, Luxembourg (+1.2%), Germany (+0.7%) and Estonia (+0.4%) registered a government surplus, while

Sweden (0.0%) reported a government balance. The lowest government deficits as a percentage of GDP were

recorded in Lithuania (-0.2%), the Czech Republic (-0.4%), Romania (-0.7%) and Cyprus (-1.0%). Seven

Member States had deficits equal to or higher than 3% of GDP: Greece (-7.2%), Spain (-5.1%), Portugal and the

United Kingdom (-4.4% each), France (-3.5%), Croatia (-3.2%) and Slovakia (-3.0%).

At the end of 2015, the lowest ratios of government debt to GDP were recorded in Estonia (9.7%), Luxembourg

(21.4%), Bulgaria (26.7%), Latvia (36.4%) and Romania (38.4%). Seventeen Member States had government

debt ratios higher than 60% of GDP, with the highest registered in Greece (176.9%), Italy (132.7%), Portugal

(129.0%), Cyprus (108.9%) and Belgium (106.0%).

In 2015, government expenditure in the euro area was equivalent to 48.6% of GDP and government revenue to

46.6%. The figures for the EU28 were 47.4% and 45.0% respectively. In both zones, the government expenditure

and government revenue ratios decreased between 2014 and 2015.

Bron: http://ec.europa.eu/euros(...)f6-bb53-a23175d4e2de

Sweden (0.0%) reported a government balance. The lowest government deficits as a percentage of GDP were

recorded in Lithuania (-0.2%), the Czech Republic (-0.4%), Romania (-0.7%) and Cyprus (-1.0%). Seven

Member States had deficits equal to or higher than 3% of GDP: Greece (-7.2%), Spain (-5.1%), Portugal and the

United Kingdom (-4.4% each), France (-3.5%), Croatia (-3.2%) and Slovakia (-3.0%).

At the end of 2015, the lowest ratios of government debt to GDP were recorded in Estonia (9.7%), Luxembourg

(21.4%), Bulgaria (26.7%), Latvia (36.4%) and Romania (38.4%). Seventeen Member States had government

debt ratios higher than 60% of GDP, with the highest registered in Greece (176.9%), Italy (132.7%), Portugal

(129.0%), Cyprus (108.9%) and Belgium (106.0%).

In 2015, government expenditure in the euro area was equivalent to 48.6% of GDP and government revenue to

46.6%. The figures for the EU28 were 47.4% and 45.0% respectively. In both zones, the government expenditure

and government revenue ratios decreased between 2014 and 2015.

Bron: http://ec.europa.eu/euros(...)f6-bb53-a23175d4e2de

There is only one religion

Vind het ook niet erg, meer om mensen er even op te wijzen zodat ze geen oude reacties gaan quoten etc.quote:

[..]

Bewust voor dit topic gekozen vanwege 4 dingen.

• Het is weer actueel

• Wat gaat Duitsland doen. Als het IMF de trekker eruit trekt (Trump heeft hier wel een troefkaart om de EU uit elkaar te spelen).

• En de Griekse-schuldenlast was bij toetreding tot de EU al onhoudbaar omdat hun cijfers nooit hebben geklopt.

• Is is Griekenland de eerste domino een gedwongen testcase voor wat er straks met Italië gaat gebeuren.

ik ben niet gek.. ik ben volstrekt niet gek, ik ben helemaal niet gek... ik ben een nagemaakte gek

gooi alles weg neem een besluit, doe als het moet alles opnieuw

gooi alles weg neem een besluit, doe als het moet alles opnieuw

Brexit, Grexit, NLexit

Laat het gebeuren svp

Laat het gebeuren svp

Drop drop drop drop drop drop drop!!!! DROP!!! drop drop drop drop !!

The IMF Should Get Out of Greece

The International Monetary Fund's involvement in Greece has been an unmitigated disaster: Time and again, its failure to heed crucial lessons has visited suffering upon the Greek people. When the fund's directors meet on Monday, they should agree to forgive the country's debts and get out.

The IMF should never have gotten into Greece in the first place. As late as March 2010, with concerns about the Greek government's ability to pay its debts roiling markets, Europe's leaders wanted the IMF to stay away. Europeans feared that the fund’s financial assistance to one of their own would signal broader weakness in the currency union. As Jean-Claude Juncker famously put it: “If California had a refinancing problem, the United States wouldn’t go to the IMF.”

Nonetheless, German Chancellor Angela Merkel decided that the IMF’s presence was the signal needed to persuade German citizens that Greece needed urgent financial support and that strict discipline in the use of those funds would be enforced. Merkel’s political priorities coincided with the interests of Managing Director Dominique Strauss Kahn, who was desperate to pull the IMF out of irrelevance. From that moment on, the IMF became Europe's -- mainly Germany’s -- instrument in Greece.

Greece's Financial Odyssey

Then came the cardinal error: At the IMF’s Board, over the fierce opposition of several executive directors, the Europeans and Americans pushed through a bailout program that, contrary to the fund’s rules, did not impose losses on Greece’s private creditors. The decision was based on a spurious claim that “restructuring” private debt would trigger a global financial meltdown.

Thus, European governments and the IMF lent Greece a vast sum to repay its existing creditors. Greece’s debt burden remained unchanged and onerous, and the most vulnerable Greeks were forced to accept crippling austerity to repay the country’s new official creditors. The economy quickly and predictably went into a tailspin.

Even when the IMF recognized the error of its ways, it didn't change course. An internal “strictly confidential” report, later made public, acknowledged that the program was riddled with “notable failures,” including the lack of private debt restructuring and excessive austerity.

But the IMF never took responsibility. Instead, it demanded even more austerity throughout 2014. In December, the public rebelled and brought the opposition Syriza party to power, which only made the IMF’s demands more insistent. At this point, the evidence that the strategy was pushing Greece to economic and financial collapse was overwhelming. It was like requiring a trauma patient to run around the block before being admitted to intensive care. Yet as usual, the inevitable suffering was blamed on Greece's unwillingness to cooperate.

The absurdity reached an apex in mid-2015, when the IMF released a report stating plainly that under Europe's latest set of austerity proposals, Greece would need a miracle to repay its debts. At the time, the IMF’s own research showed that the best course would be to forgive the debt and abandon any further fiscal austerity. This would allow the country some freedom to grow again and possibly even attract new investment. And once that process was underway, Greece could be free of its official creditors and rely once again on private investors under notice that they were fully responsible for the risks they took.

The IMF has since sought to move in the right direction, repeatedly calling on the Europeans to write down substantial amounts of debt. The Germans, however, have refused any meaningful forgiveness. Instead, they have followed a strategy of debt forgiveness in driblets because they astonishingly believe that German citizens will not be able do the sums and recognize that ever larger relief is being granted.

And so the austerity has continued, suppressing growth and causing Greece's debt burden -- measured as a percentage of gross domestic product -- to increase. The IMF’s latest analysis, in preparation for Monday’s meeting, says that Greece's public debt levels could see an “explosive surge.”

This strategy is utterly mindless. Greeks have been subjected to gratuitous pain. Those who can leave are doing so, threatening the prospect of a graying and desolate country. With every passing day, the chances that Europe’s official creditors will see their money are dwindling. Investors have again pushed up yields on Greek bonds, fearing correctly that we are at yet another impasse.

The agony won’t end unless the IMF forces the issue. The IMF and its principal shareholders -- the Europeans and Americans -- made the original mistake and perpetuated the errors. A mere mea culpa is not enough: Real accountability requires the IMF’s shareholders to honorably accept real losses. That means forgiving the country's debts to the fund and leaving the Greeks and Europeans to work out their own solution to this mess. If the IMF stays involved, it will succeed only in further shredding its credibility.

==================================

En dan de politieke schade in Europa/Brussel Dan is de burgerij wel klaar met de EU.

The International Monetary Fund's involvement in Greece has been an unmitigated disaster: Time and again, its failure to heed crucial lessons has visited suffering upon the Greek people. When the fund's directors meet on Monday, they should agree to forgive the country's debts and get out.

The IMF should never have gotten into Greece in the first place. As late as March 2010, with concerns about the Greek government's ability to pay its debts roiling markets, Europe's leaders wanted the IMF to stay away. Europeans feared that the fund’s financial assistance to one of their own would signal broader weakness in the currency union. As Jean-Claude Juncker famously put it: “If California had a refinancing problem, the United States wouldn’t go to the IMF.”

Nonetheless, German Chancellor Angela Merkel decided that the IMF’s presence was the signal needed to persuade German citizens that Greece needed urgent financial support and that strict discipline in the use of those funds would be enforced. Merkel’s political priorities coincided with the interests of Managing Director Dominique Strauss Kahn, who was desperate to pull the IMF out of irrelevance. From that moment on, the IMF became Europe's -- mainly Germany’s -- instrument in Greece.

Greece's Financial Odyssey

Then came the cardinal error: At the IMF’s Board, over the fierce opposition of several executive directors, the Europeans and Americans pushed through a bailout program that, contrary to the fund’s rules, did not impose losses on Greece’s private creditors. The decision was based on a spurious claim that “restructuring” private debt would trigger a global financial meltdown.

Thus, European governments and the IMF lent Greece a vast sum to repay its existing creditors. Greece’s debt burden remained unchanged and onerous, and the most vulnerable Greeks were forced to accept crippling austerity to repay the country’s new official creditors. The economy quickly and predictably went into a tailspin.

Even when the IMF recognized the error of its ways, it didn't change course. An internal “strictly confidential” report, later made public, acknowledged that the program was riddled with “notable failures,” including the lack of private debt restructuring and excessive austerity.

But the IMF never took responsibility. Instead, it demanded even more austerity throughout 2014. In December, the public rebelled and brought the opposition Syriza party to power, which only made the IMF’s demands more insistent. At this point, the evidence that the strategy was pushing Greece to economic and financial collapse was overwhelming. It was like requiring a trauma patient to run around the block before being admitted to intensive care. Yet as usual, the inevitable suffering was blamed on Greece's unwillingness to cooperate.

The absurdity reached an apex in mid-2015, when the IMF released a report stating plainly that under Europe's latest set of austerity proposals, Greece would need a miracle to repay its debts. At the time, the IMF’s own research showed that the best course would be to forgive the debt and abandon any further fiscal austerity. This would allow the country some freedom to grow again and possibly even attract new investment. And once that process was underway, Greece could be free of its official creditors and rely once again on private investors under notice that they were fully responsible for the risks they took.

The IMF has since sought to move in the right direction, repeatedly calling on the Europeans to write down substantial amounts of debt. The Germans, however, have refused any meaningful forgiveness. Instead, they have followed a strategy of debt forgiveness in driblets because they astonishingly believe that German citizens will not be able do the sums and recognize that ever larger relief is being granted.

And so the austerity has continued, suppressing growth and causing Greece's debt burden -- measured as a percentage of gross domestic product -- to increase. The IMF’s latest analysis, in preparation for Monday’s meeting, says that Greece's public debt levels could see an “explosive surge.”

This strategy is utterly mindless. Greeks have been subjected to gratuitous pain. Those who can leave are doing so, threatening the prospect of a graying and desolate country. With every passing day, the chances that Europe’s official creditors will see their money are dwindling. Investors have again pushed up yields on Greek bonds, fearing correctly that we are at yet another impasse.

The agony won’t end unless the IMF forces the issue. The IMF and its principal shareholders -- the Europeans and Americans -- made the original mistake and perpetuated the errors. A mere mea culpa is not enough: Real accountability requires the IMF’s shareholders to honorably accept real losses. That means forgiving the country's debts to the fund and leaving the Greeks and Europeans to work out their own solution to this mess. If the IMF stays involved, it will succeed only in further shredding its credibility.

==================================

En dan de politieke schade in Europa/Brussel Dan is de burgerij wel klaar met de EU.

|

|